The LSE-Refinitiv Honeymoon Is Over

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

2021 has not been a pleasant year for the London Stock Exchange.

LSE’s stock plummeted after reporting FY 2020 earnings on March 5, with shares now severely underperforming market indices and -20% YTD.

The culprit? Refinitiv. A 16 month honeymoon between the two firms has already faded so soon after their tie-up became official. Investors are coming to terms with the fact that an exchange marriage of this size is tough to pull off and will require more investment than many are willing to wait for.

What caused such a strong shift in perception to warrant this kind of sell-off? How did we get here? What happens now?

The Engagement

In April 2018, LSE announced that David Schwimmer, a 20 year Goldman Sachs veteran & partner, would take over as its new CEO. Schwimmer began his reign at LSE during a tumultuous time for European exchanges - the potential for a hard Brexit loomed large & low volatility had muzzled equity & interest rate trading volumes. Schwimmer chose to combine his deal-making experience with a bet on recurring, subscription market data growth & made a play for Refinitiv, a massive data business nearly twice the size of LSE by revenue. The $27 billion merger of the two firms was announced in August 2019. The happy engagement had begun.

What did LSE see in Refinitiv? Quite a bit of potential. Refinitiv’s business can be organized into four parts:

Eikon: A desktop terminal allowing users to access real-time & historical data for a wide array of financial products, along with connections to Refinitiv’s other markets & data feeds. Eikon currently serves ~190,000 customers who pay between $3,600 - $22,000 per year for various levels of data access.

Risk & Post Trade Solutions: A suite of services tailored towards banks & financial institutions to help them manage compliance obligations, including KYC & financial crime prevention tools.

FX Trading: Currency platforms FXAll and Matching control ~35% of the global FX market, with $400 billion notional traded per day between the two. Most of the top banks, hedge funds & FX traders use FXAll & Matching to access the deepest currency markets in the world, supported by direct integration with the Eikon terminal.

Tradeweb: Refinitiv owns a controlling interest in Tradeweb, the top electronic platform for US Treasuries & a fierce competitor in corporate bonds with MarketAxess. Tradeweb’s IPO and stellar +100% return over the last two years has made it a considerable part of Refinitiv’s overall value as an acquisition target.

LSE’s sales pitch to investors was simple: a combination with Refinitiv would diversify the exchange towards more predictable revenue growth, improve the value of its existing products, and provide significant synergies.

This pitch made sense on first glance. A combined LSE & Refinitiv would boast nearly 70% recurring revenue, which normally comes with more predicable earnings growth & higher valuations. LCH, LSE’s dominant clearinghouse for swaps & interest rate products, would benefit from closer ties to FXAll and Tradeweb. LSE’s FTSE Russell index products could be distributed more widely through the Eikon terminal and improve sales. These & other strategies supported management’s target of 5-7% annual revenue growth & £575M in total synergies:

(Source)

The Honeymoon

Investors initially cheered the transaction, calling it “transformative”, “a win for London“, and a “defining moment” for the industry. After years of failed merger attempts with Deutsche Börse, Nasdaq, and even TMX Group, LSE had finally pulled off a game-changing acquisition. They had finally “bagged the elephant”.

Only one question remained before the party could start - would regulators approve the deal? How could two massive market infrastructure groups combine without affecting competition? Would concessions need to be made to receive the green light?

After a prolonged probe & negotiations between LSE and regulators, EU authorities approved the deal on two conditions:

LSE would sell Borsa Italiana to a competitor.

LSE would not combine LCH’s interest rate clearinghouse with Refinitiv’s rates trading businesses.

Shortly after the ruling came out, LSE agreed to sell Borsa Italiana to Euronext for €4.3 billion and to keep rates trading & clearing separated. On January 13, 2021, regulators officially signed off on the acquisition, which closed soon after. The exchange mega-deal was finally complete, and investors who stayed along for the ride were rewarded in spades. During the 16 months from announcement to close, LSE’s stock jumped +70%, easily outpacing global averages and making it one of the largest & best-performing stocks in Great Britain. The market was elevating its valuation for LSE + Refinitiv given the EU approvals and optimistic integration targets, and in the meantime, COVID volatility had injected life into LSE’s transaction business. Sentiment couldn’t have been better as the two market giants officially became one.

The honeymoon phase, however, was about to end.

Marriage Problems

On March 5, 2021, LSE reported Q4 and FY 2020 earnings. It was the first public meeting with investors since the Refinitiv deal had closed, and it included updated 2021 guidance for the combined firm. This guidance contained several startling updates:

LSE would need to spend an additional $1 billion in 2021 (two years of free cash flow) to fund upgrades & integration efforts with Refinitiv.

Total operating expenses would grow mid single digits in 2021, including synergies.

In year one, revenue would come in under the 5-7% target management laid out when the deal was first announced.

Yikes. LSE won backing for the deal on the promise of better margins as revenue growth & expense savings would make up for Refinitiv’s high price tag. With this updated guidance, the exchange is now saying 2021 will be a year of sowing rather than reaping.

Each of these points likely has to do with Eikon, Refinitiv’s flagship terminal rebranded as “Workspace” which makes up ~40% of revenue. The terminal business is facing a number of challenges in light of growing automation, no-touch trading and passive investing. If an algorithm is handling most of the trade execution for a firm & retail investors simply follow a benchmark, who needs expensive terminals?

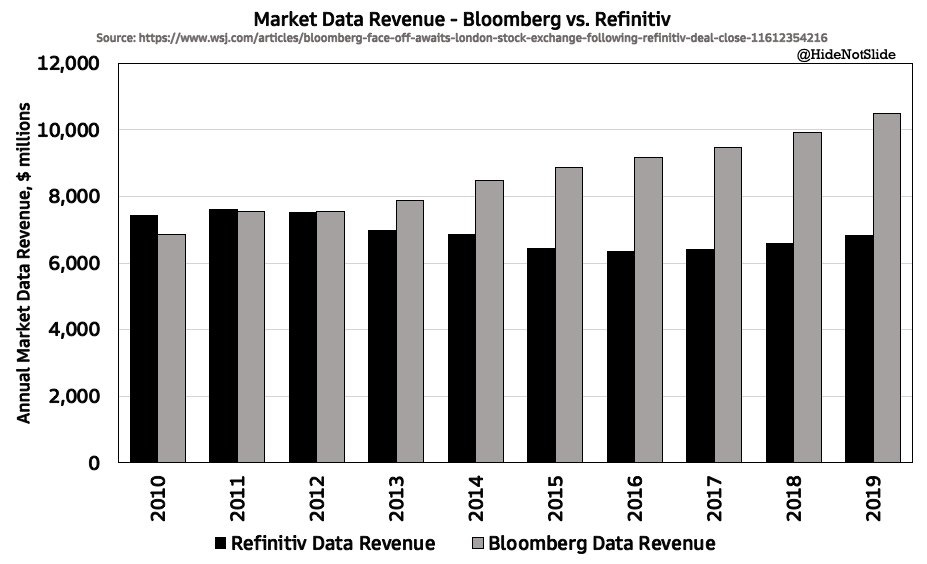

There’s also Bloomberg, Refinitiv’s #1 rival, to consider. Bloomberg has taken significant market share from Refinitiv in the last decade despite higher prices as customers pay up for a premium product. Others have described the elitist social network effect Bloomberg has spent years forming & nurturing, making it nearly impossible to disrupt. In 2010, Refinitiv was the top global terminal business with nearly one-third of the global market. Today they have just above 20% of a market Bloomberg now dominates:

(Source)

To even attempt to overcome Bloomberg’s competitive advantage & regain market share, Refinitiv needs to make major upgrades to its product offering, and that takes money. About $1 billion in 2021 to be exact.

LSE’s lackluster revenue guide may also be a product of its concessions to regulators. If LCH can’t integrate with Refinitiv’s trading platforms to appease EU antitrust authorities, where will revenue synergies come from? How will LSE be able to extract the value it needs from Refinitiv’s transaction businesses if it has to keep them running solo?

LSE’s news of higher costs and lower expected revenues immediately spooked investors, causing a sharp drop in the stock. Some are beginning to doubt the deal’s rationale altogether. Pulling off mergers of Refinitiv’s magnitude is incredibly hard - it takes a smart, dedicated management team to truly add value in the years following a mega deal like this. Will David Schwimmer, a proven deal maker but an un-proven operator, be able to pull this integration off? This remains to be seen. I personally am not eager to buy shares of LSEG even after the recent drop in price. I’m not convinced Refinitiv will be able to catch up to Bloomberg, and synergies (particularly on the revenue side) will be hard to find.

Honorable Mentions

Robinhood confidentially filed for an IPO on March 24, setting it up to go public sometime in Q3 2021. This comes as GameStop chaos & retail trading in general has begun to cool off in recent weeks, and regulators remain frustrated with the company’s payment for order flow disclosures & handling of the GameStop trading debacle.

IHS Markit reported fiscal Q1 2021 earnings on March 24, beating analyst expectations & raising its full-year outlook to the upper end of its guidance range. Strong Q1 results were driven by its Financial Services unit, which grew +10% YoY as demand for risk analytics & post-trade solutions remained elevated.

CBOE announced its acquisition of Chi-X Asia Pacific, an equity platform with 18% market share in Australian equities & 3% share in Japanese equities. CBOE intends to expand its block trading business acquired with BIDS in Asia & bolster its market data sources. David Howson, head of CBOE Europe and in charge of the company’s EU derivatives launch, will serve as head of APAC as well. Chi-X APAC made ~$26M in revenue during 2020.

Investor & writer AGB published a good piece on ICE recently, walking through the company’s history of acquisitions & returns on capital. You can find this writeup here.

Chart of the Week

Bloomberg put out a great chart this week highlighting just how wonderful it is to be an exchange. The below plots the Fed funds rate from 2008 - 2022 in black vs. what futures markets were predicting in gray over the same period. In nearly all cases, traders were predicting rates would rise faster than they actually did, and hedged their bets accordingly.

Someone who in 2008 hedged against the risk of rates rising to 4% by 2011 was wrong - like really wrong - but the exchange got paid all the same. The old adage “during a gold rush, the ones making money are those selling the pickaxes” comes to mind here. Most of the time, traders are hedging against risks that will not happen, but they pay exchange fees month after month to remove them nonetheless.

Not knowing the future comes with unavoidable costs - better to be in the business of facilitating bets than making them:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Bitcoin & Ethereum.