Options Are Eating The World

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

The New Biggest Game In Town

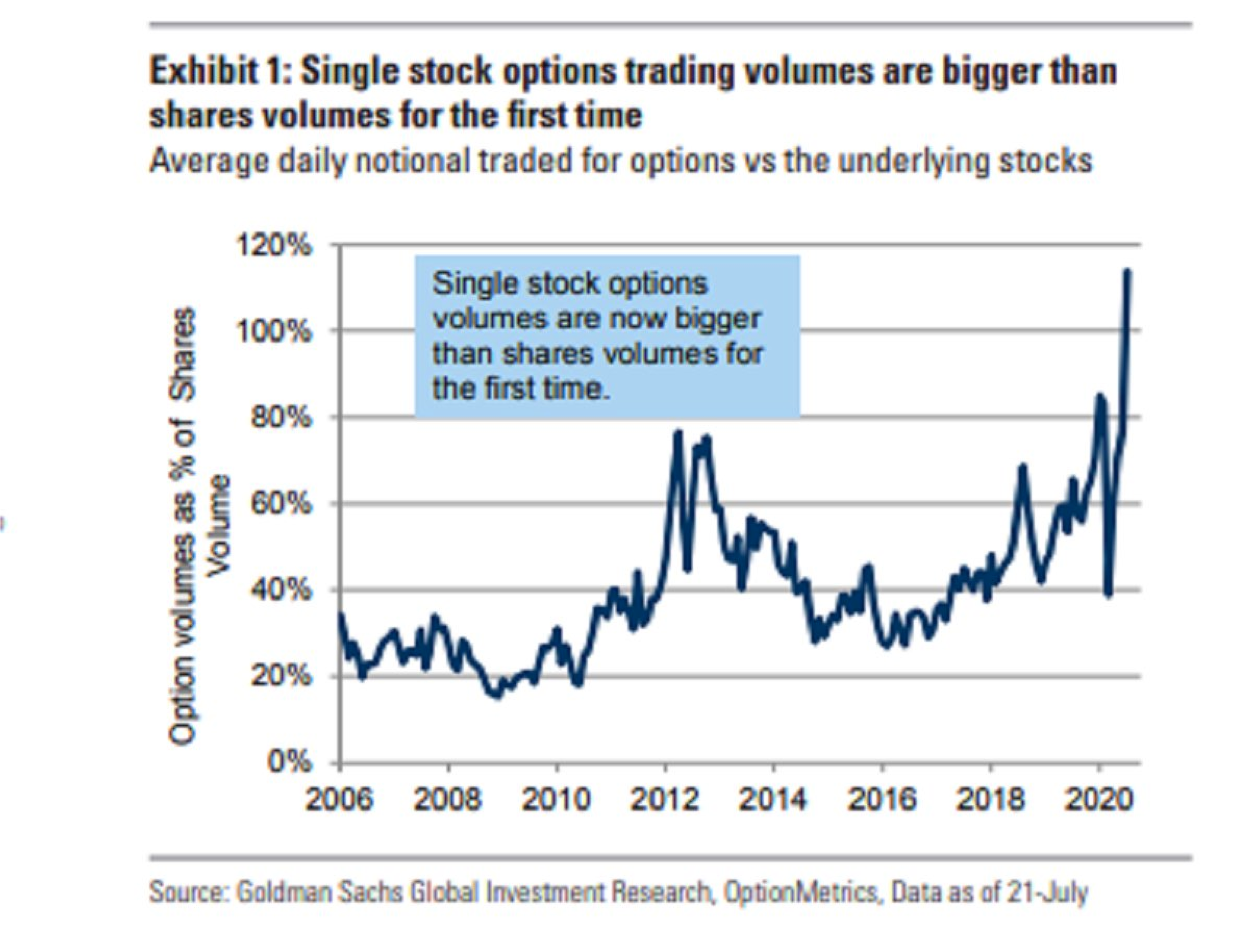

In late July of this year, Goldman Sachs published an eye-opening chart confirming feelings of rampant speculation on Wall Street - the options market had surpassed the stock market in size for the first time on record:

(Source)

With more media outlets & serious investors talking about the impacts of the ballooning options market on stocks, I wanted to pen a review as it relates to exchanges. How did we get here? Why does this matter? What happens next?

We begin in ancient Greece.

The first recorded options trade comes from an Aristotle book, written in the 4th century BC, about fellow philosopher Thales of Miletus. Thales used his background in astronomy and mathematics to predict an unexpected large olive harvest the following summer, and wanted to profit off this information. He paid olive farmers for the right to use their pressing equipment for the next year; when the large harvest did materialize, Thales exercised his contract and made a sizable profit.

Options contracts have been in use for thousands of years, but historically only on the edges of mainstream finance. Trades only took place over-the-counter and were largely unregulated. The 17th century Tulip Mania bubble saw options contracts in high demand by both merchants who needed to hedge their exposure and average investors drawn to the allure of a quick profit. Many lost everything in the succeeding market crash, and not everyone could pay off their debt when the dust settled. Because of this options drew a bad reputation as an instrument of pure gambling and were even banned in parts of the world for many years.

In the US, options trading made its way into the public eye not through regulated exchanges but through firms known as bucket shops. In the 1870s advances in ticker technology allowed stock prices to be communicated quickly across the country via telegraph. Small brokerage houses began to pop up with offices where people could come and make bets on the movement of those prices. The only difference between bucket shop betting and actual trading was bucket shop wagers never impacted a stock’s price and never made their way onto an exchange. Bucket shops opened the market up to a wide base of retail customers without the money to trade through a broker, who were now able to place small wagers on stocks with little margin. Popularity exploded across the US as hundreds of bucket shops began catering to the working class, taking out ads in the newspaper & competing with classic brokerages for business. Stock market legend Jesse Livermore launched his career by getting banned from Boston bucket shops after making too much money.

At first exchanges spoke well of bucket shops, even calling them “a sort of democratized Board of Trade”. This tune quickly changed when they started losing market share. The New York Times commented in an 1882 edition that bucket shops were "thriving in all of the large towns and cities from NewYork to Chicago, and that operators who once traded legitimately with members of the Stock Exchange, now operate through them”. The losses hurt exchange volumes by a staggering -80% & cut the value of floor memberships by half in the span of a few years. Bucket shops had to be dealt with for exchanges to survive. Between the 1890s and early 1900s, exchanges pressured telegraph companies to cut bucket shops access to stock quotations, urged lawmakers to tighten anti-gambling laws, and embarked on a public awareness campaign to try and label bucket shops as unethical & illegal. The pressure worked - by 1915 bucket shops were largely banned in the United States, and exchanges had regained their monopolistic power over the stock market.

It wasn’t until the 1970s that options became a full-fledged regulated market, when two separate events brought exchange trading to life. First, the Chicago Board of Trade, then a struggling agricultural exchange, began looking for new growth avenues. In an attempt to add liquidity to their futures markets, they decided to form a dedicated exchange and clearinghouse solely for options trading. They named it the Chicago Board Options Exchange (CBOE), and launched it in April 1973 on the CBOT’s 125th birthday. Only call options were listed in the beginning; puts wouldn’t come to CBOE until 1977.

The second catalyst for the rise of options trading also came in 1973, when Fisher Black and Myron Scholes created the first sophisticated options pricing formula (aptly named Black-Scholes). This formula gave legitimacy to CBOE’s products, and set the stage for a boom in institutional adoption of options trading. In 1974 average daily trading volume in the options market stood at ~20,000 contracts; by 2019, that number stood at ~17.5 million.

Then 2020 happened.

Most of us know the story. A move to free trades by the discount brokers. COVID-19. Stimulus checks. No sports (or sports gambling). r/wallstreetbets. Dave Portnoy.

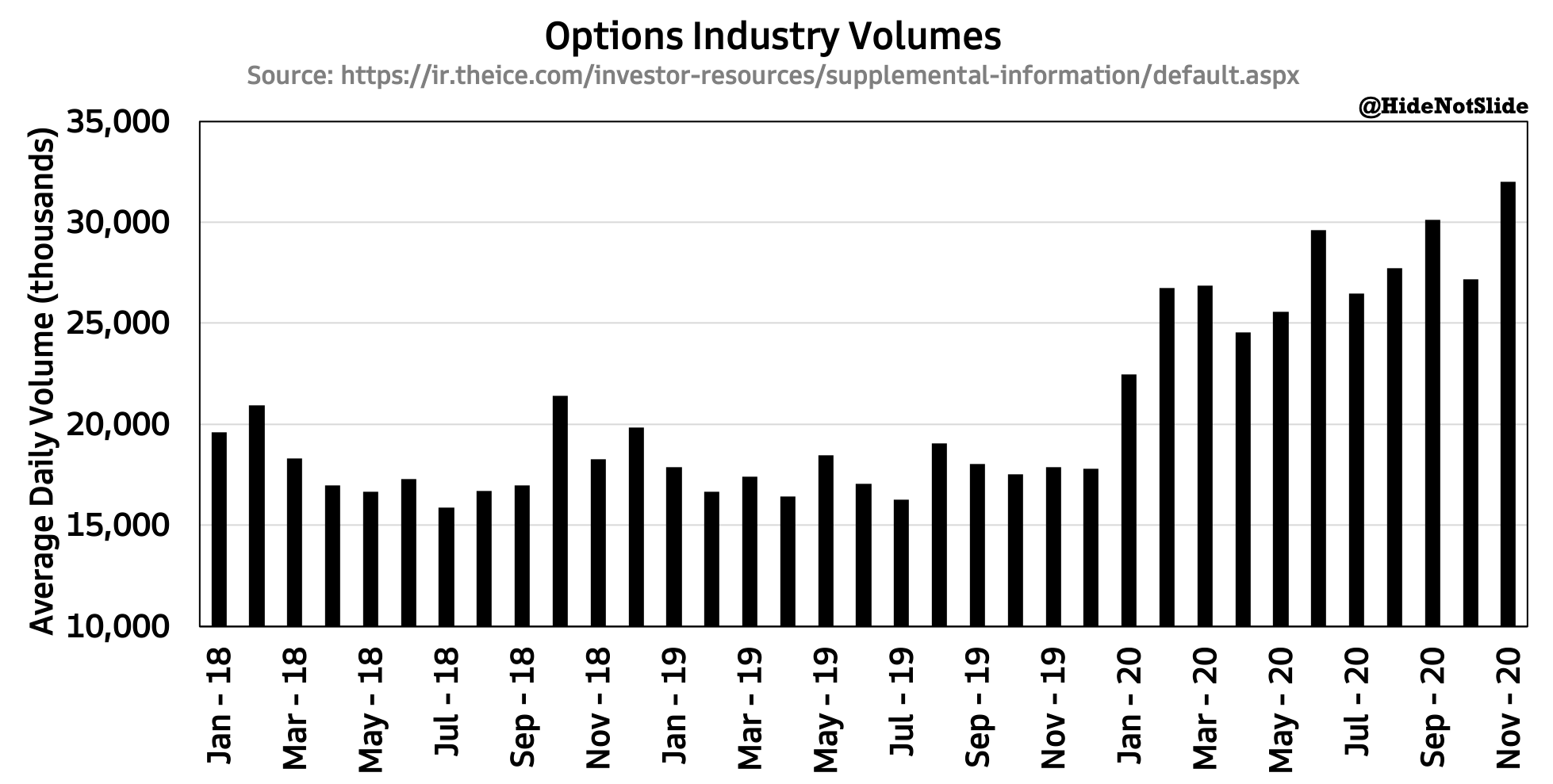

Catalyst after catalyst shoveled retail traders into the options market, pushing volumes to new highs and beyond. January 2020 saw 22.4 million options trade hands per day - a nine year high. February saw 26.8 million. By June volumes hit 29.5 million contracts per day and counting. The pace became blistering.

Many thought things would slow down after the November elections. Sports were back. A second stimulus package was nowhere near done. Even Portnoy CNBC appearances were down. And yet 32 million contracts per day traded in November, a new record. December looks to be higher still.

As the records keep falling, exchanges & analysts who cover them are beginning to adjust expectations about what a new normal looks like. During Nasdaq’s Q3 earnings call, a question came from Wells Fargo analyst Chris Harris:

“Do you think the paradigm has changed for trading in U.S. equities and options? And really, I guess, what I'm wondering is whether you think the volumes that we're seeing in these markets are going to be sustainable. And why, if so?”

(Source)

In response Nasdaq CEO Adena Friedman shared her thoughts with evidence from conversations with industry peers:

“…I think we are seeing a secular shift in getting more younger investors engaged in the market. And I think that could create a more sustainably higher trading environment than with, let's say, what we saw in 2017, '18, '19 kind of time frame.”

These comments have big implications. An options market bigger than the stock market creates more opportunity for “tail wags the dog” situations, where activity in the options meaningfully drives the price of the underlying stock. We’ve seen this with story stocks like Tesla. We’re starting to see this with the broader market. Remember SoftBank’s “Nasdaq whale” saga, where they used immense amounts of call option buying in tech to create a rally? Institutions are starting to place as much (if not more) weight on options dynamics & strategies as on equities.

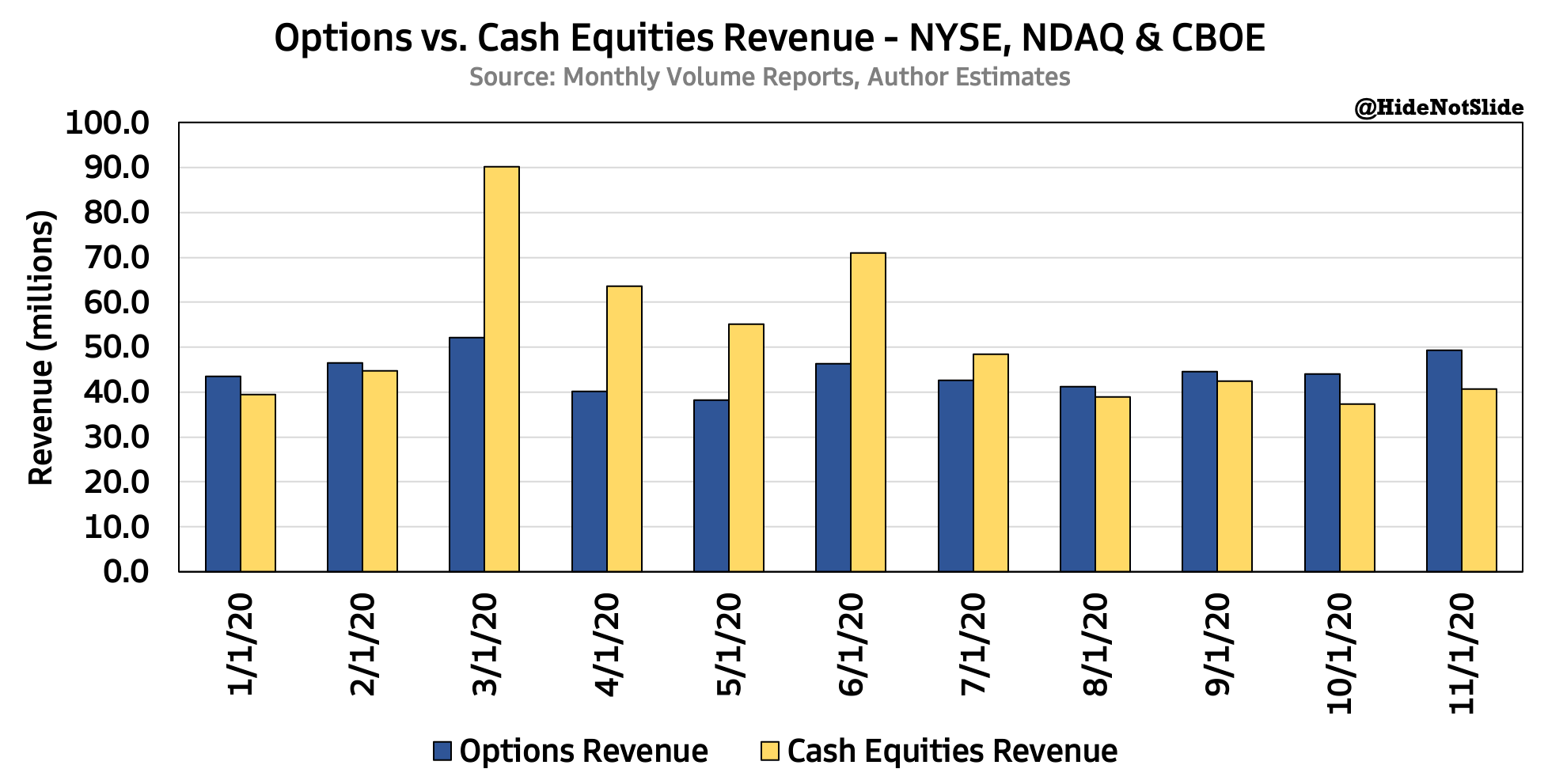

We’ve also seen the tipping point occur where the top exchanges now make more money in options trading fees than in stocks. Below chart aggregates the monthly transaction revenue of the top three players in both markets - NYSE, Nasdaq and CBOE:

The equities market is crowded & competitive. The options market is much less so, with the above three exchanges controlling ~85% combined market share. Nasdaq holds the top spot in options at ~35% market share, with CBOE in second place at ~30% and the NYSE in third at ~18%.

In closing, the options market has come a long way from the olive farms of Greece to its dominant position today. Retail participation has never been higher, and exchanges are preparing for a new paradigm where options volumes are secularly elevated & now a bigger part of their business. Platforms like Robinhood & its competitors are arguably today’s version of bucket shops - cheap ways to democratize access to the markets where novice investors can place wagers on stocks with little money down. Rampant speculation, higher volatility & trading volumes are expected to continue into 2021 and beyond as market friction becomes ever thinner. Options are eating the world, and it doesn’t look like we’re going back to the way things were.

Investor Conferences

We saw most exchanges & market data names give public appearances at investor conferences this week - namely the Goldman Sachs US Financial Services Conference on December 8th and 9th. There are always a few valuable takeaways from management’s public comments - I’ll summarize below:

The Volume Outlook Is Improving - The market is slowly coming around to the prospect of higher inflation after massive fiscal and monetary stimulus this year. Exchanges with interest rate exposure (ICE, CME, Tradeweb, MarketAxess) are mirroring this sentiment with more upbeat volume commentary. CME in particular talked about strength in their longer duration Treasury futures and expressed optimism about a cyclical recovery helping their energy business. If rates volumes do recover, it would pair well with exchange’s booming equity index businesses where retail participation is high and plenty of uncertainty remains.

Slow Evolution in Europe - CBOE and MarketAxess fielded questions about their European strategy and both responses reveal slow industry adoption of new technologies. CBOE faces a challenging buildout of a new European derivatives platform after it bought EuroCCP earlier this year. When asked about the opportunity in Europe, CEO Ed Tilly focused on better technology as the key to better liquidity - going so far as to call the current structure “dial up”:

“Think of a U.S.-based customer or an Asian-based customer that wants exposure in France, but doesn't want the dial up method of looking at a screen seeing an indicative pool having to negotiate a one-off of everybody other than Goldman.

But having to negotiate a one-off price discovery mechanism, they like the U.S. market, where you are one component of many, Alex, that's trying to make the bid offer better. And it's transparent, and it's successful, and it's clickable, and it's all in one CCP. That's the inbound. That's what we're trying to do. We're trying to grow the pie.”

(Source)

MarketAxess opined on European progress from the perspective of growth in electronic trading. Eurobond and emerging market fixed income has seen a slower uptake in market share relative to the US, and CEO Rich McVey pointed to currency complexities and more “relationship oriented” investors as the main drivers.

M&A Is Still In Play - This conference came at an interesting time for the exchange industry, as multiple large deals are currently being integrated and processed by investors - not the least of which is last week’s S&P Global - IHS Markit deal. Each exchange was asked about their thoughts on the deal in some form, as well as their broader M&A strategy. The highlights:

Moody’s directly responded to the S&P deal by saying “the merger doesn't change Moody's competitive landscape that much” and mentioned they’ll look at deals that drive geographic expansion and improve their existing products.

Tradeweb CEO Lee Olesky had a few helpful comments on the M&A front, saying that “the world is consolidating” and that their deals will be focused on geographic expansion, improving technology, and adding the best human talent to their team.

ICE CEO Jeff Sprecher talked about how we’re in a golden age of liquidity - “I'm convinced that right now, a good management team with a good track record and interesting opportunity can raise capital easily”. From ICE’s perspective, the company first must delever after the Ellie Mae deal before looking at more large deals, but Sprecher did leave the door open for more M&A in the future.

Honorable Mentions

CME launched water futures this week to much fanfare as the public tackled existential questions around the financialization of a resource as essential as water. The best article I’ve seen on the launch came from a Bloomberg opinion piece arguing that the market has a long wall to climb before becoming successful. The best assets for futures products are those that are valuable enough to transport and can only be supplied at specific global hubs. Water doesn’t fit either of those criteria - it’s just too cheap and too abundant. Despite the challenges I still see location-specific use cases for the market, and the fact that it’s a cash settled product makes it more accessible to speculators & the retail community.

ICE expanded its board by two seats after closing on the Ellie Mae deal.

MarketAxess integrated US Treasury trading into their broader fixed income platform, opening up the market to more institutional corporate bond clients.

Moody’s announced its purchase of ZM Financial Systems, a provider of risk management software for the US banking system.

Canada’s 2nd largest pension fund became a lead investor in IEX.

Chart(s) of the Week

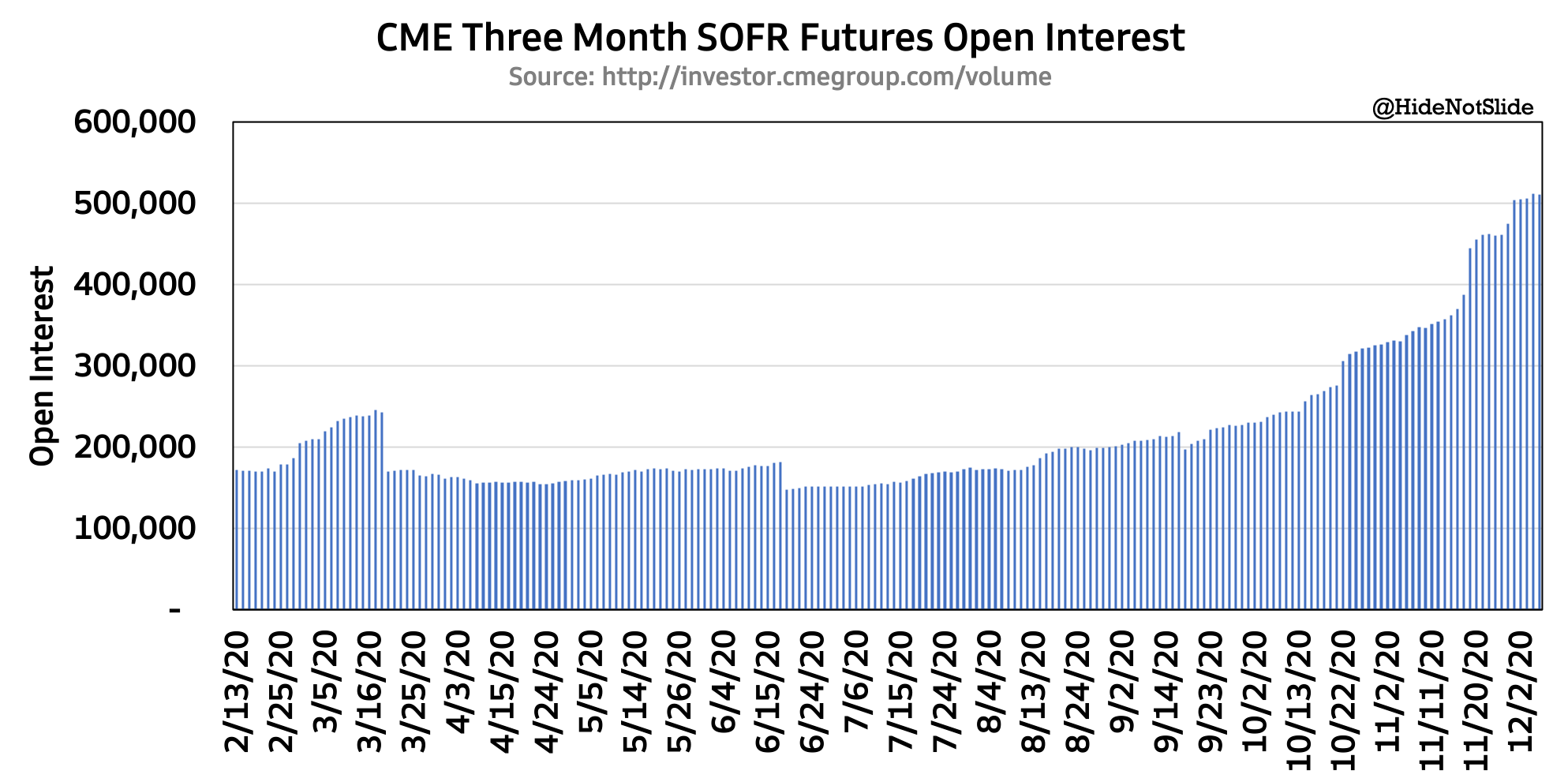

LIBOR transition has been an overhang on the banking & exchange community for a while now, with deadlines seemingly far in the future and policy still in the formation stage. As of this week the apparent end of LIBOR is set to occur by the end of 2021, even with some recent questioning of that date & back-and-forth with regulators.

End of year 2021 is not that far away, and we’re starting to see markets transition ahead of the benchmark. First, CME’s Eurodollar market is at its lowest level of open interest since 2014 and is down 20% from its high - partially because of ZIRP, but LIBOR transition is playing a part.

SOFR, the benchmark of the future calculated by the Fed, has begun its S-curve moment as open interest is up almost 300% from the start of 2020. As the banking community becomes more comfortable with SOFR and more instruments are priced of the new benchmark, OI should only increase with demand for SOFR hedging:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, CBOE, NDAQ and VIRT. I am also long Bitcoin.