Binance Controversies Continue

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

News

SEC Probes Trading Affiliates of Crypto Giant Binance’s U.S. Arm: A recent update in Binance’s regulatory saga brings renewed spotlight to a powerful & controversial side of crypto market structure.

A big difference between crypto exchanges & traditional exchanges like the NYSE or CME is their blurred & sometimes direct relationship with market makers. To review, the role of an exchange is providing a safe & regulated venue to trade a certain product, along with maintaining the matching engine to process & settle trades that occur on its venue. Market makers partner with & operate on the exchange, taking the other side of trades & risking capital to collect the bid/ask spread. Exchanges & market makers need each other to stay in business - exchanges normally entice MMs to their platform with heavy fee discounts so they can trade as much volume as possible & improve a product’s liquidity, but they don’t share data and they don’t choose favorites. Whoever can trade the most volume & make the most money for the exchange, normally gets the best deals.

The emergence of modern crypto exchanges brought with them a radical concept - operating an exchange & a market maker under one roof. FTX & Alameda is the most famous example of this - Alameda is a massive crypto trading firm that makes markets on FTX’s spot & futures exchanges, and also happens to be owned by FTX itself. This can be very powerful because it cuts costs & helps FTX offer a more liquid market to customers, but if FTX and Alameda have special data sharing & fee relationships that other MMs aren’t privy to, conflicts of interest can form very quickly. No such conflicts have come to light so far, and, importantly, both firms are very clear about the nature of their relationship. Users and regulators have been comfortable with the situation as it stands today.

Which brings us to Binance’s US subsidiary, where it was recently revealed that a relationship between billionaire founder Changpeng Zhao and two affiliated market makers had formed without being properly disclosed. From the WSJ story above:

“Corporate documents from 2019 tie Changpeng Zhao, Binance’s founder and chief executive officer, to market makers Sigma Chain AG and Merit Peak Ltd, and former executives say that as of late last year Mr. Zhao controlled them both.”

(Source)

Eek. Not a good look for CZ.

Exchanges should (in theory) be rewarded for offering low transaction costs to users - if I can trade Bitcoin for a lower total cost on Binance than FTX, for example, I should give Binance my trade & future business. If CZ also controls two market makers that trade on Binance, it means he benefits when a user’s transaction costs are higher, not lower. Wide bid/ask spreads mean customers have to spend more money & sacrifice more P&L to trade a product, which benefits the market maker on the other side of their trade. As an exchange executive, this should not be what CZ should be compensated for, regardless of how large these two market makers are on the exchange today.

Will the SEC’s probe cause the agency to take a more firm stance on exchange-market maker relationships in general? That remains to be seen. In the meantime, it’s important for healthy competition to exist in the crypto exchange space & for users to be informed about the exchanges with which they do business.

(For more background on CZ’s career & Binance’s rise to the top of crypto, check out a free post I published on the exchange last year here)

Trading Powerhouse’s $320 Million Save Suggests It’s Crypto-Rich: Although this headline received plenty of attention when it hit the tape a couple weeks ago, I want to share my opinions on it because it’s too wild of a story to let slip by so quickly. A secretive high frequency trading firm with a long & distinguished resume single-handedly saved a critical part of blockchain infrastructure, like it was a normal Thursday afternoon.

What secretive HFT firm are we talking about? Jump Trading, a massive and, until recently, completely silent part of global market structure. Jump got its start in the open outcry pits of the CME & transitioned to electronic futures trading before most firms knew it existed, expanding to global FX, interest rates, options & even equities wholesaling in the decades that followed. If you were to ask Jump’s team about their TradFi activities, they’d probably change the subject to crypto, where they’ve become a much more outspoken supporter of blockchain infrastructure. With this $320 million infusion, Jump has emphatically put their money where their mouth is.

What exactly did Jump save? A messaging protocol by the name of Wormhole, which was built to connect disparate blockchains & allow them to transfer information between each other. Wormhole deploys smart contracts on blockchains like Ethereum, Solana, Avalanche & Terra that send & receive data between each other, allowing users to jump from chain to chain without having to use a central intermediary like an exchange to swap assets. Here’s a short video explaining the protocol in more detail if interested:

Two weeks ago a hacker found and exploited a bug in Wormhole’s code and stole $320 million in crypto, threatening the stability of Wormhole itself & the thousands of users who rely on the protocol to trade & interact with DeFi apps on each chain. Jump immediately responded with an infusion of capital to keep Wormhole secure & began working with developers to find & retrieve the lost funds.

This nine figure infusion implies three important points:

Jump had a spare $320 million in crypto lying around to send to Wormhole on a moment’s notice.

In order for that much spare crypto to sit on Jump’s books without making the firm stretched for cash or over-exposed, the company likely has multiples of that in working capital & annual income from its market-making & trading businesses.

Jump sees an incredible short and/or long-term future for crypto & Wormhole specifically.

If Jump wasn’t expecting a return significantly above the $320 million it used to save Wormhole, if it didn’t have many multiples of that already at stake, why would it have parted ways with that much money so publicly?

I view this news as validation that significant value remains to be captured in crypto market structure, and that Jump has positioned itself to capture a huge chunk of this value over time. Even with a few $300 million checks written every once and a while…

If you like this free newsletter I invite you to subscribe to Front Month Premium where I post more high quality exchange & market structure research each month. The premium archive now has 18 articles on topics like FTX, Robinhood, Citadel Securities & more that instantly become available to paid subscribers.

Thank you for your support!

Other Stories I’m Reading

NYSE Wants to Be Marketplace for NFTs Just Like With Stocks

2022 Market Volatility Demands a Greater Premium on Liquidity

Tradeweb Announces Changes to Board and Succession Plans for Executive Leadership

Bakkt, Once Wall Street’s Hot Crypto Play, Has Cooled

Retail investors lose out when brokers sell their orders, Dutch regulator warns

Chart Of The Week

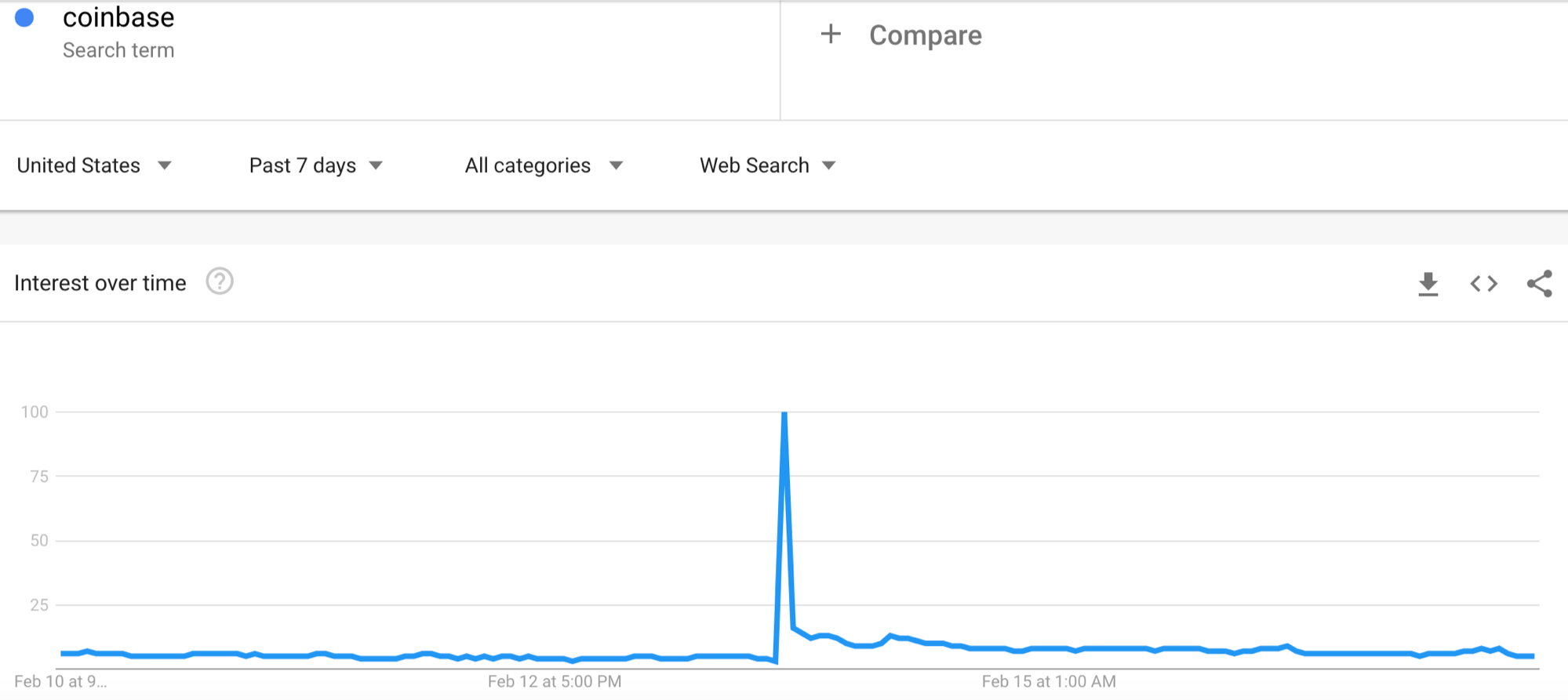

Last Sunday’s Super Bowl broadcast drew its biggest viewership in the last five years. Crypto companies from far and wide dipped into their coffers to run ads during the game, putting their brand in front of 112 million sets of eyeballs in one of the most watched events on television. Among the crypto brands vying for attention was FTX, which ran a Larry David montage about human progress through the ages. There was eToro, showing an ad about the power of social investing. None likely drew as much attention, however, as Coinbase’s spot, which showed nothing but a bouncing QR code on screen for a full minute before showing its logo & cutting to black.

The frenzy of crypto ads during a choppy time for most coins led many to reference the Dot-com bubble ads shown during the 2000 Super Bowl, implying a potential repeat of history. While we may be in a frothy time for most coins & blockchain projects, I don’t think we should be connecting the two eras together for one main reason - the crypto exchanges who ran ads are already incredibly profitable. What’s more, these retail-focused exchanges need a steady stream of new sign-ups to drive growth, which makes innovative marketing one of the most critical parts of their strategy. Super Bowl ads still show good returns on investment despite the high price tag - social following, product interest & sales normally spike after a successful ad runs.

Take Coinbase for example - in the hours after its QR code spot ran, its app rocketed to #2 on the app store, Google search interest exploded & the exchange saw so much web traffic that its app crashed. It’s too early to see how the ad will impact its volume in the coming weeks, but initial results look promising:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, SPGI, NDAQ and VIRT. I am also long Solana.