IHS&P

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

A Data Deal For The Ages

(Source)

Late on the evening of November 29, the Wall Street Journal reported that S&P Global was in advanced talks to buy IHS Markit for a staggering $44 billion. The story was later confirmed by S&P with a press release the morning of November 30 and a conference call to discuss merits of the deal. If the transaction passes antitrust & is consummated as planned, it would be one of the largest acquisitions of 2020.

Does this deal make sense? S&P Global is an $82 billion data behemoth, comprised of the #1 global credit ratings agency, the Market Intelligence desktop & analytics business, Platts energy market data, and S&P Dow Jones Indices with nearly $16 trillion in benchmarked or indexed assets. Revenue has grown at a ~5-7% pace per year since 2015, with 2020 a particularly strong year for their Ratings business. Revenue is on pace to grow double digits this year, driven by strong debt issuance boosting demand for their credit ratings and greater adoption of passive investing driving AUM to their index products. It’s worth noting that S&P has been active on the M&A front in the past, playing to the narrative of divesting “non-core” businesses to focus on their market data & index units.

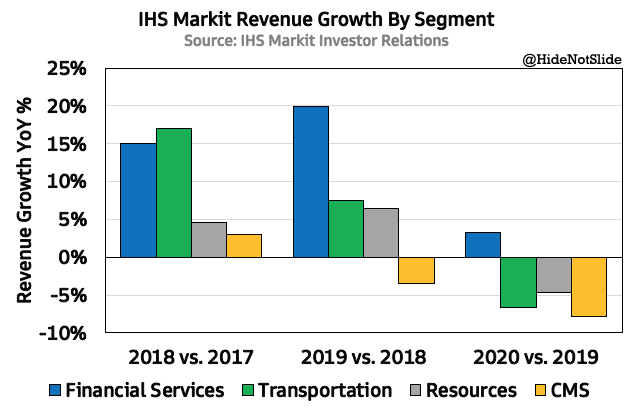

What is S&P Global buying in IHS Markit? INFO made $4.4 billion in their fiscal 2019; 40% of this came from their Financial Services unit, comprised of financial data platform Ipreo, fixed income pricing data & indices, and post-trade/compliance tools for financial institutions. The other 60%, while still in the data business, does not tailor to the financial industry. Other data IHS sells relates to the automotive & energy/chemicals industries, along with patent & product design data focused on the manufacturing sector. The financial products IHS owns have been the growth engine since 2017, with the other cyclically-exposed segments lagging sharply in 2020:

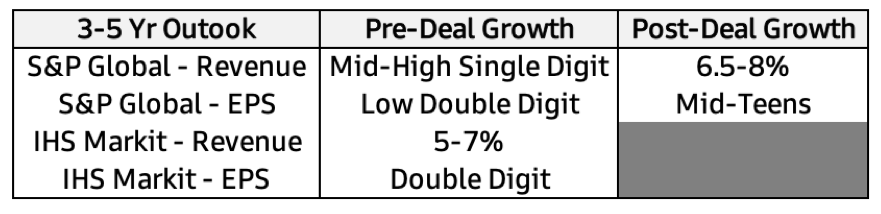

There are overlaps in the two companies that give this deal merit. An integrated Ipreo and S&P Capital IQ would be a juggernaut in the crowded desktop space, with more screen real estate for Ratings & fixed income data to flow to a wider array of customers. Both companies also share large energy businesses that when combined would have a leading position in the industry. This potential for revenue & expense synergies factored into upped growth targets after the deal closes:

(Source)

S&P Global believes they can extract $680M in combined synergies from IHS Markit by the end of 2023, expanding margins of the combined company in the process.

The $44 billion price tag values IHS Markit at ~23-25x EV/EBITDA pre-synergies. Is this expensive? Many would answer in the affirmative. Past research argues M&A above a certain size is unlikely to benefit shareholders, as executing on integration becomes more challenging & the law of large numbers puts a ceiling on future growth. For the exchange & market data industry however, large M&A has become the norm. With such high barriers to entry & entrenched network effects among the competition, many firms are choosing to buy rather than build their way into new markets. We’ve seen this trend play out in spades this year with acquisitions like ICE-Ellie Mae, LSE-Refinitiv, and Deutsche Borse-ISS all making headlines. My guess is investors will overlook the high valuation & give S&P Global management the benefit of the doubt, at least in the short term.

My outstanding questions about this deal are 1) will concessions be needed for this deal to pass antitrust? And 2) Will S&P look to divest the non-financial parts of IHS Markit down the road? Given the size of the deal and S&P’s non-core divestitures in the past, I think both are certainly possible.

Both S&P and IHS Markit traded up on initial news of the deal, but have reversed gains since and are trading flat on the week.

Exchange Analyst Starter Kit

For those who haven’t seen it, I released a bonus post this week where I collected my favorite online resources to learn about exchanges, be it books, podcasts, research papers, and more into one place. You can find that post here:

Exchanges - The New Crime Fighters?

In late September 2020 the ICIJ - a consortium of journalists who first broke the Panama Papers in 2016 - released a new series of reports on global money laundering. The headline? Banks are utterly failing at catching criminal activity, and governments have let them off the hook.

It is estimated that $2.4 trillion in money laundering occurs each year - equal to 2.7% of global GDP. Much of this money flows through the largest banks in the world, and less than 1% of it gets detected or recovered. Banks are slow to flag illicit activity & continue to do business with suspected criminals even after threatened by regulators. Although authorities have punished banks to varying degrees, the rebukes have been in the form of fines & fragile delayed prosecution deals that haven’t changed activity. Money laundering has turned into a huge problem that regulators haven’t been able to impact meaningfully.

I find the ICIJ report interesting in the context of the exchange industry’s recent entrance into the anti-FinCrime arena.

I’ve briefly covered Nasdaq’s recent purchase of Verafin in a previous post. Verafin is a small but fast growing anti-FinCrime technology provider. They make ~$140 million per year in revenue and are growing at a ~30% annual rate. Verafin takes a SaaS approach to money laundering surveillance and compliance - customers pay annual subscriptions to have Verafin monitor & analyze transactions for criminal activity. Because their platform is centralized, Verafin is able to leverage data from one customer to help others on its platform via machine learning. This is important, as anti-money laundering laws do not require a standard compliance process across the industry.

Pre-acquisition, Verafin’s customer base was largely made up of small banks & credit unions with less than $50 billion in assets. Big banks haven’t begun to use Verafin’s services yet, even as spend on AML compliance is only expected to grow.

Nasdaq’s purchase of Verafin, expected to close in Q1 2021, could change this dynamic. The exchange has long, deep relationships with many of the largest banks in the world - other than executing their stock & options trades on the exchange, Nasdaq has contracts in place with these banks for adjacent technology services:

(Source)

I find this acquisition attractive on the thesis that Nasdaq can leverage their current relationships with large banking customers to sell Verafin’s services & improve their machine learning capabilities in the process. This thesis would support an expensive purchase price on first glance - the potential for revenue synergies that only Nasdaq can provide makes the target more valuable.

Regardless of whether Nasdaq can get Verafin’s service into larger banks, regulators need to re-think how money-laundering is policed. If banks aren’t held properly accountable for gaps in compliance, no amount of technology improvement will fully solve the problem.

November Volumes

(Source: Investor Relations websites)

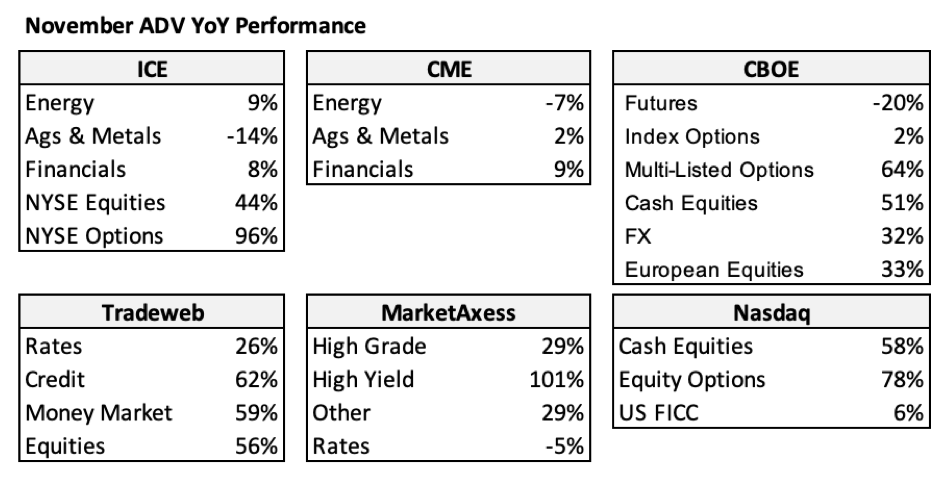

Exchanges reported November volume figures this week with election volatility driving strong growth across the industry.

ICE has outperformed CME in energy futures every month this year but lagged in agriculture & financials. CME saw its financials business grow YoY for the first time since April as equity index strength more than offset softness in interest rates. CBOE’s futures business - almost 100% their VIX market - shrank 20% YoY, but improved month over month.

In the cash equity market, volumes kept crushing historical averages as we’ve seen all year. Election fervor mixed with higher retail participation drove the boost in activity.

The US options market has so far been the star of 2020, and November was no different. Last month’s average daily volume of over 32 million contracts set a new record, surpassing the previous high set in September. We’ve seen an explosion in volumes all throughout 2020, but I think the market is surprised that growth hasn’t slowed down as retail participation stays elevated & the appetite for speculation keeps running hot:

Turning to fixed income - With such high forward multiples, Tradeweb & MarketAxess are pressured to put up stellar numbers every month, and they rose to the challenge again in November.

MarketAxess corporate bond volumes were up +41% YoY with high-yield volumes more than doubling. Electronic market share kept ticking up as well in November with just under 23% of the market now on their platform. Tradeweb’s consolidated volumes grew 37% YoY with impressive growth in swaps and government bonds despite low rates volatility. In my opinion both bond platforms are putting up the numbers needed to sustain their valuations & keep investors happy until Q4 earnings roll around in February.

Honorable Mentions

ICE and CTBC Investments announced collaboration on the launch of two new ESG bond indices.

Nasdaq filed a proposal with the SEC to require listed companies “to have, or explain why they do not have, at least two diverse directors, including one who self-identifies as female and one who self-identifies as either an underrepresented minority1 or LGBTQ+”, as well as publish more detailed & consistent company diversity statistics. Nasdaq Ventures also announced a strategic investment in Matter, an ESG analytics firm.

MSCI reported assets in equity ETFs linked to their indices surpassed $1 trillion in November.

Multiple former BlackRock executives are set to take positions in Biden’s administration, including the National Economic Council and the Treasury Department. This news comes as more attention is given to the growing power of large asset managers in markets & the economy.

LSE is set to get the green light from EU regulators to complete its acquisition of Refinitiv.

Chart of the Week

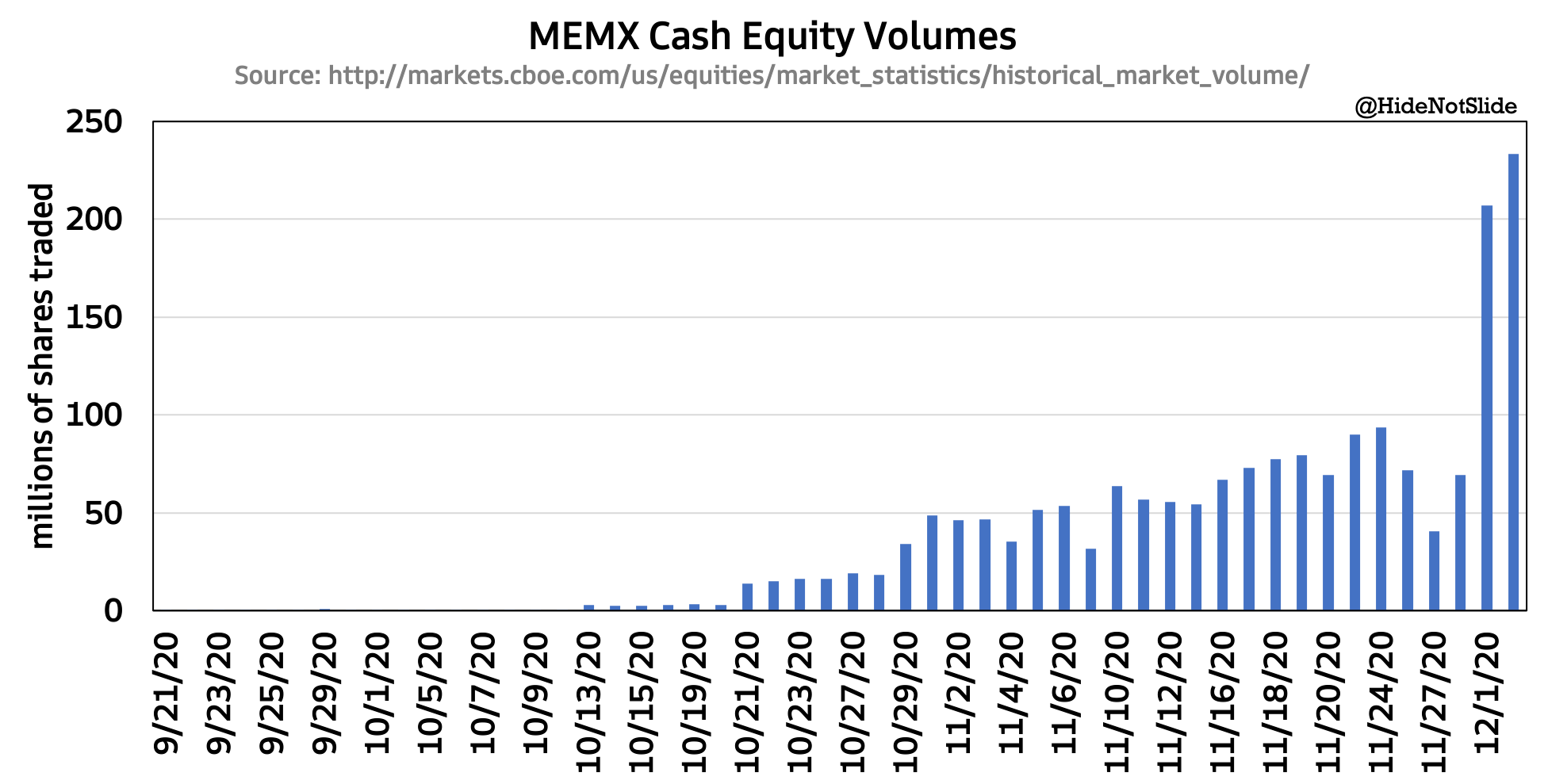

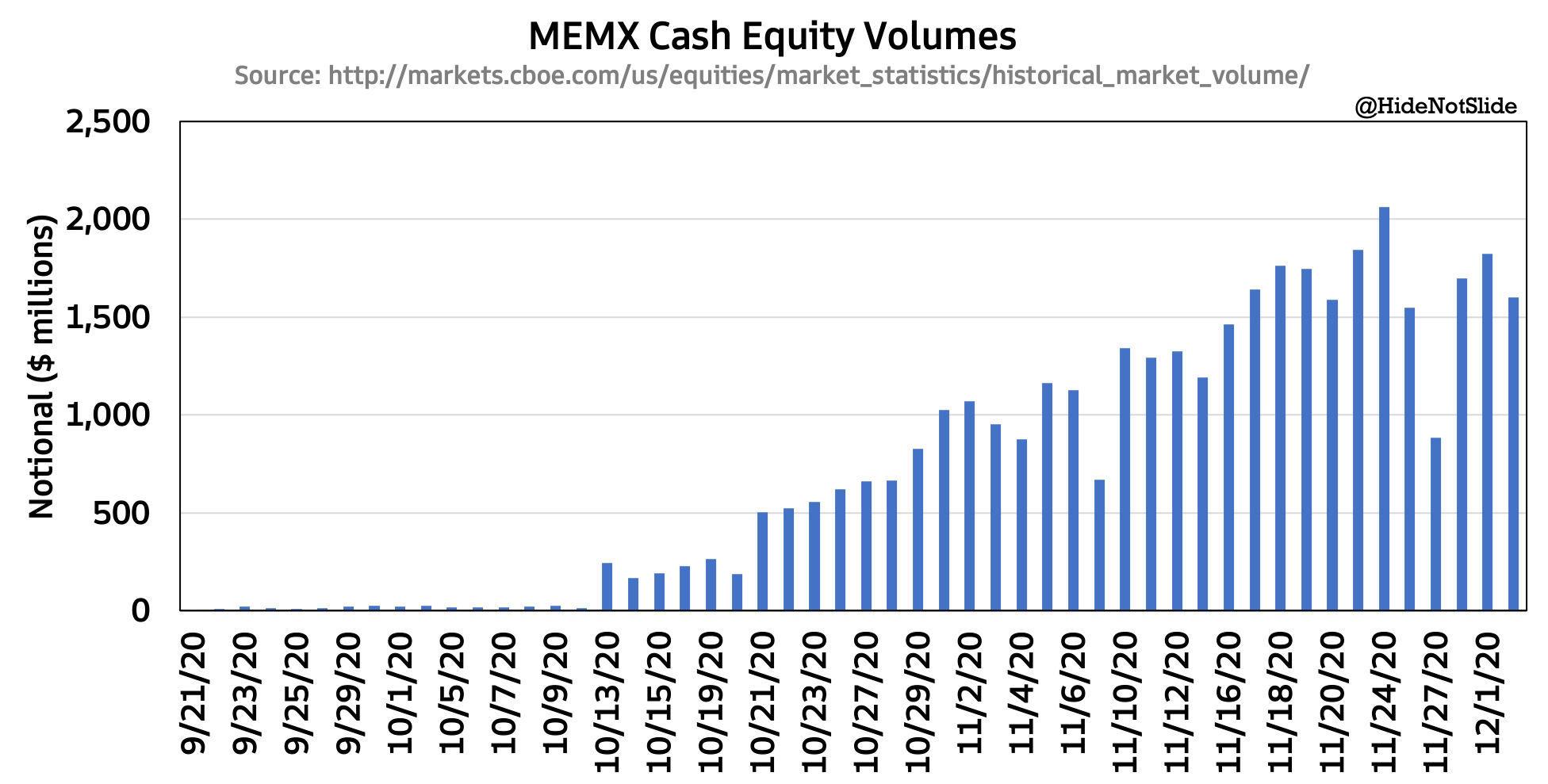

MEMX’s stunning rise on the equity market scene merits an update this week. The exchange launched on all symbols on October 29 - one month later, they already hold 2% market share and passed 200 million shares traded on their platform.

One potential driver of the surge in activity is changes to their rebate schemes to attract retail volume - a direct challenge to CBOE’s recent success with Retail Priority orders.

MEMX also seems to be attracting small dollar value stocks. While shares traded have exploded higher, notional value hasn’t risen as much:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, CBOE, NDAQ and VIRT. I am also long Bitcoin.