More Firms Want Robinhood's Order Flow

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

News

High-Speed Trading Firm Jump to Execute Retail Investors’ Stock Trades: “When the facts change, I change my mind. What do you do sir?” - John Maynard Keynes

The US equities wholesaling business is changing. Retail trading users & volume have exploded higher since COVID began. High single stock & market volatility is now the norm. Robinhood’s decision to offer free trading to clients has pushed the entire industry to match & has emphasized alternative sources of revenue - like selling order flow to high frequency traders. Virtu & Citadel Securities dominate the US wholesaling business today and have for a while now. They made a killing managing the changing retail landscape in 2020 - reports surfaced that CitSec alone made ~$7 billion in revenue, but we can’t know for sure. CitSec is a private company & can keep official figures close to the chest.

Virtu, on the other hand, plays with an open book. Being a public company requires transparency, not only about past results but about future strategy too. Virtu management is required to tell the world they made exactly $3,239,331,000 of revenue in 2020. Every quarter they’re also required to hold a public call where they say things like:

We made record amounts of profit in 2020! US equities wholesaling is a great business to be in! We’re paying our employees more & giving out plenty of dividends and buying back tons of stock!

To grow in the future we plan to enter adjacent businesses like options & crypto market making, which should become meaningful sources of revenue over the medium term.

In the world of high frequency trading it’s a significant disadvantage to play with an open book. Virtu’s competitors are very strict about not saying the very things Virtu is required by law to say. If rivals know how profitable a certain business is, they might decide to focus a bit more on that business and take profit away from the firm that’s keeping all of it for themselves.

First we saw Hudson River Trading announce plans to enter the wholesaling business in 2022. Now Jump wants to enter the fray. More firms may announce plans to follow suit in the coming months. This is honestly one of the biggest shifts in US equity market competition we’ve seen in quite some time. The Jump news is particularly important because it already acts as Robinhood’s top crypto wholesaler - adding a US equities arrangement to their already close relationship seems like a no-brainer.

Here are some of the important impacts that come to mind:

It ensures PFOF will likely stick around - The SEC’s job is to promote competition & prevent market manipulation. It recently launched an investigation into potentially unfair wholesaler concentration in US equities, the very space that’s now brimming with new entrants & fresh competition. The need for regulators to transform how wholesaling & PFOF works may be quickly fading away.

It improves Robinhood’s revenue capture - Simple economics states that, keeping other variables constant, higher demand for a product should equate to higher prices for that product. The “product” in this case is retail order flow, and more market maker demand for this flow should in theory lead to higher prices paid to trade against it. This could come in the form of price improvement - tighter spreads & better execution for retail - or in the form of higher PFOF rates paid to retail brokers. Robinhood’s primary revenue stream just became a lot more valuable.

It caps upside in Virtu’s stock - Using the same simple economic principles I referenced above, if competing for retail order flow does become harder with the entrance of HRT and Jump to the market, incumbent wholesaler margins are likely going to come down. Both firms aren’t expected to officially enter the market until 2022 and will need time to ramp up operations, but they are coming for Virtu & CitSec’s business nonetheless. I still think Virtu can do well if extreme volatility returns to the equity markets, but it won’t capture as much of the profit opportunity as it would have if this new competition wasn’t present. If the stock gets above $30 in the next 6-ish months the temptation to exit my long position may get the better of me this time.

LSE chief pledges to resolve ‘unacceptable’ Eikon outages: Marriage is hard. It takes a lot of work to make a happy marriage last, with plenty of difficult seasons expected to come. Marriage is even harder for public companies, because once every three months they have to hold a widely-followed conference call where they update the world on the state of their marriage & take questions from concerned critics about how it could be better.

Such is the case for the marriage of LSE & Refinitiv, who pulled the curtain back on the progress of their cumbersome, complex union on August 6. Revenues grew +5% YoY driven by a surge in index revenue & stellar credit trading volumes at Tradeweb. The London IPO market was strong in Q2 and management hinted the 2H 2021 pipeline looks robust, boosting Capital Markets revenue. Investors also cheered LSE’s dividend raise & better than expected synergy figures, sending the stock +6% after results were published.

There were some signs of marriage trouble however. Eikon, Refinitiv’s towering desktop business, continued to shrink. LSE’s incremental $1 billion in investment needed to refresh & update Refinitiv’s systems is sticking. Expense guidance didn’t change despite better than expected progress on synergies. As if that wasn’t enough, Eikon experienced another embarrassing outage on August 2 after similar glitches in April & June, raising more questions about Refinitiv’s ability to compete with Bloomberg & satisfy a shrinking customer base. LSE is making progress on their integration as planned, but the first years of its marriage to Refinitiv are proving to be as difficult as investors feared when LSE’s stock dropped -20% earlier this year.

Robinhood Buys Say Technologies for $140 Million: Believe it or not, most individual stocks come with some form of voting rights. Every year around the annual shareholders meeting your broker will send you voting materials where you can cast your ballot for a company’s Board members and other shareholder matters of note. For the vast majority of individuals, voting is pointless. The top 10 shareholders in a company normally control the lion’s share of voting power and are therefore the ones who decide members of the Board & management. This includes the behemoth ETF managers BlackRock & Vanguard, who together are the top shareholders of nearly every company in the S&P 500. When retail investors buy an ETF they give up voting power to these asset managers, who spend significant resources to coordinate voting power & put pressure on portfolio companies to act in-line with their agenda.

Now compare this with Say, Robinhood’s latest acquisition focused on modernizing shareholder voting & communication technology. Say Technologies partners with public companies to hold investor polls, live earnings Q&A with community up/down-vote based questions, and shareholder proxy voting via one platform. Robinhood plans to integrate Say with its larger brokerage ecosystem and give millions of retail investors an easier way to engage with the companies they own.

I think this will have a couple interesting impacts:

It will give Robinhood another feather in its UI/addictive app design cap as a leg up on competitors. If AMCApe69420 wants to make their voice heard to company management, I believe they’ll choose to do so through a clean, easy interface rather than deal with other brokers who manage shareholder votes through un-friendly online forms or even by mail. Say Tech makes Robinhood’s retail moat that much bigger.

When combined with social media I think the Say-Robinhood integration will make proxy season way more entertaining. Early 2021 saw retail shareholder activism in stocks like GameStop & AMC through the herding of trades - if enough people buy enough OTM call options all at once, they can control the price action in a stock. With Say, Reddit retail bros now have a way to herd votes in the same way they herd trades. The retail bros may not care who’s on the Board of Directors of AMC or GameStop. They may not be interested in quarterly management commentary. I’m willing to bet that with Say & Robinhood together under one roof, they might just start to care a little bit more.

My latest paid post is live - The Great Big Q2 Exchange Earnings Review is a comprehensive analysis of each exchange & market data stock’s quarterly results as well as my thoughts on which ones impressed & which ones I’m avoiding. This 4,000 word report on the 10 biggest companies in the industry is in my opinion the best value for subscribers who need quality research but can’t afford sell-side reports. Subscribers get immediate access to this post and a long list of past research on the industry.

Thank you for your support!

Other Stories I’m Reading

The Era of Cheap Natural Gas Ends as Prices Surge by 1,000%

Howard Lutnick Takes Aim at CME’s Dominant U.S. Rates Market

Nasdaq’s Board-Diversity Proposal Wins SEC Approval

Micro WTI Crude Oil Futures Surpass 1 Million Contracts Traded

SEC hits crypto exchange Poloniex with $10 million fine

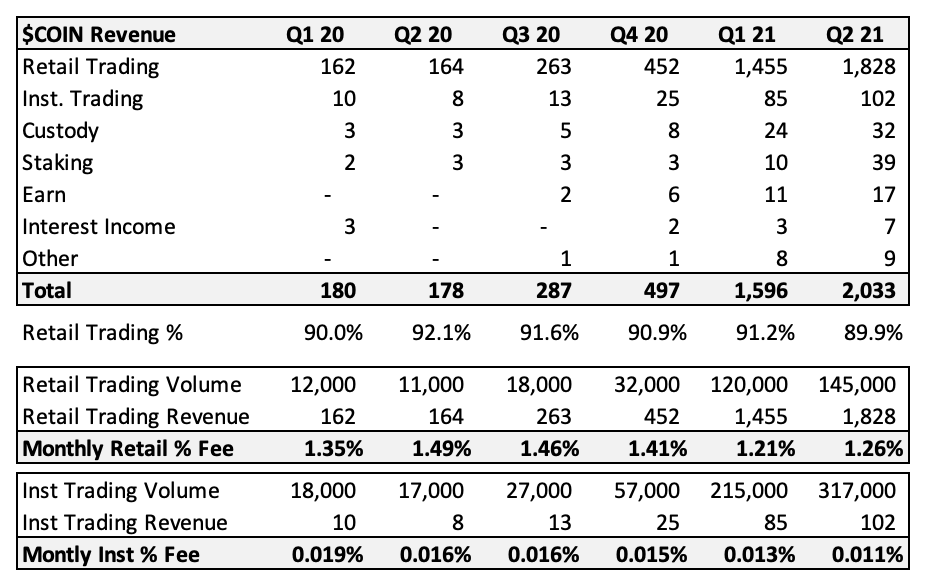

Chart of the Week

The first quarter of 2021 was a great time for Coinbase. Crypto prices were soaring, industry interest was hitting new levels of feverishness, and volumes were reflecting this sentiment with massive amounts of activity particularly in January & February. Coinbase ended Q1 with 6.1 million active users, up 4x from Q1 2020.

The second quarter of 2021 was an INCREDIBLE time for Coinbase. Trading volume hit new all time records in May as mix shifted away from Bitcoin trading to Ethereum and alt-coins, which now make up ~75% of all trades on the platform. Although institutional fee capture continues to slide, retail fee capture, accounting for 90% of revenue, actually rose sequentially. Coinbase ended Q2 with 8.8 million active users, up an impressive +45% QoQ. Investors cheered Coinbase’s stellar results by bidding the stock up to three month highs at just above $275 per share.

The focus now turns to the future. I’ve said this before & I’ll say it again - 90%+ of Coinbase’s revenue comes from volume-based transaction fees, and no one can predict volumes. Coinbase management “guided” for trading fees to be down in Q3 based on today’s trend tampering the stock’s gain a bit, but their guess is as good as mine. I continue to hold my $COIN shares on the bet that crypto volatility is not done this year, giving the exchange insane amounts of cash flow to either return to shareholders or make investments in diversifying revenue streams.

(Source)

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, COIN and VIRT. I am also long Bitcoin, Ethereum, and UNI.