The Usain Bolt of Electronic Trading

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

On August 16th, 2009, Usain Bolt made history.

It was a clear night in Berlin as the eight runners approached the starting block. The IAAF World Championships had entered its 2nd day of competition, and a packed crowd eagerly awaited the 100 meter sprint finals. There were many familiar faces among the athletes, but none more iconic than that of Usain Bolt, the now eight-time Olympic gold medalist fresh off a 2008 Beijing victory in the same event.

Analysts & spectators were concerned with one question & one question only - would they witness another world record fall that night? The fastest 100m sprint at the time was 9.69 seconds, held by Bolt at the '08 Olympics. Was tonight the night this record would fall?

"On your mark."

"Set."

(Source)

Usain Bolt not only beat his previous world record, he smashed it. 9.58 seconds to this day remains the fastest 100m sprint of all time, solidifying Bolt as one of the best runners to have ever lived.

I find this race interesting because apart from being a thrill to watch, it reminds me of today's electronic trading landscape. Every time a mis-pricing occurs between different markets or a trade opportunity is spotted, a dozen or so high-speed trading firms make their way to the starting block. The gun sounds, and the fastest firm to the trade collects their profit and becomes rich. These races happen thousands, if not millions of times per day, and there are no prizes for second place.

Who is the Usain Bolt of electronic trading? There are clues that lead me to believe it's Jump Trading, a low-key but well-respected Chicago HFT firm that’s been around for over 20 years.

Every word you’d use to describe an HFT firm applies to Jump Trading, and then some. Jump isn’t just secretive - it barely has a website, consistently turns away media requests, and once nearly sued Twitter to reveal the identity of an account posing as a former employee. It isn’t just successful - it routinely brings in hundreds of millions in annual trading profits. It isn’t just sophisticated - it employs an army of PhDs and buys the best equipment to shave seconds off its sprint time. Jump Trading is the HFTest of HFT firms, and its impact on present day Wall Street & markets of the future cannot be overstated.

From The Pits To Light Speed

Not unlike many other successful trading firms & some of its present day rivals, Jump’s story began in the loud, crowded pits of the Chicago Mercantile Exchange. Paul Gurinas and Bill DiSomma, two experienced floor traders who met in the FX pits in the early 90s, decided to work together to trade CME’s latest product: e-mini S&P 500 futures. At the time, CME’s S&P 500 contract, sized at 500x the equity index, was becoming too expensive for all but the biggest traders to manage. The e-mini contract, listed at 1/10th the size of the original, drastically opened up the range of interested customers willing to trade & make markets in the product.

Apart from smaller contract sizes & easier access to liquidity, the e-mini contract had another feature that interested Gurinas & DiSomma - integration with Globex, CME’s new electronic futures trading platform. A semicircular ring of computers were installed around the pit allowing traders to arbitrage the new e-mini contract with its older counterpart. One trader would stand in the pits & trade one market while another would man the computer in another market, offsetting the pit trader’s positions for a risk-less profit. Gurinas & DiSomma executed this strategy with impressive success as Globex & the e-mini contract grew in stature.

(Source)

With their first electronic trading strategy showing good returns, Gurinas & Disomma began to get serious about the screen’s role in the future of market structure. In 1999 the pair decided to start their own firm, called Akamai Trading, with fellow pit trader John Harada. The trio spent the next several years experimenting with Globex and the new strategies that came with it, trading right through the rise & bursting of the tech bubble. In late 2001 Harada left to start his own firm, and Akamai changed its name to Jump Trading in early 2002.

Jump’s success to this point had always been closely intertwined with the CME, but their futures would merge even closer together when William Shepard, a CME board member, bought a passive stake in the firm around the same time Harada left. Shepard is still a member of the board today.

Should an exchange board member be allowed ownership in one of its largest customers? I’m torn on this issue. On one hand, exchanges were initially created to serve their trader customers. Brokers & firms like Jump outright owned the exchange until they demutualized and became public companies in the early 2000s. Exchanges and their top traders should have a shared interest in each other’s success, right?

On the other hand, CME serves a wide swath of retail traders & institutions apart from Jump, not to mention public shareholders, and other HFT firms don’t have Shepard as an investor.

Regardless, we can’t view Jump Trading’s rise to power in the early 2000s without acknowledging its close working relationship with the CME. Jump was one of the first HFT firms to become a CME clearing member, allowing it to get the best exchange fee rates in return for higher capital contributions to the clearinghouse. It then expanded market-making & trading activities far beyond e-mini S&P 500 futures, setting up units for CME’s interest rates, energy, and FX markets.

With the lowest fees & a close exchange partnership in tow, Jump could turn its focus to speed. As we’ve reviewed before, many strategies that involve collecting risk-less profits only work for the first trader to spot & act on the opportunity. Markets were waking up to a new electronic future, and Jump started to attract competition. Speed became one of the single most important advantages Jump had over rival firms, and it spent enormous sums ensuring it became the Usain Bolt of electronic trading. It hired quants and developers from the ranks of Google & Facebook, ex-traders from Citadel & other prop shops, and PhD students from local Illinois universities. It built relationships with different exchanges around the globe, from local venues like CBOE and CBOT to Germany’s Eurex & the London Stock Exchange. To connect this vast network of end markets, Jump paid to house servers inside exchange data centers & bought microwave towers that transmitted messages between all these data centers at near-light speed. The amount of investment needed to build & maintain a network like this is mind-boggling, which puts a HFT’s profit potential into even greater context.

For many years, Jump built its high-speed empire with little to no public attention. It traded its own money and its owners avoided a flashy lifestyle. Mainstream investors only got small glimpses at the extent of the firm’s success in the form of legal filings, required public disclosures and regulatory reports. In 2008 a Jump subsidiary reported over $300 million in operating profit. In 2010 profit had slipped to ~$260 million on lower volatility, with revenues reaching in excess of $500 million. In 2012, Jump & Citadel fought in court over trading secrets; the fight revealed that some of Citadel’s strategies were becoming less profitable, and Jump competitive pressures may have been the cause. When the CFTC began cracking down on market manipulation & spoofing in the futures markets, it approached Jump for advice.

While executives hadn’t graced the front page of any newspapers or Congressional hearings, just outside the spotlight Jump had secured its position as one of the wealthiest, most influential firms in high frequency trading.

Crypto’s Top Doge

For all the strict tight-lipped policies about its activities & interests, Jump Trading is quite vocal about one asset class in particular: crypto. Despite not talking to the media & not having a website, Jump does have a podcast where executives talk about blockchain, DeFi, and their involvement in the crypto trading space.

Why is Jump so outspoken about crypto when it’s secretive about every other market? I believe this has to do with crypto’s relative youth as an asset class. In mature markets where competition is more intense, it’s in Jump’s best interest to keep their agenda a secret to protect their share of a hard-fought trading pie. In crypto however, it’s currently in Jump’s best interest to grow the pie rather than defend their share of it. If more institutions join the asset class & trading volumes grow, Jump stands to benefit considerably regardless of competitive pressures.

The HFT firm’s crypto hype has turned out to be more than just talk. Jump’s interest in the asset class began in the early 2010s as a recruiting tool - the firm set up internship programs with local colleges to get developers interested in working for Jump with crypto research as the selling point. By 2015, the data this research was producing became so valuable that Jump couldn’t sit on the sidelines any longer. It launched a crypto trading unit later that year, quickly growing to become a top market maker on BitMEX and Bitfinex with a significant passive & active trading presence across the market.

Jump Trading’s share of the crypto universe is now so big that it’s becoming difficult for them to avoid the spotlight. Take Robinhood for example - Jump serves as the primary market-maker for the retail broker’s crypto order flow, absorbing trades by the thousands on everything from Ethereum to Dogecoin. What’s interesting here is Citadel Securities, the infamous wholesaler paying for Robinhood’s equity & options order flow, has intentionally avoided the same service for crypto, allowing Jump to fill the gap.

We’re even seeing Jump invest in emerging crypto startups. In late 2020 Jump bought a stake in Serum, a decentralized exchange built on the Solana blockchain, with FTX founder Sam Bankman-Fried as its project lead. Jump’s President David Olsen says investments like these happen less as a VC looking to turn a profit but more as a customer looking to build a better product for his firm. Olsen has quite a bit to say about Jump’s vision for DeFi too:

“We’ve talked about the institutionalization of the crypto market and have used Bitcoin as a short-hand for that. That’s an exciting theme that’s going to play out for years, but in our opinion the more exciting theme is the institutionalization of DeFi, and how the intermediaries, the rent-seekers in financial markets that exist today could very well be disrupted by parties being able to interact directly on-chain and have a safe solution to do that.”

(Source)

If crypto-maximalists are right and the blockchain economy rivals the real economy in size one day, Jump Trading is in a position to become as powerful & influential as Ken Griffin’s Citadel is today.

The Fastest Race On Earth

It’s safe to say that high frequency traders are currently engaged in the fastest race on earth, and are using all means necessary to win.

For years the best strategy was fiber optic cable laid underground in as straight a line as possible between exchanges & trading firms. Then it evolved to microwave towers, shooting data into the atmosphere and reflecting it back down to its destination. Now we’re hearing rumors of trading firms launching satellites into space to send trades across continents with even greater speed & efficiency.

Each time the public gets word of a new upgrade, Jump Trading always seems to be mentioned as an early adopter. The best equipment is always required if they want to maintain the title of HFT’s Usain Bolt. With their involvement in almost every asset class in existence, including a massive presence in crypto, we may soon be hearing quite a bit more about Wall Street’s speediest trading firm.

Honorable Mentions

On May 13 S&P Global and IHS Markit announced its planned divestiture of OPIS, an energy data provider, and its Coal/Metals/Mining business to satisfy antitrust regulators & keep its merger on schedule.

After launching on May 3, CME’s micro Bitcoin futures product has so far traded more than 100,000 contracts, putting it near the top of the exchange’s list of best product launches of all time.

On May 10, Robinhood’s new weekly podcast “Under the Hood” published a conversation between Vlad Tenev and Virtu CEO Doug Cifu on market making, payment for order flow, and its impact on retail investors - it’s worth a listen.

Chart of The Week

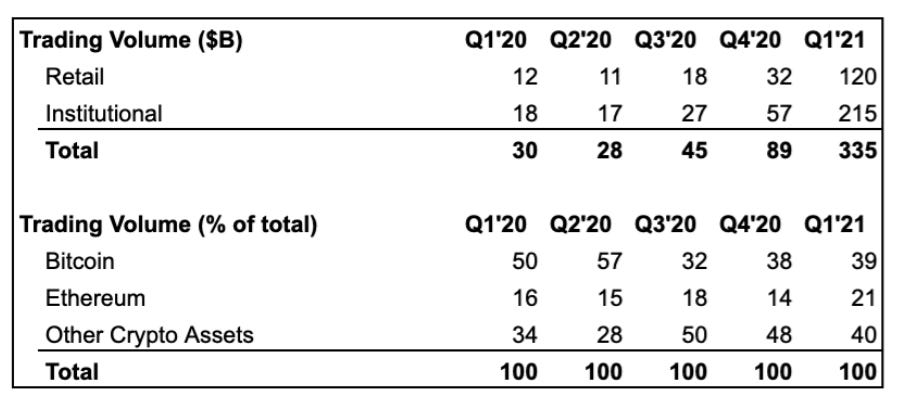

After the market closed on May 13 Coinbase reported earnings for the first time as a public company. When looking at Q1 by itself performance was largely as expected - revenue & earnings ballooned in 2021 driven by the massive run up in crypto prices & interest. 56 million users have now signed up for the exchange’s services & over 6 million retail users are now making transactions on a monthly basis. Net income grew an astounding +2,400% year over year, a testament to the impact a bullish crypto market can have on Coinbase’s trading volumes.

Forward guidance given during the earnings call is where things really get interesting. First, Coinbase announced they’re planning to list Dogecoin for trading in ~6-8 weeks time, which should capitalize on the meme’s current buzz & add to the exchange’s active users. Second, and more importantly, it gave guidance for trading volumes & MTUs to be at or above Q1 levels. As the chart shows below, Q1 levels were insanely strong, and Coinbase management signaled this quarter to be more of the same.

With the stock now down more than -20% from its IPO day, and with volumes & user interest staying strong, I’m beginning to get interested in starting a Coinbase position. I still think there are long term headwinds for the company particularly around its eye-poppingly high retail trading fees, but crypto volatility is stretching out longer than I had originally anticipated and valuations have become more reasonable.

(Source)

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Bitcoin and Uniswap’s UNI governance token.