The House That Sam Built: Part II

If you’re reading this, you’re a Premium member of Front Month, a newsletter dedicated to exchange & market structure research & analysis. Thank you for reading & supporting my work! Please reply to this email with any questions or feedback & I’ll be more than happy to answer. Enjoy:

Like most televised sports leagues, Formula One thrives on a slew of high-profile sponsorships with behemoth brands from around the world. It costs north of $50 million per year to get a brand name on a Formula One car depending on the team & placement on the vehicle. While the price tag is high, the returns are real - more than 600 million people globally watch F1 throughout the season, with ratings in North America particularly strong amid Netflix’s stellar F1 documentary series. Stakes are as high for brands as the cars & drivers themselves.

On September 23 Mercedes’ championship contending F1 team announced the addition of a new sponsor to its long list of partners. Current partnerships include the $50 billion Malaysian state-owned oil company Petronas, chemicals giant INEOS, UBS, Hewlett Packard, and other major corporate brands. The team’s new sponsorship deal seemed a bit unique in comparison - cryptocurrency exchange FTX earned access to the car, drivers & team in a long-term deal for an undisclosed amount likely in the tens of millions per year.

F1 isn’t the only area where FTX is shelling out serious money. FTX has inked brand deals with Tom Brady, Major League Baseball, high-profile esports teams, and Miami’s downtown sports arena. The price tag & sheer quantity of sponsorship deals in such a short amount of time has certainly raised eyebrows in & out of the crypto space. Where is FTX getting all this money? What’s the larger marketing strategy here considering FTX’s slim presence in the US today? What does FTX even do?

To answer these questions we again return to the young but explosive career of Sam Bankman-Fried. SBF’s exchange is rewriting the strategic playbook in many ways & has thus far shown impressive returns. This post examines how & why FTX is likely to challenge more than just competing exchanges in far-off corners of the financial world.

We begin in 2018:

Unique Partners, Unique Profits

Alameda Research entered the summer of 2018 on a high note. It had just pulled off a fame-grabbing hundred million dollar Bitcoin/Japanese Yen trade & was expanding its presence across every major global crypto exchange. New products, cross-asset mispricings & demand for liquidity could be found around almost every corner. The transition from a college dorm-room trading outfit to a sophisticated global firm was advancing quickly.

Amid this expansion, Alameda began to realize just how nascent & unformed the structure of the crypto market truly was. The exchanges it was interacting with on a daily basis were difficult to use, plagued with technical issues & lacked functionality Alameda was looking for. Through its vast network of crypto exchange & OTC relationships Alameda had access to a view of the market few other firms could match, and this view became an idea.

What if we launched our own exchange?

The company would achieve product-market fit from the second it opened. Who better to build an exchange than its top customer, the very firm who would immediately use the products it sought to build? Alameda could now turn complaints about other exchanges & product aspirations into a tangible business model.

Preparations to launch an exchange began in 2018, and after a few short months SBF’s team had a working futures platform ready to go. FTX officially opened for business in May 2019, offering a suite of crypto futures & leveraged tokens for trading backed by Alameda’s competitive liquidity & a packed roadmap of new features & products on the way. Success immediately followed - by early July more than $300 million was trading hands daily on FTX.

FTX’s early success was driven by a long list of differentiators & catalysts, two of which I want to examine in particular:

The Alameda cheat code.

Binance.

The first catalyst is pretty apparent & serves as a unique market structure case study. A lone market maker had never started their own exchange prior to FTX, and it’s unheard of in traditional markets for an exchange & a market maker to be working together under the same roof.

There are ethical reasons for this. Given their central role an exchange has access to more complete data about their customers than any other market participant. If FTX is able to feed this data to Alameda & excludes other market makers from this arrangement, Alameda would have an unfair advantage over competing trading firms & FTX’s own customers. This relationship leaves plenty of room for collusive behavior that may not put end users of FTX’s platform first.

On the other hand, there are scenarios where an exchange-market maker combo can be both a competitive superpower & a good thing for end consumers. All upstart exchanges face a difficult dilemma - the core product they want to provide (liquidity) is something they can’t directly create themselves. Partnerships with market makers are therefore vital to that exchange’s success. Many times the agendas of the exchange & market maker differ too much to work together, and the exchange is forced to shut down because it can’t do its job.

When FTX first launched it didn’t have to worry about relying on third party liquidity providers. Alameda was ready to quote prices from day one in full cooperation with the exchange it was itself standing up. Think of this like vertical integration - the venue and provider of a liquid market working together in perfect unison.

I think the FTX/Alameda relationship is tolerable as long as their incentives are aligned with users & focused on supporting the best possible trading experience. In a growing, competitive market like crypto I think this alignment does exist - for now. If FTX can’t offer customers tight spreads & sufficient order book depth they’ll lose market share to platforms like Binance, Bitfinex or OKEx regardless of Alameda’s presence. When more than one exchange is battling for market share in the same product, I think an exchange/market maker combination is permissible under strict supervision.

The situation gets murky when thinking about a market where one exchange has all the market share. If the exchange/market maker combo faces no competitive pressures it can trade against its customers without having to worry about providing them the best experience, likely resulting in unfairly high transaction costs. This I am not a proponent of. Crypto exchanges haven’t been forced to consolidate yet, but if FTX does become the global market share leader I’ll begin to have more issues with its close ties to Alameda.

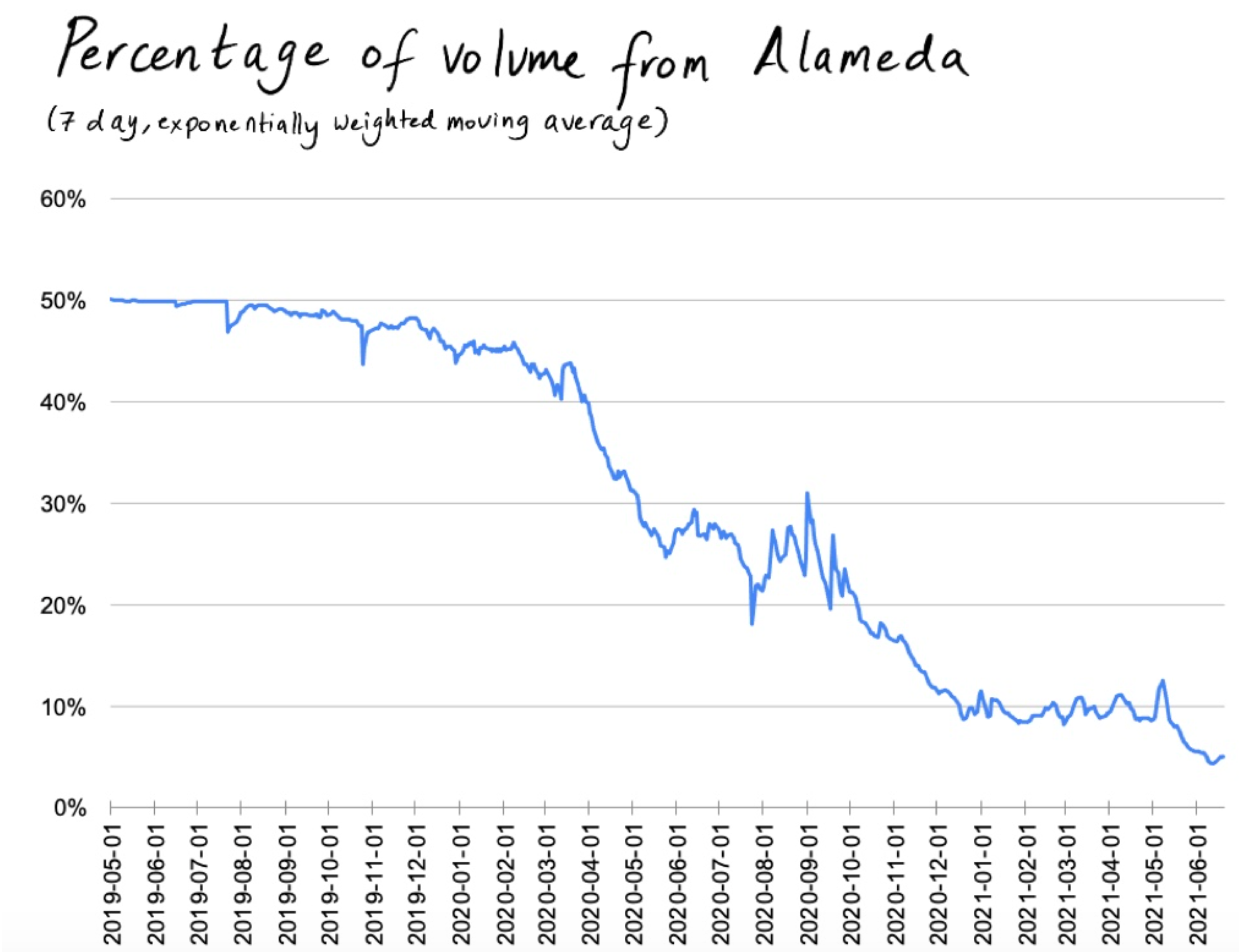

As newly released data shows, when FTX first launched Alameda accounted for ~40-50% of the exchange’s order flow from its inception to early 2020, meaning it took the other side of almost every trade made on FTX’s platform:

(Source)

Apart from the Alameda cheat code, FTX got a big early boost from another unlikely partner - Binance, the world’s largest crypto exchange launched by Changpeng Zhao in mid 2017. Binance took an early interest in FTX and announced a partnership with the exchange in late 2019, including a sizable equity stake in the company & its associated FTT token.

Why would the industry’s largest exchange back an emerging competitor so quickly after launch? Revisiting Binance’s own timeline puts the investment into better context.

Binance was in the midst of launching its own futures exchange in September 2019, putting them behind the curve relative to FTX. At the time a partnership favored both parties - Binance received help building its futures platform & attracting institutional flow, FTX received new sources of capital & Alameda received deeper access to Binance’s ecosystem.

There’s also Binance’s BNB utility token to consider. FTX released BNB futures shortly after it launched in May 2019, and early volume data leads me to believe the product saw strong user adoption in the following days. A Binance partnership with the largest futures market for its own utility token makes a lot of sense to me.

The nature of Binance & FTX’s relationship was further complicated when FTX repurchased Binance’s stake in the exchange in July 2021, ending their partnership after only two years. The decision to go separate ways was mutual according to SBF & Zhao, but closer inspection gives me a different opinion. Here are SBF’s own words on the decision to kick Binance out of FTX’s cap table:

“I think it just makes sense given the role that our businesses are playing in the space…”

“I think there are some differences between how we run our businesses. I think there are ways I would have reacted, responded, and run things differently. And we have been running things differently.”

“…something I'll say is that we try really hard to be as cooperative as we can with regulators… I think that when you don't do that, and when you sort of appear less flexible or responsive, I think that’s more likely to lead to cases where regulators might feel like they have no choice but to start bringing the hammer.”

I think FTX’s decision to split from Binance was primarily about image as each exchange begins to clash more with regulators around the world. Binance has historically been seen as the less compliant exchange, consistently moving its headquarters to avoid international crackdowns & suffering a slew of executive resignations as it tries to gain traction in the US. Meanwhile FTX is attempting to take a more direct, overt & friendlier approach to regulation, acknowledging that compromise with governments about crypto adoption is the only way towards a future the industry wants.

Regardless of their differences FTX and Binance both helped each other become the largest crypto futures exchanges in the world - their stark divergence when it comes to growing in developed economies is a recent & noteworthy event.

Understanding the Business

Today FTX boasts a user base of ~1.25 million retail accounts & ~2,700 institutional customers with $2B-$2.5B in average daily trading volume. SBF has publicly noted the exchange expects to make nearly ~$1 billion in revenue in 2021. The exchange’s retail customer base skews high net worth ($3M monthly ADV per retail user) and is concentrated in Asia & Europe with a significant presence in Turkey, South Korea & Australia:

(Source)

Like its competitors FTX makes a vast majority of its revenue from transaction fees - payment for executing & managing crypto trades on its platform. These transaction fees have grown by a factor of 10x in 2021 as the exchange rode the bull craze of Q1 to record levels of volume & open interest. Today FTX’s Bitcoin futures open interest stands at ~$1.8 billion notional as of September month-end (for context, CME Bitcoin futures OI stood at ~$1.6 billion):

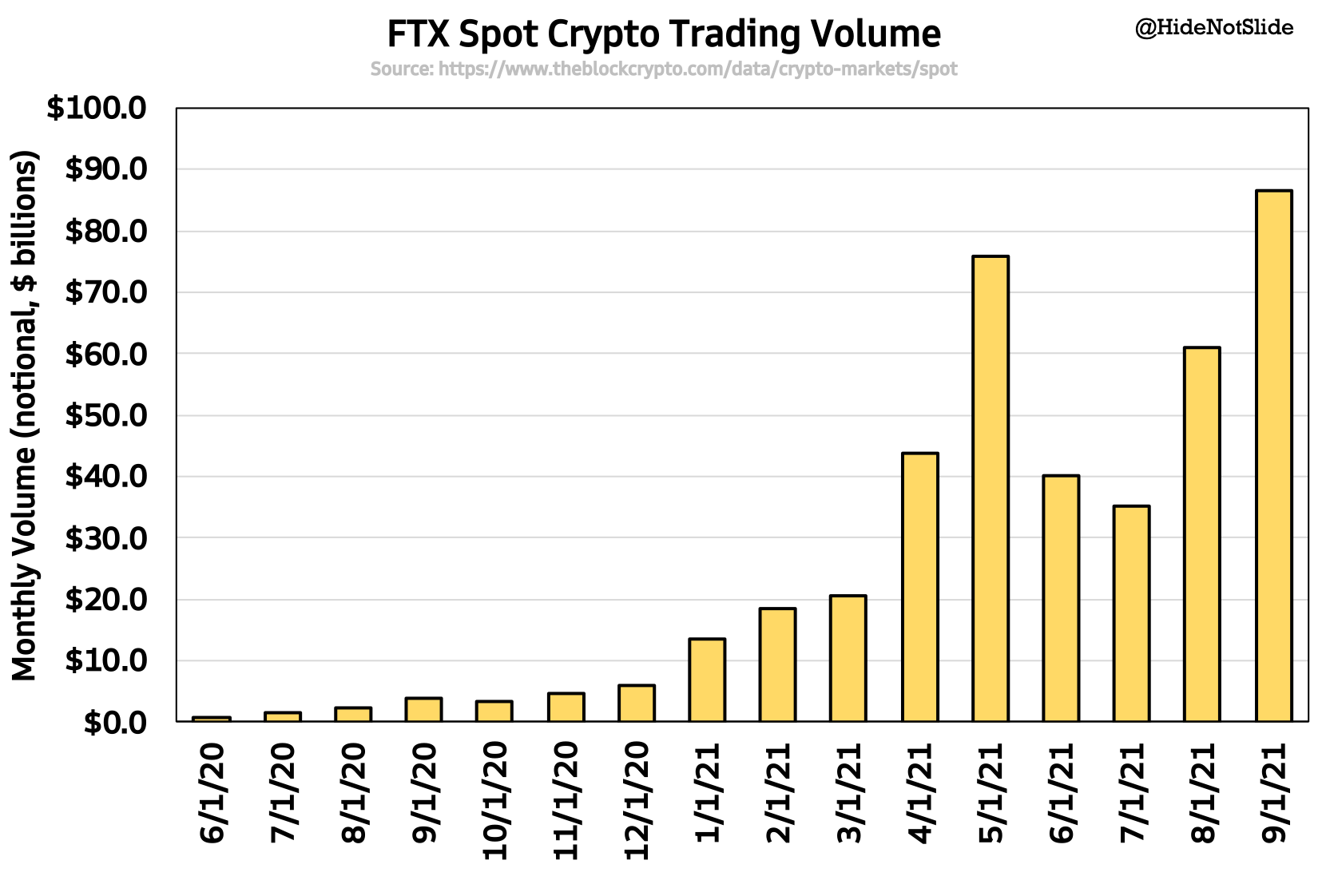

Spot trading has also ridden the bull wave to record activity since launching in mid 2020 - volumes crossed the $85 billion notional mark in September 2021:

To review, FTX enters Q4 2021 with:

Breadth - A diverse business across geographies, customer mix, and products

Depth - Volume & open interest rivaling competition in the US and internationally

Cash - A large & growing war chest from record transaction fees this year

Where is the exchange looking to expand next?

America - Forming a Beachhead

Every major investment FTX has made in the last 12 months has been focused on capturing retail trading revenue in developed economies, particularly the US. The company launched a separate US exchange in mid-2020 to comply with local regulations & begin building market share. It then bought Blockfolio, a retail-focused crypto price & news tracking app boasting ~800,00 daily active users largely in Europe & North America. More recently FTX purchased LedgerX, a US-licensed derivatives exchange & clearinghouse which it plans to integrate with its existing platform & expand its offerings to include equity spot & futures trading, putting it in competition with the likes of Robinhood & the rest of the discount brokerage field. The pace of deals in and around North America show FTX’s focus on becoming a serious competitor to all exchanges in the region.

Why go so hard after US customers? Fee capture. Retail customers in the US pay exorbitantly pricey crypto trading fees today, show high levels of stickiness, and trade frequently in line with the broader crypto bull/bear cycle. Coinbase is the shining example of an exchange enjoying fat trading margins with a loyal & engaged retail customer base. More people trade on Coinbase than Coinbase Pro despite no switching costs & lower fees! If that’s not a sign of a wealthy, fee-indifferent customer base, I don’t know what is.

Success as a retail crypto exchange is heavily dependent on acquiring & retaining users at scale, which means monumental spending on marketing & advertising. Coinbase spent ~$200 million on marketing alone in Q2 2021 equating to 10% of revenue. This money is spent through a variety of channels, including YouTube ads, Twitter influencer deals, affiliate marketing & TV commercials - what I consider to be a more classic approach to attracting eyeballs & retail signups. These channels are controllable, measurable, & flexible - Coinbase can easily turn off one channel or move money elsewhere if ROI metrics aren’t performing. As long as Coinbase continues to throw immense amounts of money towards marketing in the US, my bet is they’ll remain relevant regardless of their fee levels in the short term.

Let’s compare this to FTX’s approach. FTX is spending just as much if not more money on marketing than Coinbase is, which is notable given the size & profit discrepancy between the two exchanges. FTX has publicly committed to ~$350 million in marketing spend in the last few months, not to mention undisclosed marketing deals that likely add another few hundred million to the total. FTX is serious about getting its name into the minds of everyday Americans.

What I find interesting is the way FTX is spending all this money. They’re not focusing on YouTube ads & social media spend, although that’s surely a small part of the budget. Most of FTX’s marketing dollars are going to massive, multi-year sponsorship deals with iconic American franchises. Major League Baseball. The NBA. College football. Formula 1. Even e-sports. These long-term deals are less flexible & offer nebulous payoff compared to a traditional Coinbase marketing approach - FTX can’t simply back out of a 5-year deal if users aren’t converting the way the exchange thought, and it’s hard to trace retail signups back to a specific sponsorship deal.

I believe FTX’s marketing investments are risky but worth the outlay. On one hand, if regulators muffle FTX’s product launches or keep them from gaining momentum in the US, the exchange will find itself with a big brand presence in America, but no real operational presence. On the other hand, SBF’s exchange is playing major catch-up in the US, and the only way to make quick progress on the brand management front is with big, headline-grabbing deals that magnify the potential return on investment. While I’m not fully bought in on the sponsorship deal angle, I like how much money FTX is spending on US marketing & think it will lead to market share gains as long as regulators don’t interrupt the exchange’s advance.

Conclusion

In just four short years Sam Bankman-Fried has ascended from a low-profile ETF trader at Jane Street to one of the most well-known names in modern finance. His interest in a simple cross-exchange arbitrage became the largest trading firm in all of crypto, and that firm’s interest in better market structure became a $20 billion business with no signs of a ceiling in sight. The US has become the next battleground for foreign crypto exchanges looking to take a slice of the valuable retail pie - I expect FTX to emerge as the region’s top challenger. Their controversial but powerful use of an in-house market maker to source liquidity & flashy marketing tactics are sure to force other exchanges to revisit their age-old strategies.

SBF once said buying Goldman Sachs & CME wouldn’t be out of the question if it was able to beat its competition. While I do believe the comment is a bit hyperbolic I’ve seen nothing to make me think he & his firms can’t continue to surprise both the crypto & legacy exchange world for many years to come.

I can’t thank you enough for reading & supporting my work! It means a great deal to me. Please feel free to reach out with any questions or ways I can make this service better.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, COIN and VIRT. I am also long Solana.