Recapping Last Week's Stock Market Boxing Match

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

Last week saw the explosive re-emergence of a debate that’s been heating up for a decade now, moving from the small, out of the way market structure arena into the mainstream media & halls of Congress.

First it was a Financial Times opinion piece from Alex Gerko, the billionaire founder of HFT firm XTX Markets: “Retail trading frenzy reflects ‘broken’ US equity markets, says XTX’s Gerko”. Then it was a public speech by SEC Chair Gary Gensler, where he struck an aggressive tone on the topic of market maker concentration, saying it “can deter healthy competition and limit innovation” and increase system-wide risks. Shares of Virtu Financial immediately sank -10% as Gensler’s comments were digested.

In response, Virtu CEO Doug Cifu appeared on CNBC to tell his side of the story. He argued that US equity markets are as efficient as they’ve ever been & that his firm provides billions of dollars in cost savings to retail investors, over and above what regulators require. Virtu followed up the appearance with a presentation showing how little credit the firm gets for the risk it takes on & the services it provides to investors.

Gerko fought back with another opinion piece. Both CEOs continued the fight on Twitter. The word “securities fraud” was used at one point. Quite an eventful week for equity market structure folks indeed!

Today I want to try and explain what these firms are arguing about, each side of the debate, and what I think about it all. It’s not every day that two high profile trading firms share their views on a widely-followed industry topic, which signals to me that more fireworks could be coming. A couple disclaimers before I dive in:

I own shares of Virtu Financial.

I am not the #1 expert on this topic, and I may get some points or opinions wrong while explaining everything. I welcome genuine questions & feedback.

Background

In 2005 the SEC passed a massive set of changes to the US equity markets via Regulation NMS. Reg NMS requires brokers to execute client trades at the best price, defined by the SEC as the National Best Bid & Offer, or NBBO. If the best available price for a stock happened to be quoted on the NYSE, brokers were forced to send their trades to the NYSE. If it was on Nasdaq, brokers had no choice but to trade there.

Despite the SEC’s mandate, not all trades are executed at the NBBO. The NBBO only covers certain trade sizes and, most importantly, only covers public exchanges. If someone were to route their trade to an off-exchange venue like a dark pool, they could get better execution than what’s on a public, or “lit” exchange.

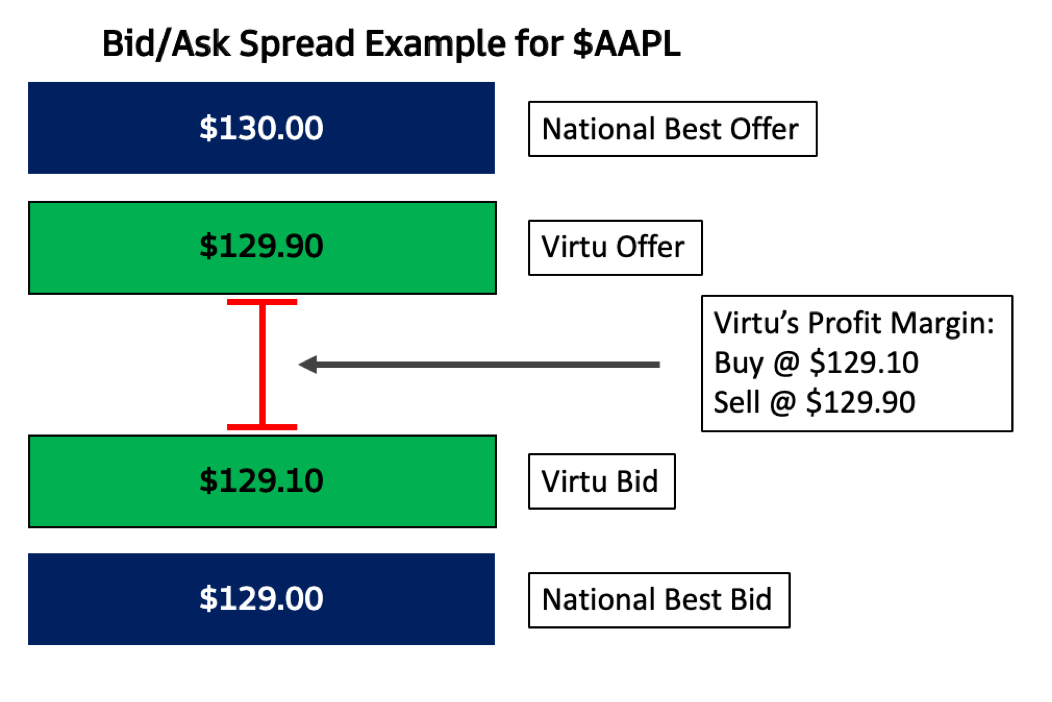

This is where wholesalers like Virtu & Citadel Securities come in. They take order flow from a variety of brokerages and execute trades at or better than the NBBO. If for example the best price to buy Apple on a lit exchange was $130.00, but Virtu could fill the same order at $129.90, brokers who route to Virtu could save $0.10 per transaction for their client. Or on the flip side, if the best price to sell Apple was $129.00, but Virtu could offer $129.10 for the same order, Virtu becomes the more attractive execution option. This is called price improvement. Similarly, rather than offer $0.10 in execution cost savings, Virtu could simply pay the broker $0.10 to execute their order at the NBBO. This is called payment for order flow.

Off-exchange activity has exploded in popularity since Reg NMS. As of 2021, nearly half of all equity transactions happen off-exchange, including most retail trades.

Many in the industry argue Reg NMS has caused equity markets to become more complex, fragmented, and exposed to manipulation, with 2021’s meme stock drama as a perfect example. Major changes seem to be on the horizon, but what should those changes be?

In One Corner - Gerko & Gensler

With the above setup in mind, XTX’s Gerko & SEC Chair Gensler weigh in with the same general opinions:

The wholesaling business is too consolidated among the top market makers, mainly Citadel Securities & Virtu.

Brokers & market makers have gamified the market to earn higher profit margins at retail’s expense.

If you recall a post from earlier this year - Bernie Madoff’s Parting Gift - I explained why retail order flow was so valuable for a market maker. Institutional traders can see the market’s core order book and know when short term supply/demand imbalances will move a stock. Retail traders won’t run away at the first sign of an order book imbalance and trade in small size, making them less risky to execute. Today wholesalers trade most retail volume in the US and get the benefit of taking the other side of this “uninformed flow”, as evident by their stellar earnings results:

Citadel Securities Reaps Record $6.7 Billion on Volatility

Virtu Reports Q1 ‘21 EBITDA Of $565 Million After Record 2020

Gerko argues that transaction costs would be lower if brokers routed retail trades to a public exchange rather than one of these two market makers. Doing this would give other firms - like XTX - a way to compete for this order flow. Today Gerko’s firm doesn’t have a chance to compete with Virtu & Citadel Securities because retail trades never land on a lit market. If they did, XTX could try and offer better prices than competitors to take market share, benefiting the end user in the process.

The other opinion shared between Gerko & Gensler is the gamification of markets, whereby retail customers are drawn into speculation with free trades, addictive app design, and easy access to both leverage & complex trading products. These incentives are attracting users into increasingly volatile “meme stonks”, which tend to have wide bid/ask spreads & the most profit potential for market makers. Gerko highlights this as a conflict of interest - brokers treating market makers paying for order flow as their primary customers rather than retail users themselves. Eliminating payment for order flow, in his opinion, would help end this conflict & make retail execution the top priority.

In The Other Corner - Wholesalers

To argue the opposite side of the debate there are just a few wholesalers to choose from, and only one - Virtu - is a public company. Which leaves CEO Doug Cifu as the sole public face of the market maker community.

Cifu’s argument is this: everyone needs perspective. The SEC needs perspective. The mainstream media needs perspective. Retail investors need perspective. Cifu said it best during his CNBC appearance:

“Any investor in this country can pick up a smartphone of any type, and for no money get a better execution than just about any institutional investor… it’s phenomenal what has happened.”

Revisiting the bid/ask diagram above, Virtu executes most retail orders within the NBBO, which represents the best prices a lit exchange can offer. Institutional customers are mostly executing on a lit exchange, and retail almost always gets a better price with the wholesalers. From a retail investor’s perspective, the equity markets have gone from an expensive, slow, guarded experience to one that is fast, convenient, and cheap to access. With the advent of decimal stock prices & record amounts of trading volume, bid/ask spreads have been tighter than any other point in history. Are markets perfect? No. Have they improved tremendously in the last decade? Cifu would say absolutely.

Another point Cifu believes is in need of perspective - how much competition really exists in today’s equity market. Sure there’s concentration among wholesalers, but brokers have never had more options when it comes to routing orders. There are now 16 lit US equity exchanges and more than 50 dark pools competing for the same retail orders as Virtu & Citadel Securities. Why do wholesalers win? Executing on an exchange normally comes with some form of an exchange fee - the price of accessing that venue’s liquidity. Wholesaler execution is free, and in some cases they’ll even pay the broker for the privilege of executing their order. When choosing between paying a fee to trade vs. getting paid to trade, the latter option wins almost every time. Virtu & Citadel Securities get most retail flow because they provide the best price in today’s environment. Exchanges can’t really compete.

How can wholesalers offer free execution & still make boatloads of money? The key difference here is who’s taking risk. An exchange does not take the other side of every equity trade - they incentivize market makers to do this for them with rebates & other rewards. Wholesalers cut out the middle man & execute orders themselves, without having to provide the same service on an expensive exchange. If their matching engines implement buggy code or they mis-manage their inventory of stock, market makers could lose a lot of money very quickly. The bid/ask spread compensates them for taking on & managing this risk.

Cifu’s point here is that wholesalers provide a valuable service & they do it better than a long list of competing venues. Why punish them for giving retail the best deal available?

Closing Thoughts

After digesting each argument, I think both sides can be equally right. Does payment for order flow put brokers in a position where conflicts of interest can happen? In some cases, yes. Are retail investors currently getting better execution than anyone else in the market? Yes. Would lit markets be healthier if retail flow was executed on exchange? Yes. Would transaction costs likely go up if that happened? I believe so. The equity market is extremely complex & leaves plenty of room for subjectivity. There’s never a clear-cut proposal that would immediately fix every problem or benefit every party.

Here are some of my thoughts on what changes need to happen:

Brokers need more accountability for advertising the stock market like a video game. Retail participation in the US stock market has radically changed since 2020 - many first-time investors now view the market as a short-term gambling vehicle rather than a long-term investment vehicle. Gambling and speculation is a drug, and brokers benefit when more people become addicted to this drug. It needs to be more difficult for retail & first-time market participants to get access to margin & options accounts, and the broker- engineered dopamine hits from short-term trading & excessive speculation need to be addressed.

The NBBO needs an update. Despite vehement disagreement on some points in last week’s debate, nearly everyone could agree on one thing - the NBBO is a slow, outdated, flawed way to measure the US equity market. As more of the market begins to trade at a different price than the official NBBO, the NBBO itself becomes a fake signal of where stocks really trade. If this benchmark were updated to include more trade sizes & venues, it would help simplify everyone’s view of the market and could help improve competition.

Regulators need to expand their view of the problem. Brokers aren’t the only ones responsible for promoting the market as a casino. Social media has a massive influence on retail participation - today more Millennials get financial advice from Reddit & TikTok than from licensed professionals. Demand for the stock market gambling drug has exploded, and it’s impossible to change demand for a drug by targeting its supply. I don’t believe retail traders are YOLOing in stocks like GameStop or AMC because Virtu pays Robinhood $0.10 for its order flow. I think they’re trading GameStop & AMC because CrazyApe69420 posted a viral funny video disguised as “research” on these stocks that people want to connect with. Changing execution costs won’t change a thing about CrazyApe69420’s video or the gambling demand that video creates.

Hopefully this recap helped put some headlines in context. I’m expecting more fireworks & potentially massive regulatory changes on the horizon - here’s to the hope that it helps the US stock market remain a fair & attractive place for global capital.

Chart of the Week

To those who thought the options market chaos was over…

May 2021 was the fourth highest volume month of all time after falling from record highs earlier this year. A continuation of the GameStop & now AMC meme mania likely boosted activity. Interestingly enough, the steadily increasing trend in options volume since January 2020 has so far remained intact.

Exchange stocks that benefit from this trend include Nasdaq, CBOE, ICE and Virtu:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, COIN and VIRT. I am also long Bitcoin, Ethereum and Uniswap’s UNI governance token.