FTX: A Defining Dilemma

Anyone who’s paid even the slightest bit of attention to markets in 2022 knows that the crypto tide has come out in vicious fashion.

Spurred by rising rates, inflation pressures & a retraction in global asset prices, a deep downturn has hit the crypto market with no digital coin or monkey picture spared from carnage. Altcoins like Solana & Avalanche have suffered a whopping -80% drop YTD. Ethereum is -70%. Even boring ole Bitcoin, the digital gold poster child, has retraced nearly -60% since the beginning of the year.

As the crypto tide recedes we’re beginning to see just how many trading firms, exchanges & high profile leaders in the space were swimming hopelessly naked. Even for a market as Wild-Westy as crypto, the amount of blowups among well-known, respected brands has been quite surprising. In the last few weeks alone we’ve seen firms like Celsius, CoinFLEX, Three Arrows Capital and Voyager Digital all either restructure their debt, restrict customer withdrawals, or enter outright bankruptcy as margin calls reverberate through the system. Headlines about new firms facing liquidity issues or cutting staff en masse continue to appear by the day. Crypto’s pain, at least for now, looks nowhere near finished.

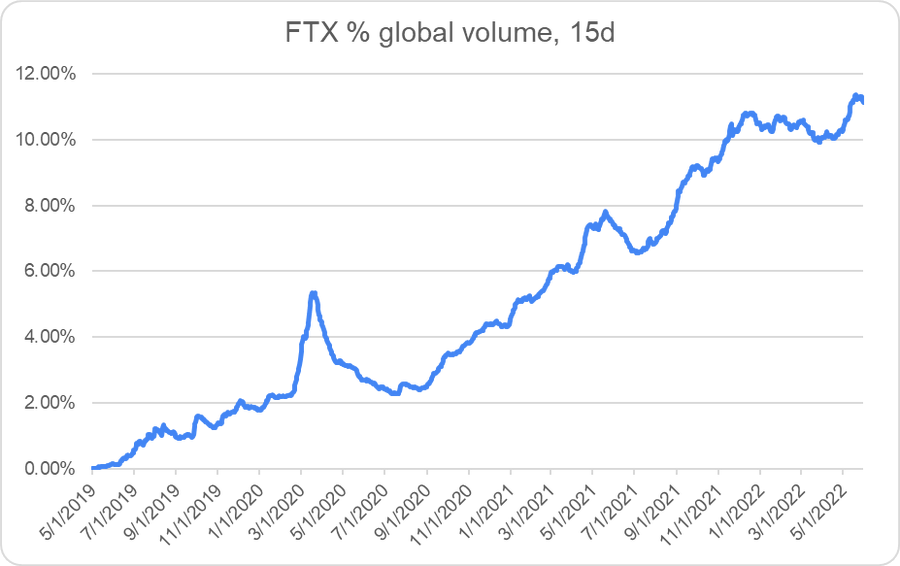

And yet, despite the industry-wide crisis dragging every major crypto firm to the brink of oblivion, one company has stood above the fray in dramatic fashion. FTX, the omnipresent, multi-billion dollar Bahama Behemoth, led by all-star altruist Sam Bankman-Fried, finds itself in a better position than perhaps any other crypto firm. FTX has leveraged a combination of shrewd marketing, aggressive lobbying and steady product rollouts to win substantial crypto market share, surpassing 10% of all global trading volume earlier this year:

(Source)

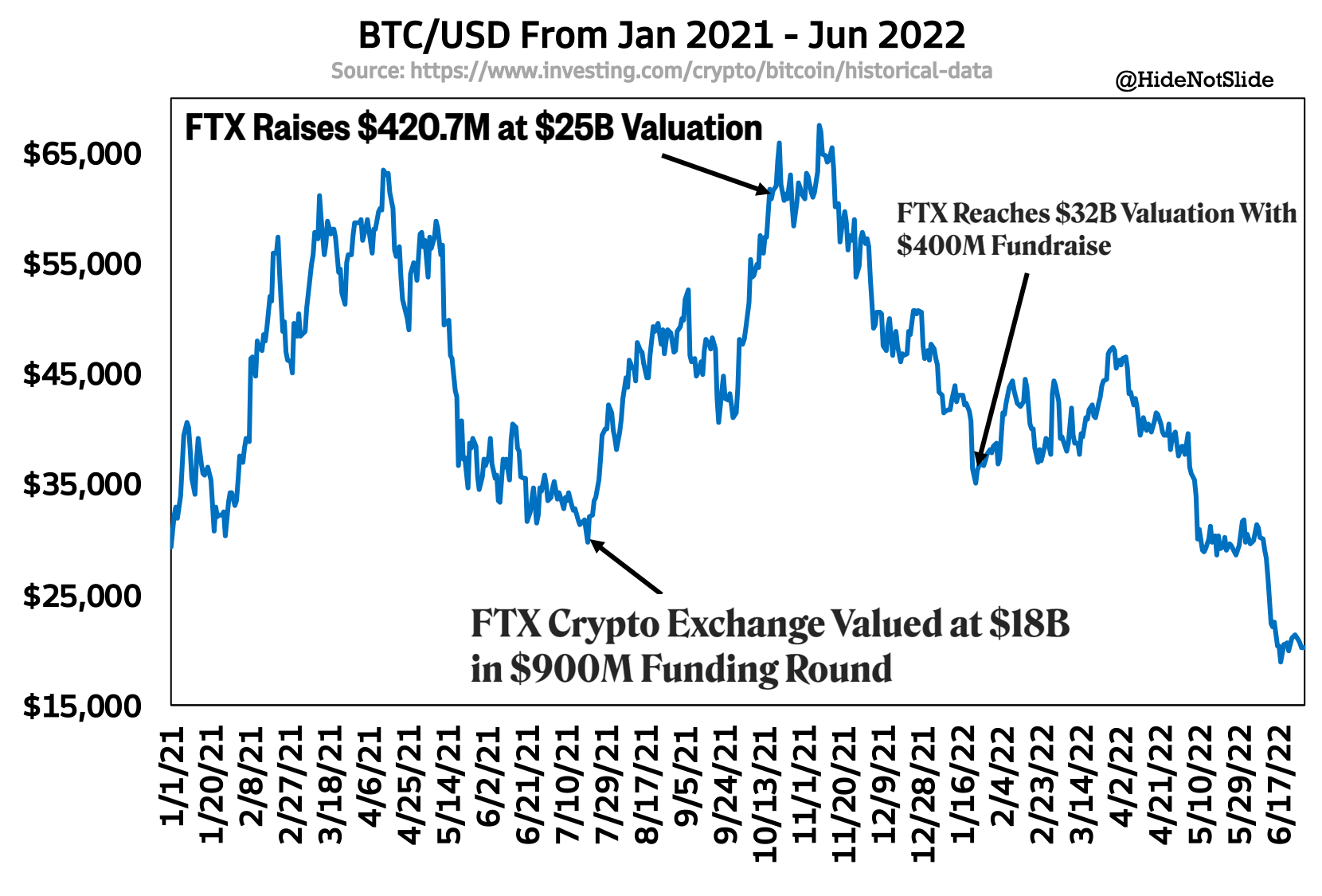

What’s more, during peak hype season in 2021, FTX embarked on a massive fundraising campaign that ended with nearly $2 billion in the bank and a $32 billion exchange valuation to boot. FTX’s second capital raise in October 2021 - priced at the $420.69 million magic meme number - came at almost the exact top for Bitcoin:

While retail traders & institutions alike were taking on leverage & plowing head first into long-only rocket-to-the-moon crypto plays, FTX took advantage of the hype to strengthen its balance sheet beyond what most crypto firms could match.

Did SBF foresee the coming crypto winter? Could his team have predicted that rising rates would cause cascading liquidity crunches across their industry? Were FTX’s numerous fundraises the exchange’s way to “sell the top”? We may never know. Regardless, in retrospect, raising that much cash in 2021 looks like yet another genius move by SBF that secures his exchange’s future for many years to come.

The Dilemma Part 1 - Crypto

Very rarely are companies able to time the market like FTX seems to have done. Flush with cash and faced with a new bear market across crypto & traditional markets alike, FTX can now make strategic investments at attractive prices to solidify its position as the world’s top crypto firm. SBF was recently quoted saying the exchange plans to spend $2-$3 billion on M&A and other investments in the coming quarters.

Opportunities of this size come with challenges, however, and leave FTX to assess new questions in its life as an exchange. What the heck do we do with all this money? We have so many opportunities to capitalize on this deep crypto bear market - how do we make the most of it? I believe FTX’s answer to this question will define its future as an exchange over the next 3-5 years and potentially for much longer.

While the question hasn’t been fully answered yet, we have been given clues as to where FTX may be looking to invest & the dilemma that sits in front of them.

One one side of the equation, FTX remains committed to its long term goals of expanding influence across global crypto markets, acquiring new (mostly retail) customer groups, and building new crypto trading products. In February FTX announced its purchase of Liquid Group, an Asian crypto exchange with operations in Japan, Singapore & Vietnam and ~$60 billion in annual trading volume. A few months later it purchased Bitvo, one of Canada’s largest crypto trading platforms, and a license from Cypriot regulators to expand product offerings in Europe.

This string of deals grows FTX’s geographic footprint and gives the exchange more seats at the global regulatory table, where SBF and his team can push for more retail & institutional access to the crypto ecosystem. As it relates to their core vision I view these purchases as relatively low risk & prudent ones to make.

We’re also starting to see FTX use its cash pile in a distressed investor/”lender of last resort” role with a number of crypto firms facing liquidity issues. The most prominent example of this came when BlockFi, a large crypto lender with ~$15 billion in AUM as of 2021, found itself short on cash after large customers (Three Arrows Capital in particular) failed to meet their debt obligations. Amid growing doubts about the lender's future, FTX announced a $250M revolving credit line had been extended to the company & later unveiled it had purchased an option to outright buy BlockFi for up to $240M. FTX extended similar lines of credit to battered exchange Voyager facing its own liquidity struggles.

I find this set of distressed lending deals a bit puzzling. Viewed in a particular light, FTX could be capitalizing on the crypto downturn in a smart way by supporting important firms & laying the groundwork for attractive M&A, not unlike how Ken Griffin’s Citadel hedge fund grew so successful in the early 2000s. In a different light, it’s difficult to see how lending money to distressed colleagues & buying options to buy companies advances FTX’s long term strategy. Why not buy BlockFi outright now for pennies on the dollar? Why pay extra to wait & see how the company performs with less overall control?

To me, FTX adopting an option strategy over a full acquisition of BlockFi signals it’s not fully sure how crypto could perform in the short term & doesn’t want to commit significant capital until stability returns. Doubling down on distressed crypto firms - even at depressed prices - still poses significant risk to an exchange like FTX, making the investment dilemma a hard one to overcome.

The Dilemma Part 2 - TradFi

Tackling a crypto M&A strategy alone would be an immense challenge in this market, even with a sizable cash position. If that wasn’t enough, FTX has also signaled an intense focus on traditional market structure through partnerships, organic investment & rumored M&A measuring in the billions of dollars.

FTX’s TradFi foray began with its purchase of derivatives clearing unit LedgerX in late 2021 for an undisclosed sum, followed by the launch of FTX Stocks, the purchase of brokerage services provider Embed Financial and a ~$100M IEX investment in early 2022. These deals have set FTX on a path to become an all-in-one retail trading platform across crypto, equities & futures while preparing for a scenario where digital assets become securities in the US - another set of moves I generally agree with.

Then there’s Robinhood. Rumors have swirled for months that FTX has been weighing a purchase of Robinhood, which would mark an emphatic entrance into the TradFi retail arena if it materializes. Competitors, retail users & regulators across traditional market structure would have no choice but to take FTX’s advances seriously if a deal were to happen, and a more than -50% drop YTD makes HOOD more affordable.

Despite the rumors & excitement, I put chances of a FTX-Robinhood tie-up at next to none for a number of reasons. First, the deal would stretch FTX’s balance sheet considerably given Robinhood’s ~$8 billion price tag, more than twice what the exchange has said they have available for acquisitions. Second, FTX has publicly stated through the launch of its retail brokerage service that it will not take payment for order flow, a controversial practice for some that also accounts for the vast majority of Robinhood’s revenue. It would surprise me a great deal if FTX were to change their mind on something as closely watched as PFOF by buying Robinhood after only a few months.

The biggest obstacle to an FTX-Robinhood merger, however, comes from the still recent purchase of ~8% of Robinhood’s shares by Bankman-Fried himself. if FTX does end up purchasing Robinhood in the near future, SBF will have to contend with accusations of insider trading, something I seriously doubt he or his firm want to risk. Did SBF buy shares of Robinhood knowing his firm would acquire the company shortly thereafter? Did his ownership of the stock influence FTX’s decision to sign a deal? Do regulators challenge him in court? With the amount of good press SBF receives for being a leader of integrity in crypto, I would be shocked if his firm buys Robinhood and risks a breakdown of this otherwise infallible public persona.

Closing Thoughts

To review, FTX finds itself with a new wave of crypto success, a boatload of cash in the bank, a vast ocean of assets to scoop up on the cheap, and a high-stakes dilemma for its future as a company. M&A has become a make-or-break part of remaining relevant as an exchange - ones who do it well can disrupt their industry overnight & reward shareholders for decades. Ones who misuse resources or miss emerging themes quickly find themselves bloated, stagnating & irrelevant. Where will FTX find themselves after all their billions are spent?

If I were in FTX’s shoes, I would look for investments that fulfill both its goals at once - diversifying the exchange away from crypto AND supporting its existing business at the same time. One way to do this would be to buy retail users in adjacent asset classes & increase crypto market share with those users (a Robinhood deal would be this strategy in action). Another way would be to enter a space where crypto could disrupt the status quo & make investments to accelerate that disruption (gaming and music as examples). It could buy a TradFi market maker and marry its operations with Alameda’s. It could break into the blockchain-based carbon market. The list of potential deals & future businesses for FTX is dizzyingly long & grows by the day.

There is one deal, however, that I think could trump all others - OTC Markets Group, the ~$650M trading hub for the 12,000 or so OTC securities in the US. Here are a few reasons why I find this potential deal so interesting:

It diversifies FTX away from crypto: OTCM makes money by collecting and disseminating quoting & pricing information on the thousands of equities not listed on a Tier 1 exchange. Broker dealers who make markets in these securities are required to buy OTCM’s data in the form of recurring subscription fees, making the exchange’s revenue highly defensible and less correlated to crypto price swings. FTX could leverage OTCM’s relationships to improve its standing with TradFi broker dealers & regulators at the same time while expanding into the market data business, an exchange industry favorite.

It supports FTX’s existing business: There are a number of interesting ways FTX could use OTCM to increase crypto adoption. Most securities that trade on OTCM face liquidity issues - the vast majority of OTC stocks don’t see trading activity on a given day. If FTX and other exchanges start experimenting with tokenized stocks or other securities down the road, penny stocks & foreign ADR shares that trade OTC could be a great starting point. There’s also the surge in COVID-era penny stock trading to consider - OTCM could fulfill FTX’s ambitions of acquiring retail customers at attractive prices.

It’s “cheap” and fits within their M&A budget: To top it all off, OTC Markets Group sports an enterprise valuation of ~$600 million, making it a more than affordable option for FTX to consider. FTX could purchase OTCM at a healthy premium and still have plenty of capital to pursue other opportunities, and considering the exchange earns ~$30 million in annual income, it would be difficult to accuse FTX of overpaying at current prices.

Regardless of their ultimate decision, I’m excited to see how FTX can overcome its dilemma & put its war chest to work to as it continues on a path to market structure domination. It looks like SBF and his team are looking out for - and considering - all potential ideas…

Thank you for reading this issue of Front Month! If you’d like to read more of my market structure research & support my work, please check out my archive on Gumroad with over 20 articles & supporting financial models for the exchange industry. Please reply to this email or DM me on Twitter with any questions.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, SPGI, NDAQ and VIRT. I am also long LOOKS and SOL. I own NO shares of $OTCM and have no plans to purchase any shares in the immediate future.