Don Wilson's Hidden Empire

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

High frequency trading (HFT) is an often talked-about but misunderstood industry. Extremely smart people work in HFT, and like all industries, some use their knowledge & skillset to improve markets & the economy, while others use it to enrich themselves at another’s expense. The extreme complexity of their strategies & products they trade make them hard to understand & easy to blame when markets fail, and their sheer size can instill fear among layman investors & politicians alike.

I want to shed more light on the nuances of HFT by making three core arguments:

Firms who embraced HFT early in its evolution are today’s kings.

HFT firms help expand the market’s frontier.

HFT is the new active management.

Thankfully, I can make all these points by telling the story of an elite, influential & secretive HFT firm - DRW. DRW’s rise to power is the perfect example of a traditional open outcry trading firm evolving into a sophisticated, pervasive presence in modern markets.

We begin in 1989.

First Eurodollars, Then The World

Don Wilson began his career at 21 years old as the youngest trader in the CME Eurodollar pits, when open outcry trading was near peak popularity. He was given a $100,000 account by his employer, LETCO, to trade & make markets in Eurodollar options. Wilson would trade in the pits by day & stay up late building models & studying the markets by night, forming a foundational knowledge of trading, risk management, and interest rates.

1992 saw two now historic events take place that set Wilson up for Wall Street dominance in the years to come. First, Wilson decided to start his own firm named after his trading badge initials - DRW Investments LLC. The operation began as himself, a few other traders & clerks, and a single programmer focused solely on Eurodollar options.

Second, that same year CME unveiled Globex, a new state of the art electronic trading platform allowing day & after hours sessions online. Wilson was one of the first to sign up & trade on Globex despite minimal adoption of the platform at first.

This brings me to my first point - firms who embraced HFT early in its evolution are today’s kings. Of the 10-20 firms that make up the bulk of high frequency trading profits, a large majority were launched before the 2008 financial crisis and many even prior to 2000. Because superior technology leads to direct competitive advantages in HFT, barriers to entry have become insurmountable over the last decade as companies have invested in ever faster exchange connections & market data feeds. A 2017 paper from researchers at Cornell & Penn argues this exact point - newer, smaller entrants that engage in HFT can survive, but they don’t get anywhere near the share of profits that larger, more established firms enjoy. Many end up leaving the industry altogether.

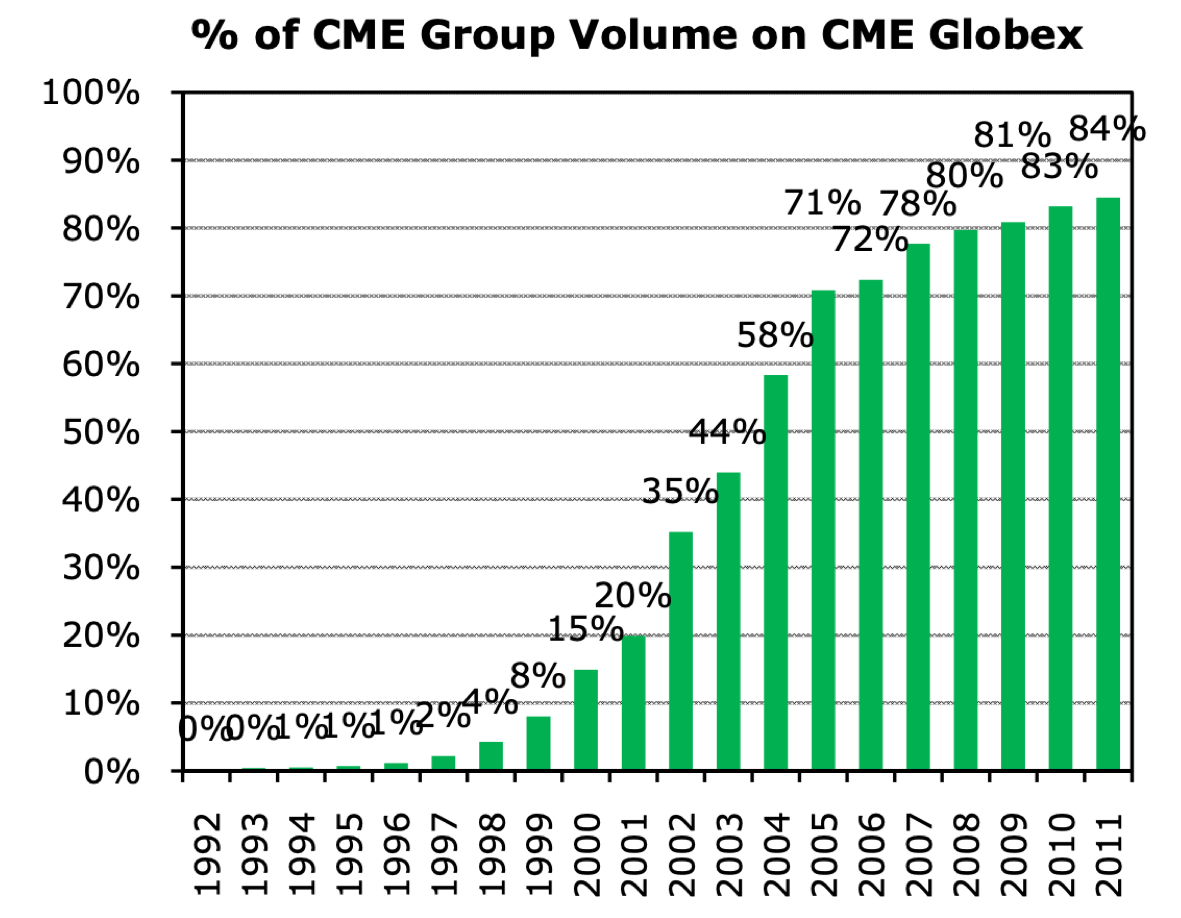

DRW was one of these firms that prioritized early investments in new technology, and it quickly paid off in spades. By 2005 nearly 75% of trading on CME took place electronically, and Wilson’s early adoption of the Globex platform gave DRW a valuable head start:

(Source)

In 2000, CME demutualized and became a for-profit, shareholder owned company. Members of the exchange (including DRW) converted their membership into CME equity and owned ~95% of the company. DRW was then able to leverage handsome profits from CME’s IPO in 2002 to seed further tech investment.

Now with a staff of over 100, DRW exited open outcry trading in 2005 and expanded to new markets, including agricultural & FX futures. When Lehman Brothers went bankrupt in late 2008, DRW was the only non-bank to participate in the fire-sale auction of Lehman’s derivatives business. Lehman took a combined $1.2 billion loss on the sale, which was quite a discount for those on the other side of the trade with the expertise to handle new books of business. The passing off of assets from a dying bank to a rapidly growing HFT firm is the perfect symbol of a changing of the guard among Wall Street’s upper echelon.

DRW’s next era of growth aligns well with my second point - HFT firms help expand the market’s frontier. A high frequency trading firm can profit from three primary activities:

Passive market making - providing liquidity in different markets & collecting the bid/ask spread in return for taking on the risks of being a middle-man.

Proprietary trading - taking short & long-term positions with owner capital to make a profit.

Latency arbitrage - exploiting market fragmentation by capturing price differences across exchanges before slower participants have time to react.

Competition within these verticals is intense. Spectators have argued the industry is engaged in a massive arms race to capture winning trades with technology that’s quickly approaching the limits of physics. HFTs need to take increasingly bold risks to separate themselves from the pack & succeed.

DRW took a bold risk in 2011 when they spotted a mispricing that harked back to Wilson’s early days in the CME pits. At the time Nasdaq operated a small, illiquid swaps exchange called IDCG, and certain products on their platform weren’t trading in line with their related Eurodollar futures contracts. Throughout 2011, DRW amassed large positions in these swaps and made $20 million when the mispricing corrected itself. Following the trade DRW was sued by the CFTC for alleged market manipulation - they were accused of repeatedly “banging the close” in an opaque market for illegal gain.

The ensuing legal & courtroom battle is a great story for another time - the abridged version is after a years long trial, DRW beat the CFTC and had the case thrown out. The below quote from the judge sums up the verdict pretty well:

“It is not illegal to be smarter than your counterparties in a swap transaction, nor is it improper to understand a financial product better than the people who invented that product.”

-Judge Richard Sullivan (source)

DRW was willing to trade where others wouldn’t to make a profit, going so far as to survive a drawn-out legal battle with the CFTC. I consider this frontier market activity HFTs engage in consistently.

If that’s not enough to convince you of HFT’s frontier status, consider this - DRW is one of Bitcoin’s top market-makers and has been since 2014, long before the retail hype began. The firm incorporated its Cumberland crypto subsidiary in early 2014 to mine Bitcoin when prices traded in the $300-$400 range. When Silk Road mastermind Ross Ulbricht was arrested and convicted in early 2015, the Feds were left with 140,000 Bitcoins on Ulbricht’s laptop to auction away. Guess who scooped up nearly half of these Bitcoins? That’s right - DRW. While it’s unknown how many of them DRW kept long term, the value of the firm’s haul amounts to $3.5 billion at current prices.

Crypto as an asset class makes perfect sense for an experienced HFT - the market is 100% electronic, highly volatile, and rapidly growing in size & popularity on Wall Street. Firms like DRW provide a valuable service to crypto traders by sourcing liquidity & lowering transaction costs in a relatively small, chaotic market.

I’ll end with one last argument - HFT is the new active management. While most HFTs don’t manage outside money, they have many of the same goals as active managers - mainly to leverage their portfolio of assets to outperform the market & make their owners wealthy. To do this, HFTs create their own trading strategies and diversify their investments to weather all market cycles.

For example - in addition to a highly profitable trading unit, DRW houses its own venture capital arm to invest in fintech trading startups. Their current portfolio includes:

Premise - a diversified data services platform

OpenFin - a financial services operating system developer

ERIS - a creator of futures & options products in partnership with ICE and CME

Convexity Properties - a large real estate portfolio of more than 60 commercial, retail & residential properties

While it’s painfully clear how fast traditional active management is fading away, I believe it’s equally clear how a new type of active expertise is surviving & even thriving in this new market environment. The only difference is these new active managers aren’t focused on amassing outside capital - they simply don’t need it.

Today DRW continues to stand near the top of the HFT podium. While exact numbers are unknown, filings show DRW’s UK subsidiary routinely pulls in half a billion dollars in revenue per year. Ex-employees of DRW’s Cumberland crypto unit are becoming highly influential parts of the industry, and its venture unit is seeding a new set of successful fintech startups. The firm has survived wholesale transformation of its industry, intense competition, and high-profile legal battles to stay relevant and highly profitable.

The next time you check the price of Bitcoin, 10 Year Treasury yields, or even most agricultural commodities, give a little credit to DRW. Don Wilson’s hidden empire probably had a critical hand in setting that price.

Honorable Mentions

Hong Kong Exchange notional trading volumes are now 4x that of LSE as the venue sees fresh inflows from mainland China & large tech IPOs, giving it the title “Nasdaq of Asia”.

Ahead of its IPO, Coinbase has amassed a $77 billion valuation based on recent trading on Nasdaq Private Market, making it more valuable than exchange heavyweights including ICE and CME.

Charles Schwab added more than 1 million new clients in January 2021, up +200% year over year and +75% month over month. The retail trading tsunami keeps building.

BlackRock is putting heightened pressure on companies to disclose more emissions data ahead of annual shareholder meeting season.

Chart of the Week

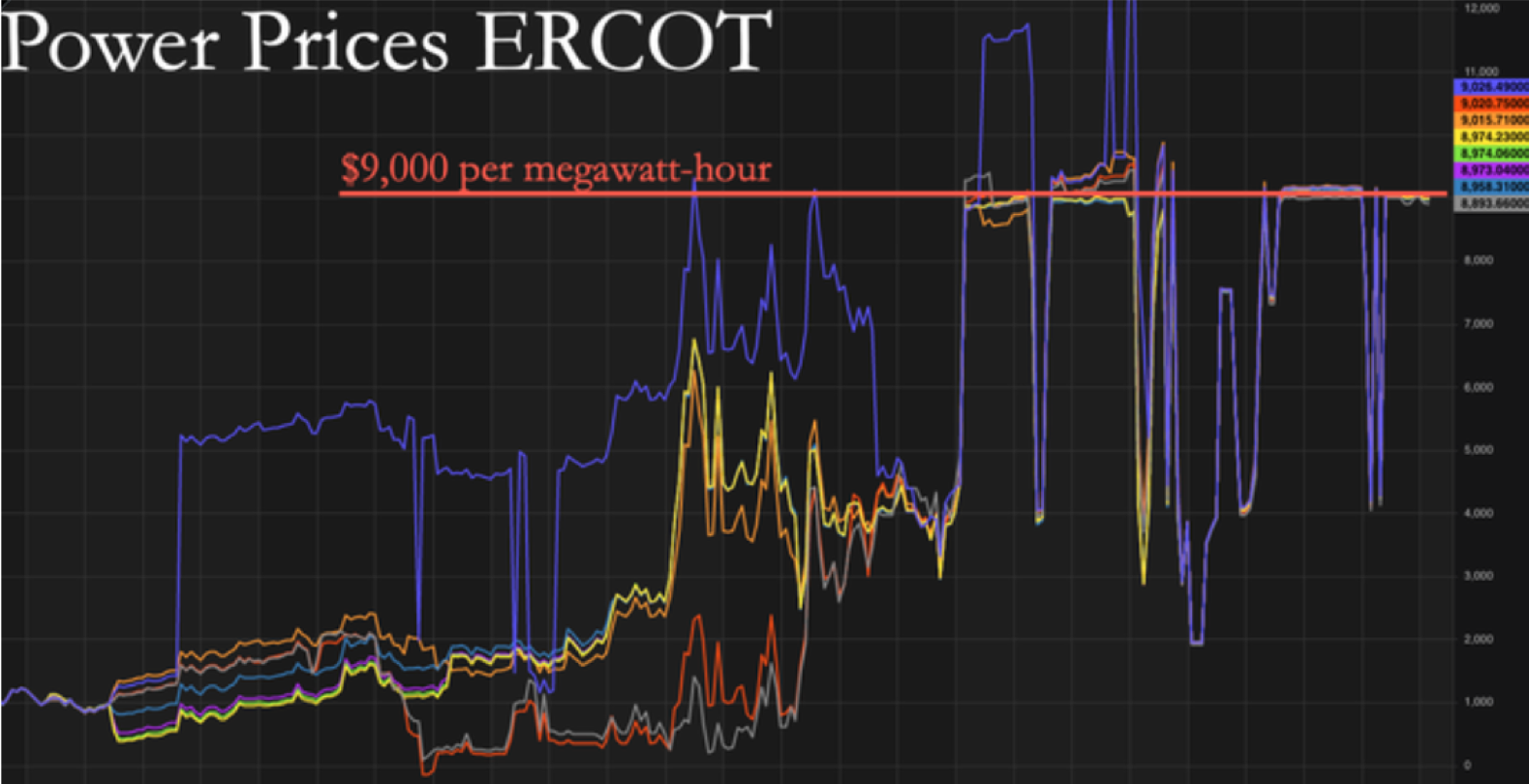

An unprecedented snowstorm swept across the middle United States this week, hitting Texas & its strained power grid the hardest. Statewide blackouts have now been in effect for multiple days, revealing the fragility of the power market when unexpected disruptions occur. Unlike oil or natural gas, electricity can’t be stored for future use, making the market for power highly volatile & trading short term in nature. Below chart shows how the spot power market reacted to the chaotic winter weather - ERCOT is Texas’s regional power grid:

(Source)

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Bitcoin.