Miami's Wall Street Challenger

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

Welcome to Miami

Last week I profiled the stunning rise of the US options market in 2020. This week I want to profile the equally stunning rise of one of its most promising underdogs - Miami International Holdings, or MIAX. The success of MIAX since its launch in 2012 serves as a textbook example of industry disruption, and the company’s unique vision gives them a chance to win a permanent seat at the table.

The idea for MIAX was born at a New Jersey law firm in the mid 2000s. Thomas Gallagher, a New Jersey native with an Ohio law degree, started his own practice in the early 90s catering to the financial services industry. Gallagher was able to learn about exchanges first hand from dealings with clients who traded and made markets in options. Some of his clients thought competition was missing from the options market, and Gallagher saw an opportunity to build his own exchange and fill the gap.

Gallagher had the legal expertise to win SEC approval for an exchange. He had a deep Rolodex of potential investors to raise capital. His offices were close to New York, where he could tap into a deep pool of Wall Street talent to get a market off the ground. By 2007, he had raised over $100 million from partners in Kuwait & around the world to begin the launch process.

Next came the human capital. With a healthy war chest in tow, Gallagher attracted current and former executives from Nasdaq & CBOE to branch out and join his upstart venture. Industry knowledge from top competitors helped MIAX build a state of the art platform from the beginning. MIAX received SEC approval for an options exchange in late 2012, and officially launched on December 7.

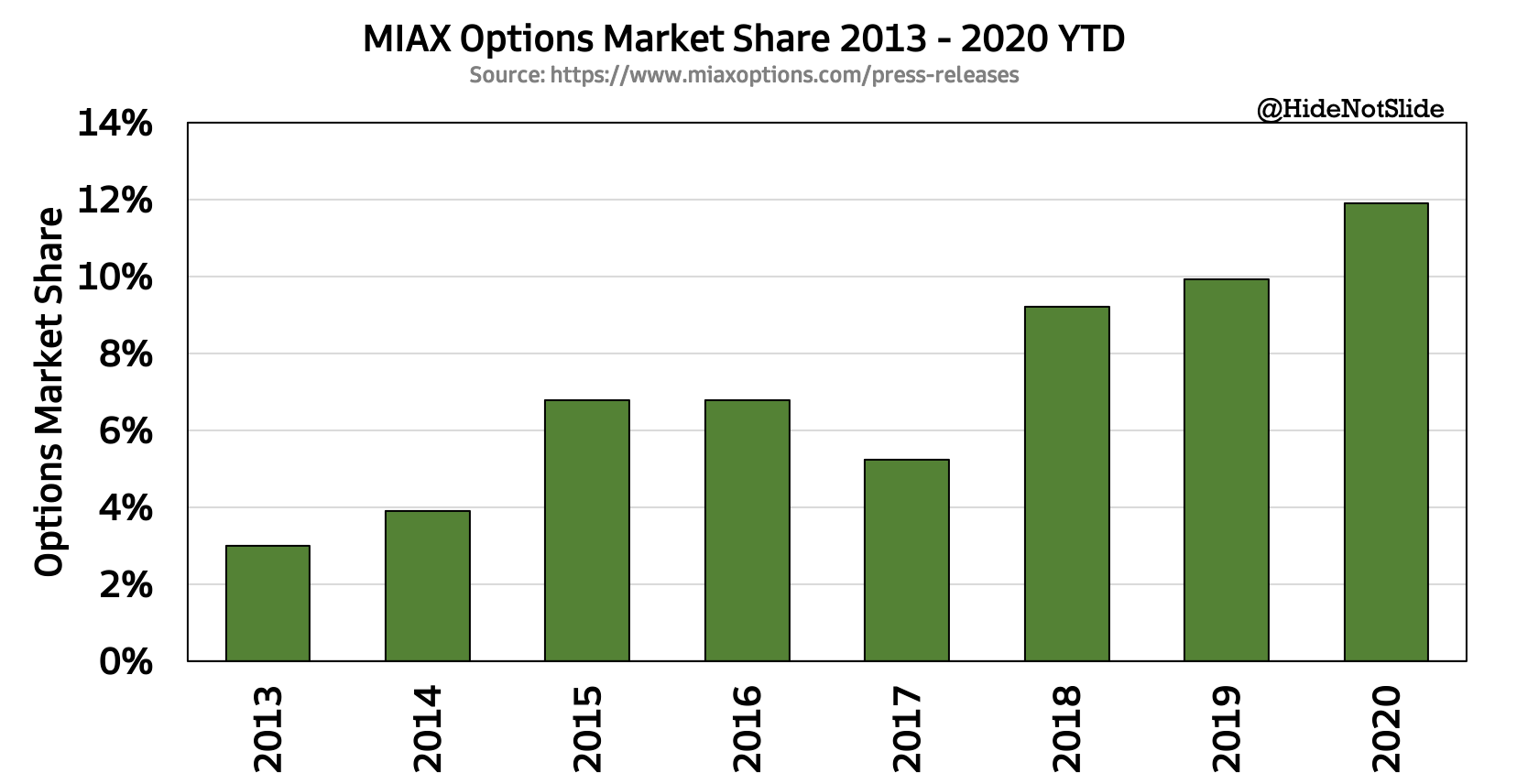

After finally securing a seat at the table, MIAX could start competing with legacy options exchanges for business, using an age-old industry tactic to win market share. Starting in 2013, MIAX created an incentive for banks & other large customers to send volumes their way - ownership in the exchange itself. In exchange for pre-payment of trading fees and helping MIAX hit certain market share milestones, participating members would get equity in MIAX at the end of the contract. The tactic worked - by the end of 2013 the startup had captured 3% of the options market, a notable foothold. MIAX launched a second equity offering for customers to move volume to their exchange in early 2015, and more well-known trading firms took part in the program. By the end of 2015, market share rose to 7%. Today MIAX holds just under 12% of the options market, with jumps in market share corresponding to new equity deals with their largest customers.

At 12% market share I estimate MIAX’s revenue to be anywhere from $50 - $75 million per year based on public competitor data. With a growing high margin revenue stream secured from their successful options business, MIAX began setting their sights on expansion into new asset classes & geographies.

MIAX’s first foray outside of options didn’t come without controversy. In 2016 MIAX bought a stake in LedgerX, a crypto startup with backing from Google Ventures and other established VC firms. In the years that followed LedgerX struggled to get a successful crypto futures product off the ground, butting heads with the CFTC over delayed product approvals and failing to gain traction despite being one of the first regulated crypto exchanges to market. In late 2019 LedgerX co-founders Paul and Juthica Chou were ousted from the company, the same day rival Bakkt launched Bitcoin options. A few weeks later a LedgerX board member sent a letter to the CFTC alleging the company was in chaos and in violation of CFTC compliance, while MIAX was leveraging its two board seats to launch a hostile takeover bid. While no such takeover materialized, MIAX did lead a new $4 million funding round for LedgerX that closed around the time the letter was sent.

MIAX has also eyed growth in Latin America - not only with a presence in Miami, but with a controlling stake in the Bermuda Stock Exchange. Here’s Gallagher himself on MIAX’s global vision:

“Eventually we want to be the place where the global Hispanic entrepreneur seeks to go public… You do not have to be an entrepreneur from Colombia to list on our exchange. You can be a Hispanic entrepreneur from Union City. You can be a Hispanic entrepreneur from Hightstown. Or you can be a Hispanic entrepreneur from Los Angeles.”

(Source)

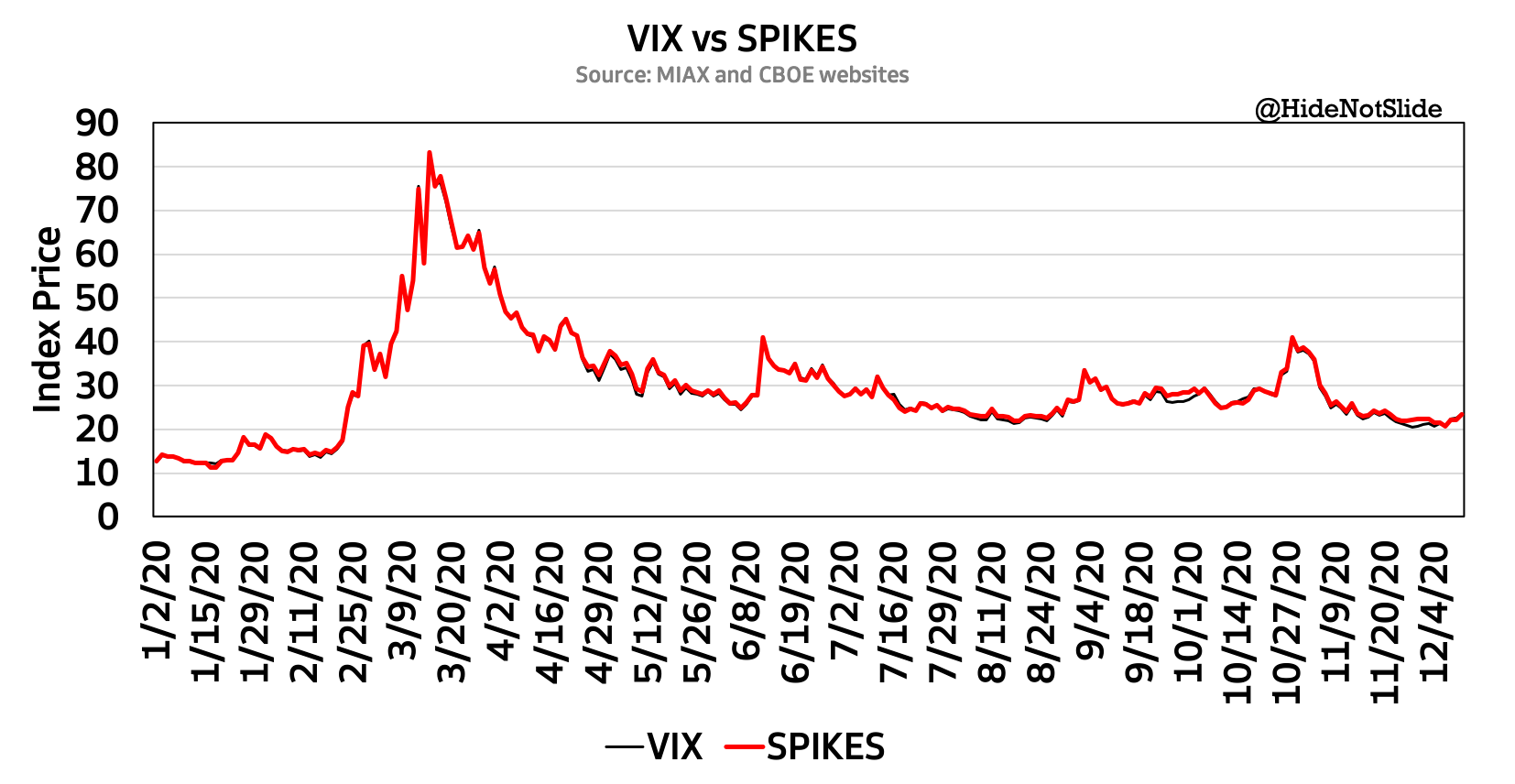

There’s also MIAX’s entrance into volatility futures to consider. In late 2019, MIAX partnered with T3 to launch a futures contract on the SPIKES volatility index, and in 2020 purchased the Minneapolis Grain Exchange as a venue to list the new contract. Whereas the classic VIX uses S&P 500 options to calculate volatility, SPIKES uses the S&P 500 ETF (SPY) to construct a look-alike fear gauge. The contract was voluntarily delisted after only a week of trading, but re-launched on December 14, 2020.

You can see how wide a net MIAX is casting with its investment capital. They’ve purchased stakes in MidChains, a Middle Eastern crypto exchange; in Diamond Standard, a spot diamond exchange; and in StratiFi, a risk management tool for financial advisors. They even launched a new cash equities exchange in late September 2020 with modest success to date.

I think the “throw money out there and see what sticks” approach is a good one provided management can execute and not stretch the company too thin. When it comes to cash equities and options, MIAX’s strategy of giving ownership stakes to top customers is one that has worked in the past and I believe will continue to show returns. Outside of their core options business, I’m skeptical. The SPIKES volatility index, for example, trades too much like CBOE’s VIX product for customers to switch to MIAX naturally. Why trade an illiquid volatility product that matches the exceedingly liquid one tick-for-tick?

I believe MIAX is placing a variety of bets to ensure long term relevance. If even one bet pays off - be it crypto, Latin America, equities, or even diamonds - MIAX will hold a low-cost key to future influence over a growing market. Whatever exit opportunity MIAX management may be considering - an IPO or strategic sale down the road - demonstrating lasting value creation is key to attracting capital. Exchange competitors and investors alike need to keep a watchful eye on MIAX and their growing presence in the US and around the globe.

NMS 2.0

On December 9, 2020 the SEC finalized the biggest set of updates to its market data policies since the 1970s.

The first big change includes adjusting the definition of a “round lot” to allow smaller trade sizes to be included in public data feeds. In the past, only data associated with trades in 100-share multiples were included in the public feed (the SIP), prejudicing larger dollar value stocks where round lot trades are less common. The new SEC plan introduces a tiered definition of round lots based on share price; the higher a stock’s price, the less shares needed per trade to be included in the SIP.

The SEC’s second change forces exchanges to include basic depth-of-order book data in the SIP. Traders would previously have to pay exorbitant sums of money to see this underlying supply & demand data for a stock, allowing them to time trades better & predict short term price movements. This change boosts the amount of quality market data flowing to more cost-conscious customers, although with more data comes the operational challenges of processing it - some estimate the SEC changes could increase the amount of SIP data by 10 fold.

The final change worth noting is the introduction of “competing consolidators” to the market. Today the legacy exchanges have a monopoly on supplying SIP data to the public, and give higher quality data & faster speeds through separate channels to those willing to pay huge fees. Under the new rules exchanges will be forced to give SIP data to registered competitors at a price the SEC sets, who can then turn around and sell that data to the public. These changes should foster more competition between the exchanges & those who can potentially provide a better data product at lower cost. The rewards for competing consolidators could be quite attractive - SIP fees amount to ~$250 million per year in total, and when split among the participating exchanges makes up a sizable portion of their market data revenue.

Overall I believe the changes are a step in the right direction. It’s a gargantuan task to update a system as complex as today’s equity market, and the SEC’s changes show they’re listening to the industry & are working to improve how the market functions. Even with these changes there’s no denying the system is still extremely complex - the SEC’s final rule release is a whopping 898 pages long, and the industry is still working to digest the full scope of changes & impacts.

Honorable Mentions

CME announced the addition of hemp pricing data to their platform in partnership with cannabis index firm New Leaf Data Services.

Multiple crypto index data deals were announced this week, including CBOE’s licensing deal with CoinRoutes and S&P Global’s deal with Lukka. Both announcements set each firm up to launch digital asset indices in 2021 with the potential to launch either futures or ETFs on top of those indices, should regulators give the green light. The CBOE deal stands out to me in particular given the exchange’s 2017 foray into crypto that ultimately ended in failure.

On December 16, CME announced the launch of Ether futures in February 2021 after successful launches of Bitcoin futures and options.

State Street - ranked 3rd in a 3-player global ETF race - is exploring strategic options for its asset management unit, including potential mergers with UBS or Invesco.

Massachusetts regulators filed a complaint against Robinhood alleging failure to protect customers from trading risks & “falling far short of the fiduciary standard”. A couple days later, Robinhood announced a $65 million charge to settle an SEC lawsuit alleging the popular broker failed to provide best execution to their users & hid the true nature of their operations.

Johannes Petry, Jan Fichtner & Eelke Heemskerk penned an insightful piece on the power & politics of index providers like MSCI, S&P Global and FTSE Russell.

High frequency traders turn to high tech hollow-core fiber optic cables to gain an edge over competitors.

Chart(s) of the Week

The listings business is a two-firm race in the US - Nasdaq vs. the NYSE. Each exchange has carved out a niche for itself to attract new listings; Nasdaq is the tech-heavy exchange catering to smaller IPOs with lower listing standards, and the NYSE is the pricey thoroughbred with higher fees but deep relationships with some of the oldest and most popular public brands.

The below charts show each exchange’s metric of choice - Nasdaq routinely celebrates the quantity of IPOs on its exchange (it did so this week), while the NYSE cites it normally has the most proceeds raised. The IPO market is quite cyclical, with lulls in activity when markets are volatile & surges when sentiment is strong.

2020 has been a record year for IPOs, with SPAC listings through the roof and high-profile names like DoorDash and Airbnb helping proceeds. The NYSE cited 2020 as the best year for proceeds raised in its history:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, CBOE, NDAQ and VIRT. I am also long Bitcoin.