Nasdaq Q4 2020 Earnings Review

Nasdaq Q4 2020 Earnings Review

This piece is part of a series on exchange & market data industry earnings - please SUBSCRIBE below for more earnings reviews & weekly writeups on the top stories in exchanges:

Links

Results

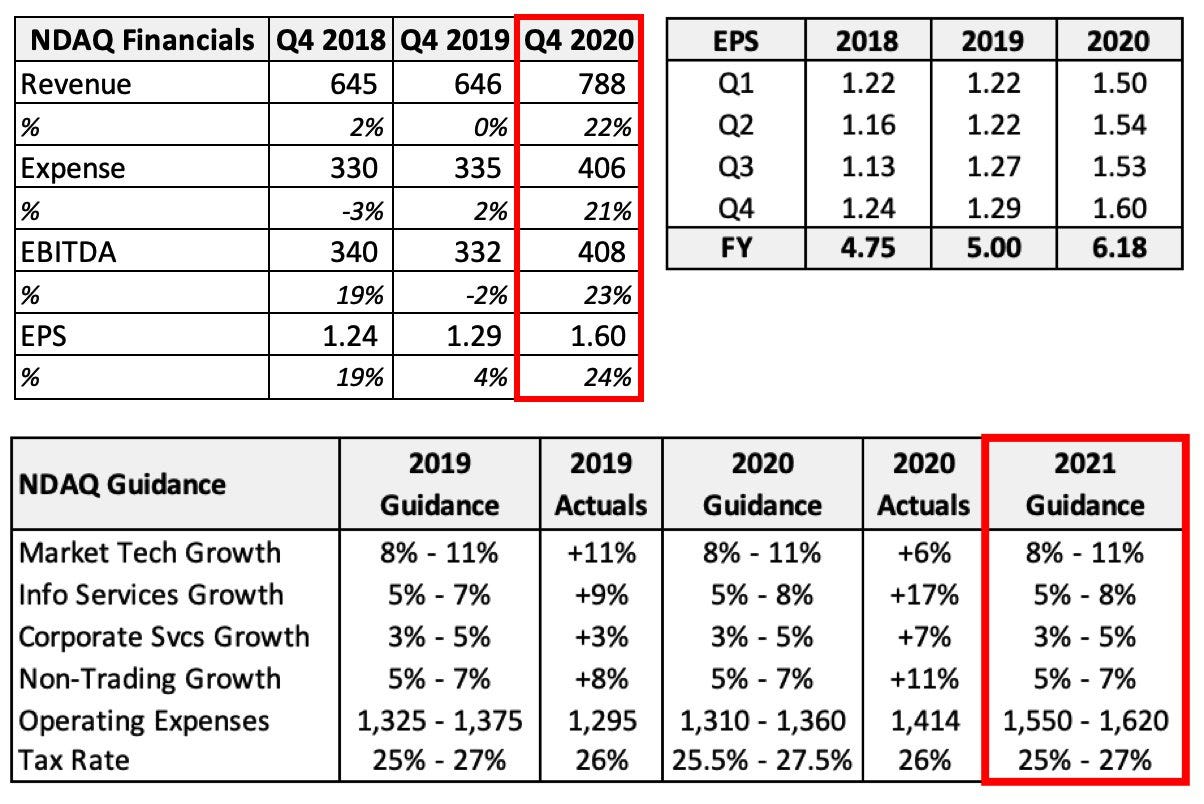

(Source: Nasdaq Investor Relations)

Nasdaq entered Q4 earnings season with the stock trading at all-time highs. The market applauded when Nasdaq doubled down on recurring SaaS revenue during their November 2020 investor day, and kept the applause rolling when they announced their acquisition of Verafin, an anti-finCrime technology company. A mix shift towards more stable, predictable revenue streams while still putting up solid growth numbers makes Nasdaq’s results easier to forecast & expands their valuation.

To top it all off, Nasdaq is the #1 options exchange in the US, and the options market is as active & chaotic as it’s ever been. Options volumes hit new all-time monthly records six separate times in 2020, and FY volumes were 75% higher than the average over the last decade. Steadily growing SaaS revenue combined with peak transaction performance creates a recipe for a stellar quarter.

With some exceptions, a stellar quarter is largely what we saw when Nasdaq reported results on January 27. Revenue grew +22% in Q4 2020 with equal contributions from Solutions (the recurring businesses) and Market Services to the result. Within the Solutions segment, Index revenues continue to explode higher - Q4 saw eye-popping +70% growth YoY as Nasdaq ETF assets reached a record $360 billion and index derivatives trading more than doubled to 90 million contracts during the quarter. The massive outperformance of the Nasdaq index itself has attracted materially higher interest in related funds, and Nasdaq the exchange is benefitting.

The rosy picture becomes a little muddied when turning to the Market Technology business, a closely-watched part of the company given Nasdaq’s large & unique position as an exchange technology provider. Market Tech revenue grew +4% organically in Q4, below its medium term guidance range of +8-11% every quarter in 2020. Management kept pointing to delayed projects & uncertainty around large client deals due to COVID. New order intake shrank to $37M in Q4, way under Q4 2019’s intake of $204M and the lowest number of 2020. It looks like Market Tech sales are slowing down because large clients aren’t locking in new contracts given the pandemic disruptions. This may turn around later this year as the economy reopens, but the outlook here is uncertain.

Additionally, Nasdaq reported a one-time $25M expense reserve for a particular Market Technology project that is proving more difficult than they originally expected. According to management the client has been with Nasdaq for many years and has a long-term contract with the exchange. Discussions with the client during Q4 2020 caused Nasdaq to increase their cost projections for the contract and take a hit to EPS. While the charge is one-time in nature, it does signal that Market Tech is a high-maintenance, relatively nascent business that does have cyclical characteristics. Could these kinds of charges happen in the future? I’m unsure - we certainly weren’t expecting this one. Market Tech margins were already below average, and this expense reserve means they’re now even lower:

Nasdaq’s Q4 earnings revealed a challenging Market Tech environment that stellar results elsewhere - mainly trading & index products - are overcoming. I’m currently long Nasdaq and will continue to hold after digesting earnings; I’m pleased with Nasdaq’s exposure to options trading & a blisteringly fast-growing index business, and the addition of Verafin later this year should add more opportunities to grow Nasdaq’s SaaS revenue. A healthy listings & corporate services business adds to my optimism. The stock may trade off its highs if options trading starts to slow down, but I think the forward multiple will keep inflating & the stock will keep outperforming the S&P.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this post, I am long ICE, CME, CBOE, NDAQ and VIRT. I am also long Bitcoin.