Cracks In ESG's Armor

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

News

The ESG Mirage: On December 10 Bloomberg published a long piece on the current state of ESG that amounts to a scathing indictment of the industry & its primary beneficiary, MSCI. I’m honestly surprised how focused the piece is on one company even considering how influential MSCI is on the ESG space. I highly recommend reading the piece in its entirety, but here are the broad highlights:

There is no connection between MSCI’s environmentally friendly message & its ESG methodology. MSCI’s ESG criteria measure the climate’s impact on a company, not the other way around.

The ESG ratings business is unregulated by the SEC yet borrows terms & legitimacy from its regulated neighbor, the credit ratings business. A company with a BBB credit rating is considered “investment grade” - a company with a BBB ESG rating is considered average at best.

ESG ratings are relative to industry peers & not based on definitive, uniform sources of data. Companies can receive an ESG ratings upgrade without making any policy changes simply because its peer group changed.

Companies will also score higher on ESG metrics simply by following government mandates & avoiding fines. Bloomberg cited multiple examples of companies upping their ESG score by banning things that are already crimes, adding recycling bins to offices where it’s required by law, or adopting data protection policies where software is its primary business.

I’ve harped on the ESG Mafia in this newsletter for a while now - first by explaining the apparatus that Wall Street has built around it, then by examining how weak the product of ESG really is. I’m pleasantly surprised to see more journalists & media outlets notice & call out the ESG industry as it operates today. Cracks in ESG’s armor are becoming more apparent by the day.

At what point do articles like this begin to impact ESG stocks like MSCI, BlackRock & S&P Global? As cited in the piece, ESG interest & assets under management have grown so well because of the perception that investors can save for retirement & make the world a better place at the same time. If this perception changes & more people begin to reject the ESG narrative, will MSCI’s earnings expectations need to come down? The only stock I own with real exposure to ESG is BlackRock - I’m avoiding all others as the anti-ESG drum beat grows ever louder.

Blockchain Transaction Fees (“Gas”) on FTX: FTX wrote an interesting piece this week about the impact of gas fees on its operation & policies it plans to adopt to manage them. Most centralized crypto exchanges don’t interact with any blockchains when they process trades - they simply update entries in an internal database to transfer ownership of assets between users. It’s only when users send assets outside the exchange’s walls that an on-chain transaction occurs & gas fees are paid. Naturally, if more users wish to interact with expensive chains like Ethereum, the exchange will be forced to pay higher gas fees.

FTX lays out in this post that it plans to pass on more of this cost to customers depending on the blockchain & its transaction costs. Are you using high gas fee blockchains, making unnecessarily large amounts of transactions on-chain or transacting when the network is busy? FTX may not protect you from higher fees. Are you using cheaper chains like Solana or Avalanche instead? FTX will likely cover gas costs for these transactions as a reward. I find this post interesting considering Sam Bankman-Fried’s connection to Solana in particular - SBF has been open about his attraction to the chain & the industry leading speed & efficiency it offers. How can we forget the now famous “I’ll buy as much SOL as you have at $3” tweet or FTX’s partnership with Solana projects like Serum & Pyth? To the extent that FTX can accelerate Solana’s adoption by covering gas fees to interact with the chain, why shouldn’t it?

As we continue the intense debate around Ethereum & the so-called “Ethereum killers” one thing is becoming clear - everyone in the industry, including users, developers, traders and now exchanges - are taking sides.

My latest paid post is live - The Death Of Citadel is the first of a two-part series that explores the birth, near-death experience and ultimate dominance of Ken Griffin’s hedge fund/market maker conglomerate. Subscribers get immediate access to this post & a deep archive of past market structure research.

Thank you for your support!

Other Stories I’m Reading

CBOE CTO Eric Crampton Announces Resignation

Applying Artificial Intelligence to Trading

Doug Colkitt - CrocSwap & The Evolution of Markets

Robinhood Crypto Welcomes Cove Markets

CryptoDad’s New Title Implies He Works in Government. He Doesn’t

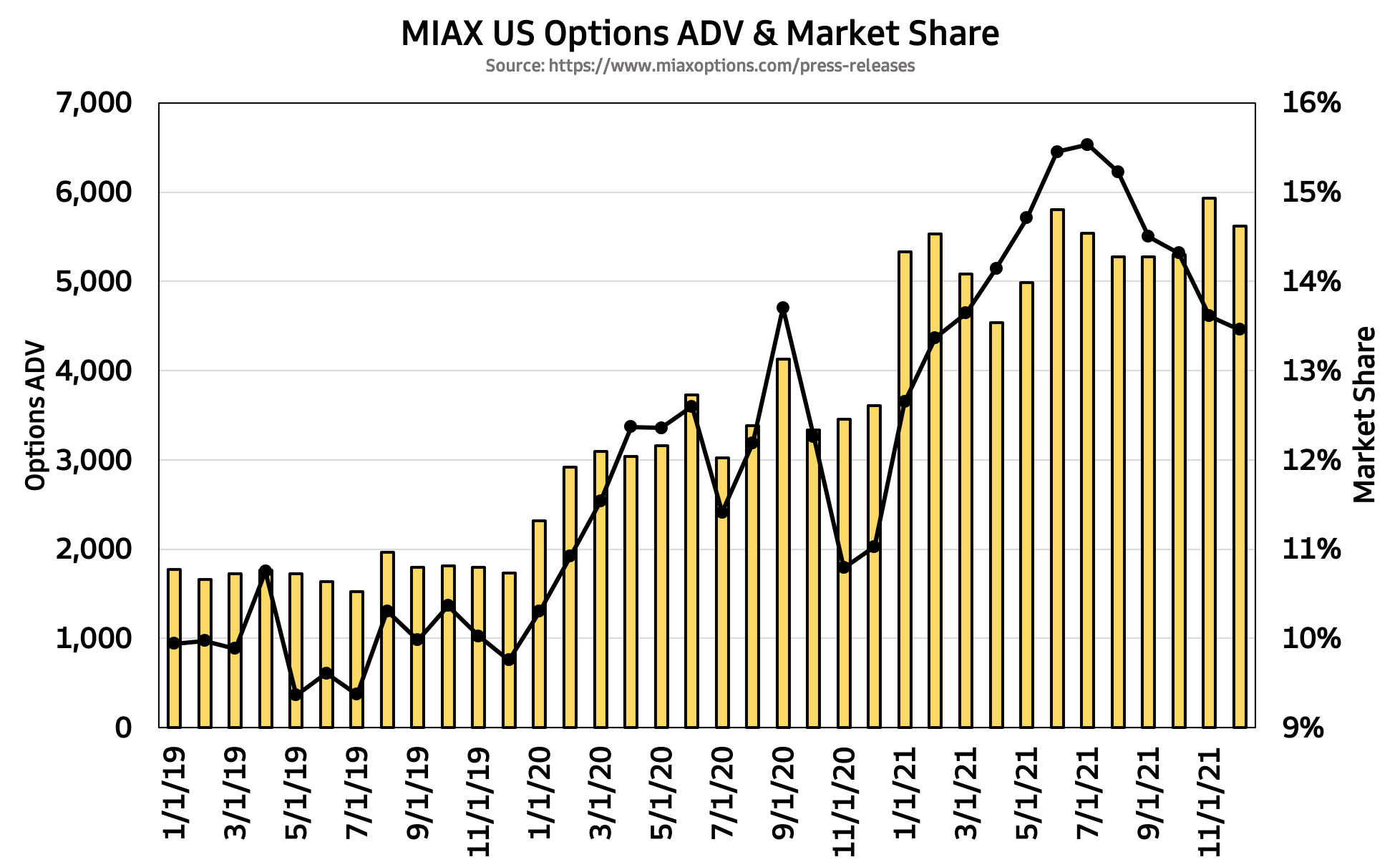

Chart of the Week

Up in Q1 and Q2. Down in Q3 and 4. MIAX’s options market share has followed a similarly cyclical pattern in 2020 and 2021 as it comes within striking distance of eclipsing the NYSE in market size. Surges in volatility & retail participation in the first half of both years may have contributed to the market share spike, along with successful equity rights programs that have allowed MIAX’s top market makers to participate in the exchange’s success. The exchange’s volumes are hovering near all-time highs despite share receding in recent months as overall activity refuses to slow down.

If this pattern holds, 1H 2022 may finally be the time when MIAX will cement itself as more than just an up-start options underdog.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Solana.