A Legacy Guy Considers DeFi

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

Until now, this newsletter has concerned itself with market structure issues of the present. From a history of its main characters to the misunderstood features of its setting, I’ve set out to help readers become smarter & more informed about exchanges, their customers & biggest partners, because I believe they’re severely under-followed. This industry is defined by a handful of companies that control powerful centralized platforms, and have leveraged these platforms to make their owners wealthy for decades.

Market structure is changing. Its main characters & setting will likely look quite different a decade from now, because disruption is looming. After spending quite a bit of time in research & considering the state of the industry, I believe this disruption will come in large part from DeFi - decentralized finance. The farther I fall down the DeFi rabbit hole the more I’m reminded of the popular show Game of Thrones - legacy exchanges may soon find they’ve been squabbling over today’s Iron Throne while ignoring DeFi, the industry’s White Walker.

What exactly is this looming disruption? Why should the centralized powers at be wake up to the DeFi disruption already underway? I’ll answer these questions and more by telling the fascinating story of Uniswap, a DeFi poster child with an army of loyal users, powerful backers & dramatic rivalries after only three years in existence.

We begin in July 2017:

You Should Try This Ethereum Thing

The events that led to the birth of Uniswap began when Hayden Adams lost his job. After graduating from Stony Brook University in New York, Adams took a job at Siemens as a car engineer. Less than a year later, he was let go. At 23 years old, living with his parents and now without a job, Adams entered an aimless season of life. “From a perspective of ‘I don’t know what I’m going to do with my life,’ it was scary at the time” Adams recounts in an interview.

With newfound time on his hands, Adams was persuaded by former Stony Brook classmate Karl Floersch to study a then little-known cryptocurrency called Ethereum. At the time, one Ethereum token traded for ~$200. Adams bought a few coins and began learning to code in Javascript & Solidity, languages needed to interact with & build applications on the Ethereum blockchain. The pair’s interest in the still-nascent world of DeFi intensified when the first crypto craze of 2017 sent their Ethereum holdings soaring in value by as much as +200%. Adams & Floersch soon realized they had a head start in an industry where global interest was only just beginning to swell.

To test his newfound knowledge as an Ethereum developer, Adams began creating smart contracts & exploring their potential use cases. When you hear the word “smart contract”, think advanced blockchain code. Smart contracts are a key feature separating the Bitcoin & Ethereum blockchains and are what make Ethereum the developer’s protocol of choice. Bitcoin’s value lies in its use as a payment network, allowing the storing & trading of cryptocurrency with no need for long processing times, censorship or intermediaries. Ethereum’s value as a blockchain is arguably greater than Bitcoin’s because it allows the storing & trading of more than just cryptocurrency.

Using smart contracts, users can link ownership of something to a coin & allow that coin to be traded freely. For example, NFTs exist because of smart contracts - Ethereum developers link ownership of anything from autographed tweets to musical albums to Michael Jordan GIFs into a token, which can then be auctioned off & traded from person to person.

This idea of transferring ownership via the blockchain is extremely powerful. Today we trust centralized exchanges & intermediaries to transfer ownership of assets for us, paying hefty commissions & fees to ensure trades are executed & processed as ordered. If we can do the same thing using the blockchain, without giving up control of our assets, what long term value does legacy market structure really bring?

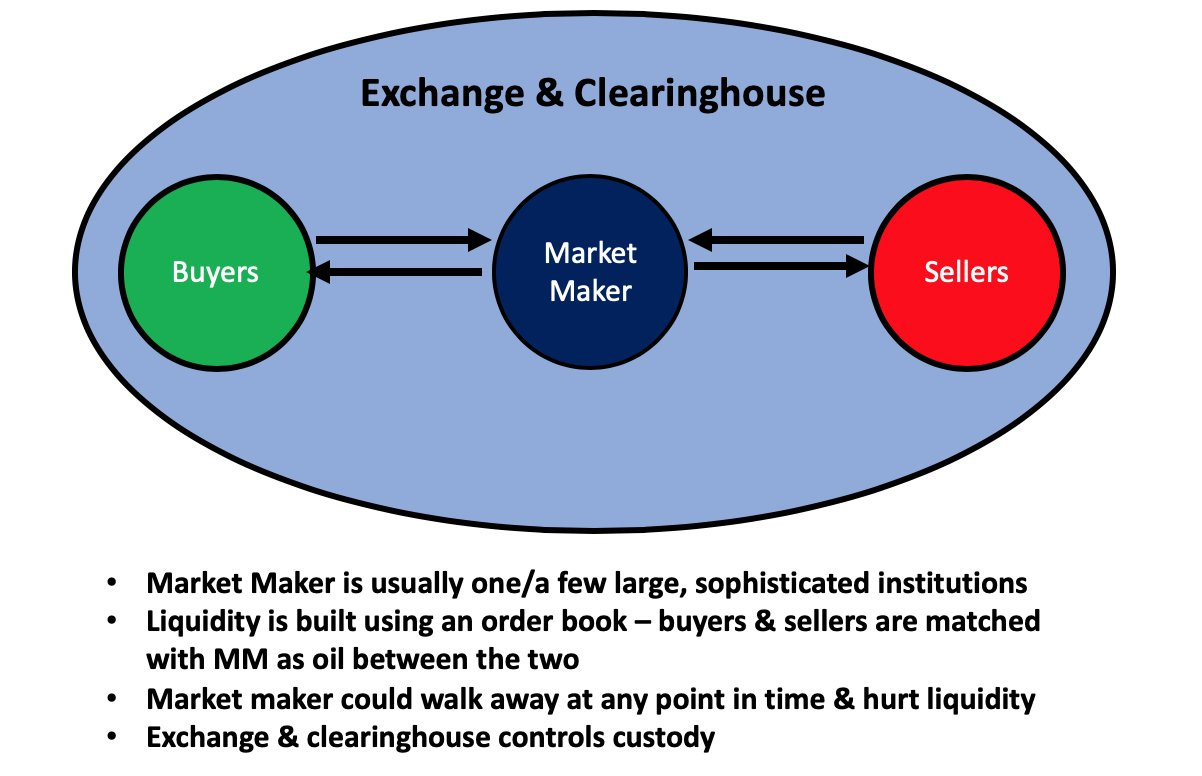

Adams’ research into smart contracts became focused on their use in building a completely decentralized exchange. He had cracked the control piece of the puzzle, but a key question remained - how does a decentralized exchange create liquidity? Successful exchanges give traders large & small the ability to buy & sell assets without drastically affecting that asset’s price. They do this by maintaining an order book of buyers & sellers & incentivizing market makers, normally sophisticated institutions, to stand in the middle & match between the two.

(Source)

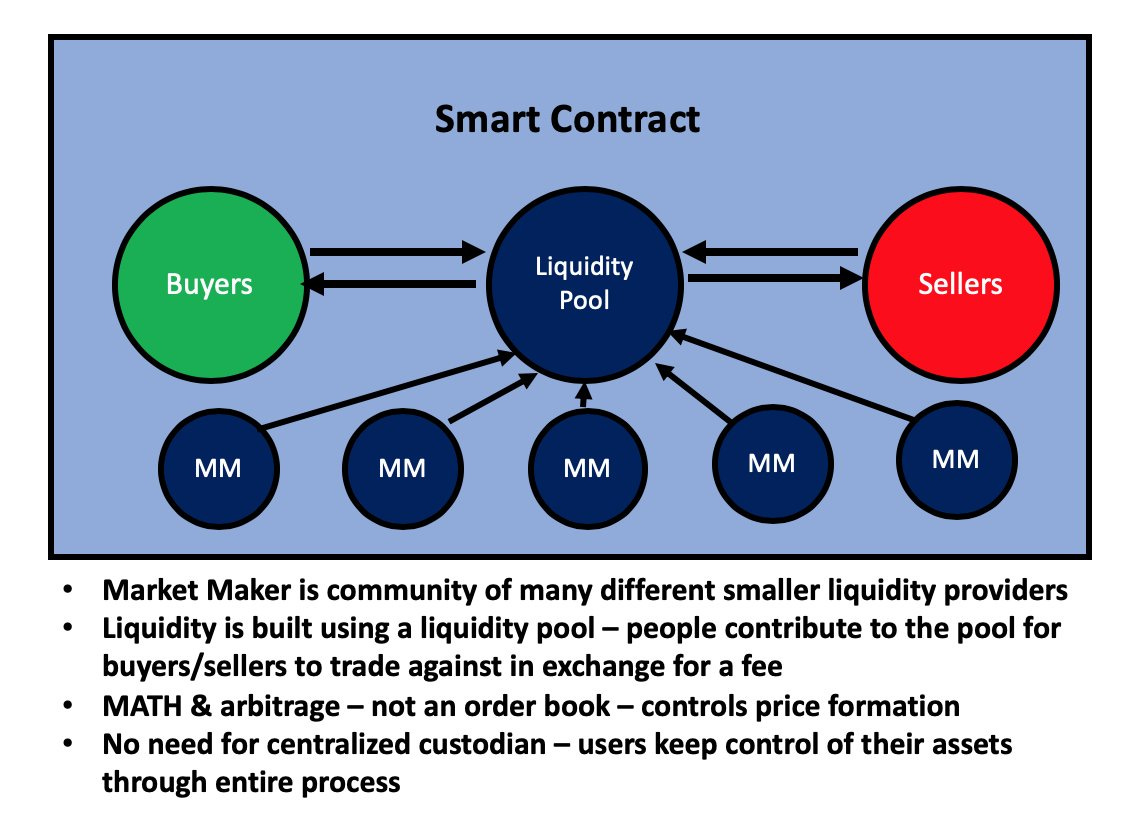

To try and replicate this using the blockchain, Adams went to the best resource he could think of for help - the Reddit boards. There he found a year-old post on r/ethereum describing a new way to incentivize liquidity, called automated market makers, or AMMs. Instead of an order book with centralized market makers in between, smart contracts can collect liquidity from many smaller providers into a larger pool that traders interact with. Price formation happens not with an order book but with a mathematical formula - as liquidity is exhausted in a particular pool, it becomes more expensive to transact with that pool. I won’t go too deep into the nuts & bolts of AMMs in this post, but those looking for more detail can fall deeper down the rabbit hole here.

(Source)

The AMM model took the already considerable utility of smart contracts and expanded it a hundred-fold. Think of AMMs like YouTube for liquidity. With YouTube, anyone can record a video, upload it to their channel, and have the potential to be seen by billions of people. YouTube democratizes television.

With automated market makers, anyone can post liquidity to a decentralized exchange & grease the wheels of market structure, with the potential to profit in the process. AMMs are democratizing liquidity provision.

DeFi Summer

Throughout the spring & summer of 2018, Adams perfected his AMM prototype & began sharing his work with the crypto community. To keep the project alive he received grants from the Ethereum Foundation and was mentored by some of the industry’s early pioneers. After many months of iteration & improvement, Uniswap was finally ready for the real world. V1 of the exchange was deployed to the Ethereum mainnet on November 2, 2018, a little over one year after Adams was laid off from Siemens.

What follows can only be described as a smashing success for Uniswap & its growing community. Scores of users began flocking to the exchange to both provide liquidity & trade an expanding list of available token pairs. Interest in Uniswap V1 came from three core strategies:

DeFi developers who’s projects needed to list their own tokens or access existing tokens could easily use Uniswap to find willing buyers & sellers.

Early crypto adopters could trade certain tokens long before they became listed on a centralized exchange like Coinbase. If people were willing to post liquidity for a token, a market was formed. No central approval was needed.

Other traders could make riskless profits by arbitraging price differences between Uniswap and other exchanges listing the same token.

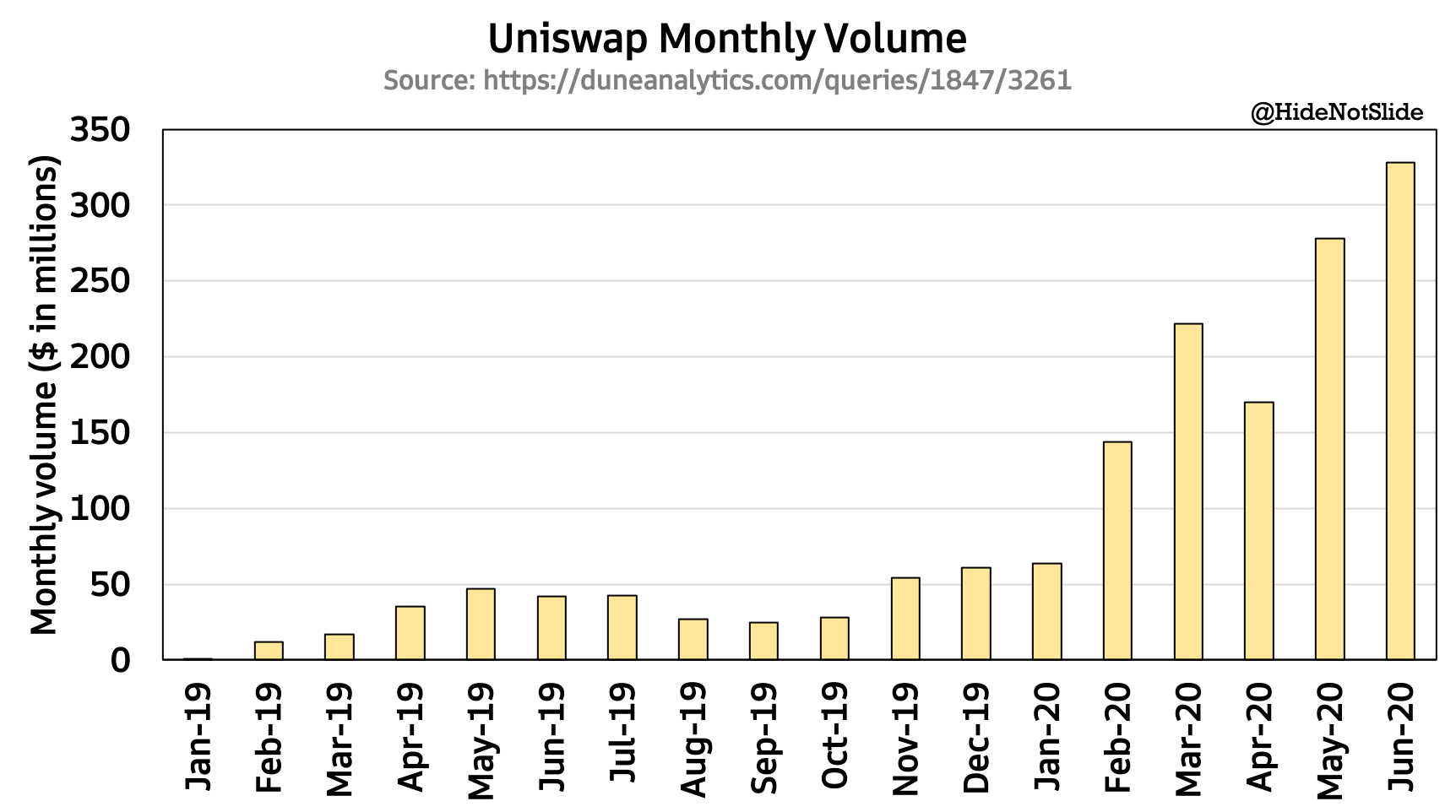

By June 2020 Uniswap was sporting nearly $350 million in monthly trading volumes:

(Source)

Then things got REALLY crazy.

First, In May 2020 Hayden Adams and his growing team of developers released Uniswap V2, bringing more flexibility & new trading features to the platform.

Second, competing DeFi exchanges began to spring up & tried to take market share from Uniswap by offering liquidity providers rewards for switching. Rival exchange Curve saw a spike in volumes when DeFi lending protocol Compound Labs minted its COMP token early that summer. SushiSwap, formed by an anonymous developer called “Chef Nomi”, launched an exchange in September with code & design specs identical to Uniswap’s & a reward token of their own. Even centralized exchanges were getting in on the action - PancakeSwap, an exchange built by anonymous developers on a Binance-controlled blockchain, became popular for lower gas fees & its SYRUP reward token (I don’t make the names…).

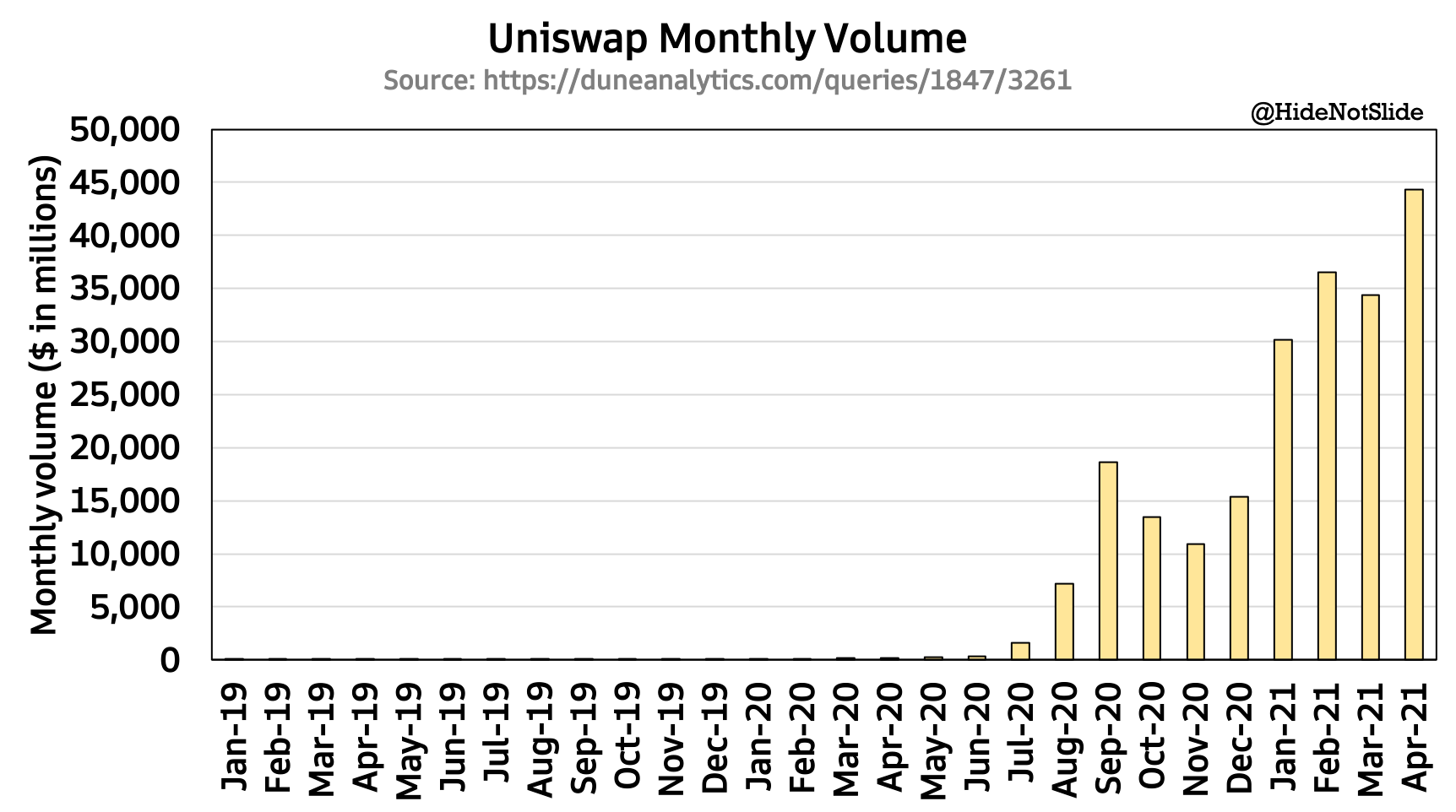

In retaliation, Uniswap launched & distributed its own reward token to its community, dubbed UNI. The term “yield farming” became used to describe the rush of traders chasing these rewards, bringing a tidal wave of interest into DeFi’s atmosphere. By the end of 2020, Uniswap was trading over $15 billion in monthly volume, +4,500% higher than its June 2020 pace. 2021’s pace is greater still:

(Source)

In spite of intense competition, today Uniswap remains the largest purely decentralized exchange in the world (PancakeSwap is now technically bigger, but isn’t fully decentralized… I’ll save that rabbit hole for a future post). Uniswap has now raised millions in venture capital funding from Andreessen Horowitz & other prominent investors. For a couple months in 2020, Uniswap traded more volume than Coinbase, the largest centralized crypto exchange in the US with its blockbuster direct listing only a few weeks ago. The global DeFi movement is taking not just the crypto world, but the traditional finance world by storm, with Uniswap as its chief standard bearer.

Where We Go From Here

After re-emerging from the rabbit hole, I believe decentralized exchanges mark the biggest disruption to legacy market structure since electronic trading. Uniswap’s grassroots liquidity model is working despite largely retail users, high Ethereum gas fees & minimal non-crypto use cases. If innovations ceased from this point forward, Uniswap would likely continue to thrive in its small, retail crypto corner of finance.

Innovations, however, aren’t ceasing. In May 2021 Uniswap is set to release V3 of its platform, which comes with radical improvements to its liquidity model. In Uniswap V3 automated market makers are expected to look much closer to an on-chain limit order book, where liquidity can be focused on specific prices rather than passively available at all times. I believe this upgrade will bring another big boost to trading volumes, this time from large institutions rather than armies of retail users.

Additionally, I believe non-crypto use cases will materialize over time. Today Uniswap and the crypto space in general suffers from something called the Oracle Problem, which simply means blockchains can’t interact with a non-blockchain system by design. A system built on the Ethereum blockchain has a hard time incorporating the daily price of a non-digital asset into its process, for example. The Oracle Problem is what’s keeping an innovation like automated market makers from impacting traditional finance in a big way.

I expect the industry to find workarounds to the Oracle Problem & end up treating tokens much like a derivative. Plenty of traditional exchanges make boatloads of money letting users trade cash settled futures contracts for things like oil, corn, sugar, and even Bitcoin. These markets never get anywhere close to the physical product they’re trading but still boast deep liquidity & the world’s biggest institutions as their customers. Why can’t Uniswap use tokens in a similar manner down the road?

Imagine if the S&P 500 Index was linked to an Ethereum token. Users could post liquidity to the S&P 500 AMM pool & trade this token on Uniswap. Arbitrageurs would ensure this token traded in line with the S&P 500 tick for tick. Owners of this token would have no direct or indirect ownership of any company equity, but could profit off the index’s movement nonetheless, just like traders of the CME futures contract. While not a reality today, a token-derivative market like this could theoretically exist in the near future, giving Uniswap & decentralized exchanges as a whole a wide swath of new use cases.

To be clear, I’m still a legacy finance guy. Uniswap has a long way to go before it can challenge the likes of CME or the NYSE in trading volumes or valuation. Uniswap’s transaction costs & collateral needs are still quite high & its use outside of the digital world remains lacking. However, I’m done ignoring DeFi’s contribution to market structure & the massive opportunity Uniswap has to upend the way legacy exchanges do business. I expect more fireworks this summer following the rollout of Uniswap V3, and am long a small amount of the UNI governance token with a cost basis of ~$32.

Wall Street should ignore Uniswap & decentralized exchanges at their own risk. They may not be able to drown out DeFi’s growing drumbeat much longer.

Honorable Mentions

It’s earnings week! CME, ICE, CBOE, Tradeweb, S&P Global and Moody’s all reported earnings this week with varied levels of performance & market reaction. Exchange businesses faced poor YoY comps against Q1 2020 that saw the most volatile market since the GFC. Market data businesses fared much better on average as all-time equity market highs boosted index revenue & a post-COVID Wall Street recovery helped data subscription sales. Next week’s newsletter will be focused on a deeper dive into Q1 earnings and my thoughts on each company & stock going forward.

Speaking of ICE, during Q1 earnings the company announced they sold their entire stake in Coinbase (~1.8% of the company) for a pre-tax profit of $1.2 billion. The gains are expected to be recognized in Q2 of this year.

Deutsche Borse and Commerzbank announced a €10 million investment in 360X, a fintech startup building marketplaces for NFT art & real estate. The exchange says plans to launch other digital assets on the platform are also in the works.

Chart of the Week

We’ll round out this week’s newsletter on the crypto train by taking a look at CME Ethereum futures performance. Since launching in early February 2021, Ethereum futures saw modest activity until April, when volumes nearly quadrupled month-over-month. A new record of 5,469 contracts were traded on April 22, representing more than $650 million of notional. Remember, CME is a predominantly institutional exchange with large contract sizes & customer accounts.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Bitcoin, Ethereum and Uniswap’s UNI governance token.