Let's Talk About The Coinbase Fee Problem

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

The last few weeks have given new meaning to the term “crypto volatility”.

It was only a couple weeks ago when Elon Musk appeared on a highly anticipated episode of Saturday Night Live, at one point asking the cast to call him “DogeFather” after sending meme cryptocurrency Dogecoin to new highs. We may end up looking back to Musk’s SNL appearance as a near-term top for the crypto space - since the show’s airing most coins have dropped by nearly -40%, whipsawing wildly on the way down. Musk’s closely watched stance on crypto is changing by the day. China is revamping its crackdown on mining activity within its borders. The Fed is considering creating its own digital currency. New headlines are flying so fast it’s been a struggle to keep up.

Meanwhile my foray into crypto market structure continues. Research began with a preview of Coinbase’s IPO, where I digested the company’s S-1 filing & decided to avoid the stock on its first day of trading. I then continued down the DeFi rabbit hole with a study of Uniswap, the industry’s largest independent decentralized exchange. My look into top HFT firms like DRW and Jump Trading revealed even more about crypto’s evolution as an asset class.

Today I want to continue this crypto foray with an update to my Coinbase investment thesis. On May 17 I began a small long position in Coinbase at ~$242 based on three developments:

Coinbase stock has fallen -30% since IPO but 2021 revenue projections have gone nowhere but up.

I believe Coinbase will benefit from the crypto “Virtu principle” and now offers exposure to this at a reasonable price.

I like Coinbase’s string of recent & rumored acquisitions should they materialize.

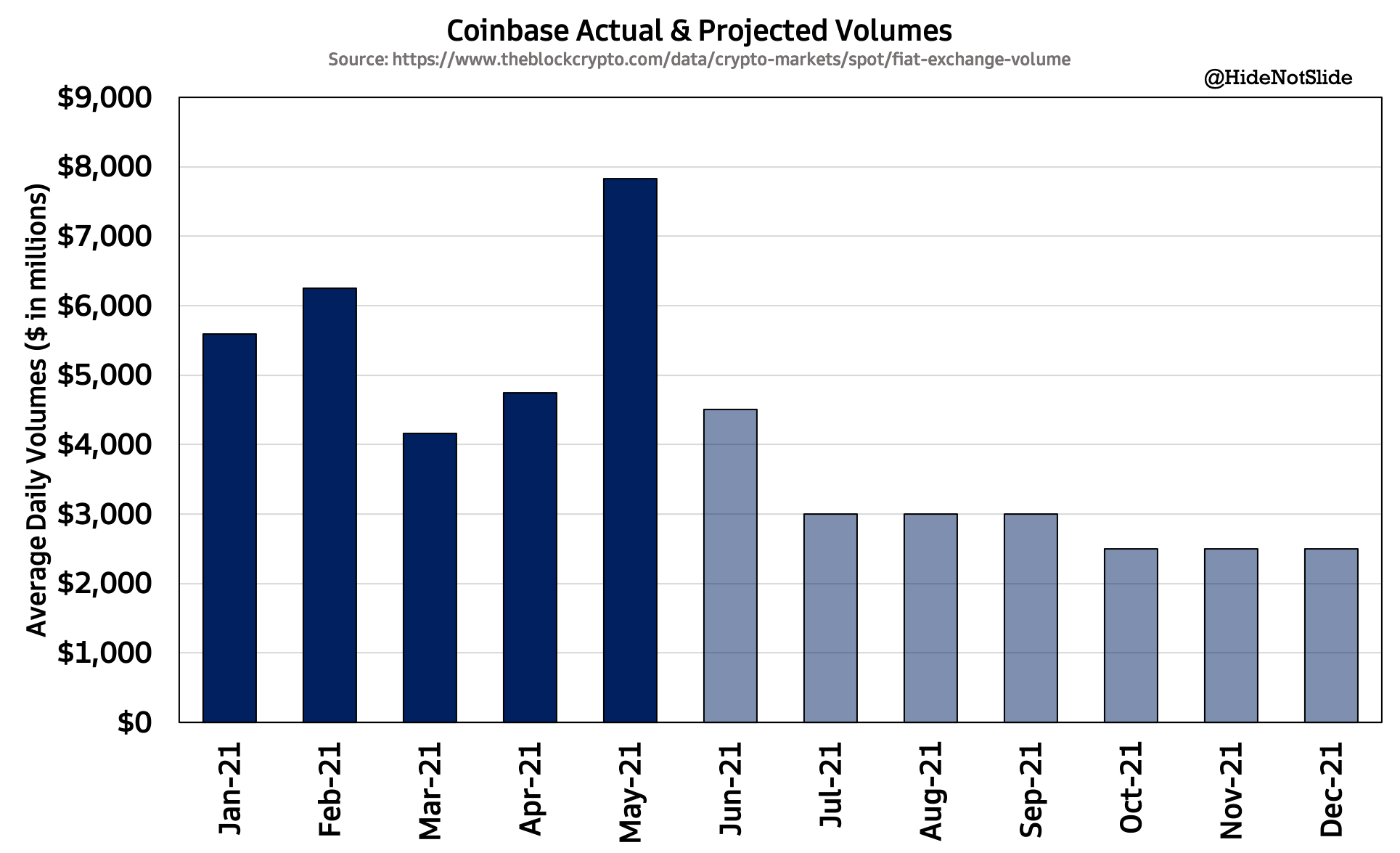

2021 has so far been a gangbuster year for Coinbase - Q1 2021 saw more trading volume & revenue than all of 2020 combined. Average daily volumes through May have continued their blistering pace and are set to make a new all time record. If we assume volumes drop off a cliff through the rest of the year I still can’t see how Coinbase doesn’t make at least $5 billion in annual revenue, with a more reasonable base case closer to $6-$7 billion. If we assume $6 billion in revenue this year & conservative 45% net margins, we arrive at 2021 projected Coinbase earnings of ~$2.7 billion. I’m buying Coinbase at a $62 billion market cap for $2.7 billion in net income, or ~23x this year’s earnings. Certainly not nosebleed valuation levels by any means.

(Source)

Okay, short term performance is all fine and good, but we can’t value Coinbase on this year’s performance alone. How should we think about the exchange’s normalized long term volumes? This brings me to my second point - the “Virtu principle”. I own shares of Virtu Financial and view the stock as a reasonably-priced call option on future equity market volatility. If US equity markets were to drop sharply down the road Virtu would be able to capitalize on the volatility and mint massive profits, acting as a counter-cyclical portfolio hedge. I believe Coinbase exhibits the same general dynamic for the crypto market - when volatility spikes as prices move sharply either up or down, retail users come rushing back to the app & transaction fees surge.

I have no idea what’s going to happen to the price of Bitcoin or Ethereum long term, and I can assure you analysts covering Coinbase stock don’t either. What I can wager with some confidence is that crypto volatility will continue to spike from time to time, and Coinbase will be able to mine that volatility into surprisingly strong earnings. It doesn’t really matter what a “normal volume year” looks like for Coinbase if random bouts of volatility ensure that year never happens.

Lastly, I like what Coinbase is doing on the M&A front to build revenue streams outside of pure buy/sell transaction fees. Recent acquisitions include Bison Trails, a blockchain infrastructure developer, and Skew, a data analytics firm serving the institutional crypto market. Rumors have also surfaced that Coinbase is considering getting into asset management by buying Osprey Funds, the 2nd largest bitcoin fund operator & a client of Coinbase’s custody business. The more Coinbase can diversify away from retail transaction fees toward institutional products, the better their long term prospects will be - I see these deals as a slow but steady push in that direction.

For all the positives laid out above, there remains one question before I build a bigger position in Coinbase, and it’s a big & complex question to answer fully. Today Coinbase makes ~90% of its revenue - an overwhelming amount - from retail transaction fees, taking a hefty cut of each trade made on its app. How are retail trading fees the bedrock of a successful long term exchange? Won’t competitors come in and undercut Coinbase on price, destroying its primary source of revenue?

I believe most, if not all the alpha to be made in Coinbase long term is dependent on answering this one question correctly.

Here’s my attempt:

Coinbase’s #1 Threat Is… Coinbase

Over the last five quarters, ~$193 billion in retail notional has traded on Coinbase’s platform. From that $193 billion Coinbase made ~$2.5 billion in transaction fees. Taking $2.5B / $193B gives us an average retail fee of ~1.30% since Q1 2020.

That’s high. Like insanely high. If you logged into your traditional brokerage account to buy $10,000 of Apple stock, because of today’s hyper competitive & efficient equity market your upfront commission to make this trade would be $0. Sure you’d be paying hidden costs like a marginally wider bid/ask spread or slightly worse fill (hello PFOF), but this is barely noticeable for liquid stocks. If you logged into Coinbase today to buy $10,000 of Bitcoin, your upfront commission would be, on average, $130. Holy cow.

Why are crypto fees so incredibly high? Some would tell you it’s because Coinbase has very little competition and therefore carries immense pricing power. CB was one of the first centralized crypto exchanges to market and is the biggest in the US - being the first & the largest does come with its share of perks. I certainly think this theory has merit, but it doesn’t fully explain why customers are still paying such high trading fees. The cost of switching to a competing platform is pretty low, save a few bank account connections & sign up questions. There are also competitors with much lower fees than Coinbase - Voyager Digital offers completely free crypto trading for example. Payment companies like Square & Venmo are also offering low cost crypto trading through their apps. Why haven’t Coinbase customers left for these alternatives in droves?

Customers don’t even have to look outside of Coinbase’s ecosystem to find lower fees. Coinbase Pro, the exchange’s platform for professional & institutional point-and-click traders, offers dramatically lower fees & better functionality than Coinbase’s retail app. CB Pro allows limit orders. Its market data services are more robust. Customers can instantly transfer funds between CB & CB Pro with no fee. Traders on CB’s retail platform pay anywhere from 0.50% - 3.99% per trade depending on order size & payment method. Coinbase Pro users pay 0.10% - 0.50% for the same trades. The exchange’s average revenue capture of 1.30% is nearly 3x higher than the most expensive CB Pro fee, implying most customers stick to the retail products and pay more. There has to be some reason customers aren’t switching & saving money. What is it?

The Brand Is King

The best explanation I’ve been able to give for Coinbase’s sticky customer base despite high fees is the exchange’s unbeatable brand value. The nature of cryptocurrency trading involves higher risk than traditional assets, mainly the risk of being hacked or scammed & having your funds stolen. Coinbase has never been hacked. Customer funds have been kept safe since the exchange’s inception. I believe the kind of retail customers who have limited knowledge of the crypto space overwhelmingly choose Coinbase as their safe, trustworthy trading option, and are willing to pay up for peace of mind. Other crypto exchanges haven’t been able to win customer trust as well as Coinbase has.

I believe Coinbase’s brand is further strengthened by its app design & user interface focusing on ease of use. Again, the nature of crypto lends itself to complexity - open a wallet, write down your 26 word private key, DO NOT LOSE IT, copy a wallet address over here, paste it correctly there, pay gas fees, and don’t mess up or your funds may be lost forever. Retail customers who don’t want to deal with maintaining a web of crypto wallets & passwords can log into Coinbase and trade just like they would in a traditional brokerage account. In this regard Coinbase could be considered the Robinhood of crypto - maintaining a competitive advantage over other brokerages through a clean, seamless, almost addictive trading experience. This experience is why Robinhood commands higher PFOF rates than its larger competitors, and why Coinbase may be able to charge higher fees and keep customers from moving to lower cost alternatives.

Just like in the consumer packaged goods or auto industries, when a product or service becomes commoditized, brand value becomes the only key point of separation from competitors. Coinbase’s brand value is unmatched in the crypto space, which comes with inherent pricing power as a result.

Will this brand value erode over time? I don’t think so. After a blockbuster IPO and a surprise $1.4 billion debt offering late last week, Coinbase has plenty of cash to burn. The company has been spending heavily on marketing efforts this year, with $118 million in marketing spend in Q1 2021 alone. This spend isn’t expected to slow down anytime soon - Coinbase expects to triple their marketing spend in 2021 to nearly 15% of net revenue. That’s likely a lot more than any other crypto exchange can muster.

What It Means For The Stock

I think Coinbase’s strong retail brand means that it could command higher trading fees for longer than the market may be expecting. If fees were a serious concern, customers would have already switched to Coinbase Pro and the exchange’s retail fees would be plummeting. That largely hasn’t happened yet, and I think it could be many years before fee pressure starts becoming a material headwind. In the meantime Coinbase is working to diversify revenue streams & push into institutional businesses, which I think is the correct long term move. I’m holding on to my COIN shares through the recent volatility and am willing to buy more if it suffers another downturn. Assessing an exchange’s brand value is difficult & up for interpretation, giving potential investors an opportunity to capture mispricings in the stock. I’m starting to believe that Coinbase’s brand value counts for more than others may be expecting.

Honorable Mentions

CME announced plans to launch Bloomberg Short Term Bank Yield Index Futures later this year, bolstering its interest rate product suite for a post-LIBOR future. The launch is notable as it complements (even cannibalizes) CME’s already popular SOFR Futures, built on an index that’s supposed to be a viable alternative to LIBOR and its Eurodollar contract. If the market is signaling demand for other interest rate benchmarks, it implies a perfectly suitable hedging solution hasn’t presented itself yet. Maybe BSBY futures will be that solution.

ICE announced record exchange-wide open interest this week surpassing a previous record set in March 2020. Growth in global oil & gas futures have bolstered recent results, but a rebound in European interest rate markets is what sent total OI to new highs.

The FT’s Robbin Wigglesworth published a good piece on the $9M S&P XIV fine that argues it’s a signal of stricter index regulation to come. As we’ve profiled in the past, index providers have amassed immense power as Wall Street’s gatekeeper & quasi-regulator. Fines like this one show their un-challenged growth in power may come with a bit more of a fight down the road.

Chart of the Week

In late March ICE launched its latest expansion in the Middle East, called ICE Futures Abu Dhabi with a flagship Murban Crude Oil Futures product. The contract was launched as its star Brent future faces potential threats from shifting global oil supplies & trade. Murban Crude Futures give traders a way to hedge exposure to a specific grade of oil at a specific regional delivery point, rather than using Brent or WTI and getting imperfect price protection.

Since launch Murban Crude Futures have seen promising initial success, with nearly 50,000 lots of open interest built through May representing over $3 billion of notional:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, COIN and VIRT. I am also long Bitcoin and Uniswap’s UNI governance token.