Amaranthology

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

On the afternoon of September 7, 2006, an urgent email hit Brian Hunter’s inbox from fellow energy trader Shane Lee.

“Tell me if I’m wrong, but we have 3 choices here.

(1) Shut down and start energy fund, lose 0.3 to 1.0 getting out, and have great future potential. However, if we lose that, who is going to want in on the energy fund? If h/j drops to 1.50 or worse, the deferred positions are all going to get obliterated too.

(2) Jump back in and help this market out. Risk losing some investors due to risk profile, but manage along until we get the proper catalyst to exit positions…

(3) Sit and wait. Let market take its course, find natural fixed price demand.

There is no catalyst right now. That’s the problem. You exit this size without one (without exiting every positions in your book), and we got a big problem…

All I know is I am personally 1 more bad day away from stopping out...can’t afford to drop below 30 for my family.”

(Source)

Hunter and Lee were beginning to realize the precarious position they and their hedge fund, Amaranth Advisors, had found themselves in. Their sizable energy portfolio had bled $200 million in just over a week, and more pain looked to be on the horizon. Faced with the prospect of massive, potentially career-ending losses, the pair decided to follow path #2 in Shane’s email above, and increased their exposure in the following days.

Two weeks later the fund’s losses amounted to a stunning $4.1 billion. Margin calls quickly followed, and Amaranth was forced to close its doors for good.

In a few weeks we’ll celebrate the 15 year anniversary of Amaranth’s spectacular blowup, which to this day remains one of the largest in history. Years of Congressional hearings & investigations would reveal the events & decisions that led to that now famous two week period in September, and end with a complete overhaul of the derivatives industry. Exchanges, HFT firms and retail traders alike are all still feeling the impacts of Amaranth’s blowup to this day, whether they credit its ghost or not.

I want to spend some time looking back at Amaranth’s stunning rise & equally stunning collapse for two reasons:

1. It’s an incredible story, and

2. It touches on so many important exchange & market structure themes that we’d be wise to remember.

Let’s begin:

Brian Hunter’s Wall Street Birth

The first act of Brian Hunter’s career as a trader can be described as nothing short of magical. Hunter made early waves as an energy trader at TransCanada, a $40 billion energy pipeline company, in the late 1990s. His ability to spot mispricings in natural gas options made TransCanada millions in profits & attracted the attention of Wall Street trading giants. In 2001 Hunter joined the Deutsche Bank energy desk where his name as a high-risk but talented trader continued to rise.

Between 2001 and 2002 Hunter made $70 million in trading profits for the bank, using the same techniques & instinct developed at TransCanada in the natural gas markets. Bank trading desks are a unique working environment - the “eat what you kill” mentality at most desks means the difference in compensation between the best & worst traders can be extremely wide. By age 27 Hunter was making nearly $2 million in salary & by 29 was running the entire natural gas trading desk. Banks are also a unique place where $2 million in compensation may not satisfy - many could argue Hunter was still being underpaid given his $70 million haul.

2003 saw a similarly stellar start to the year, until “an unprecedented and unforeseeable run-up in gas prices” turned Hunter’s healthy YTD performance into a $50 million loss in one week. Deutsche Bank demoted Hunter and withheld his bonus that year, and by 2004 his relationship with the bank had become irreparable. Hunter left the firm & filed a lawsuit against his former employer for withheld compensation and defamation.

Despite his recent bout of losses & legal battle with Deutsche Bank, Hunter was quickly hired by a Connecticut hedge fund with ~$8 billion of assets under management - Amaranth Advisors. Amaranth was a “multi-strategy” hedge fund, meaning it traded many different types of markets & strategies to make a profit, including long/short equity, credit & merger arbitrage, and primarily energy trading. Hunter was given a portion of Amaranth’s funds, a risk team to watch his back, and the goal of making as much money trading natural gas as possible.

And that’s precisely what he did.

This post is an example of the kind of content you can expect from Front Month Premium, the paid portion of this newsletter where I explore the companies, stories, and catalysts affecting the future of exchanges & market structure. Subscribers get immediate access to a long list of exchange research & at least two new posts per month.

Thanks for your support!

Brian Hunter’s First Billion

Hunter began his work with Amaranth at an important time for the natural gas industry. Two exchanges - NYMEX and ICE - were engaged in an intense battle for US market share at the time. NYMEX was the largest natural gas futures market, offering trading & clearing of products designed to hedge against & profit from large price moves. ICE, on the other hand, was a completely unregulated electronic swaps platform that offered similar products to NYMEX but operated outside of CFTC jurisdiction.

Many types of participants used both NYMEX and ICE to trade natural gas. A key source of trading activity came from producers & storage companies, who used futures & swaps to hedge their exposure & lock in profits for their business. Natural gas is cheap in the summer & scarce in the winter - companies exist to buy & hold gas through the summer and then sell it in the winter when prices go up. These companies use futures to ensure they can sell gas for a price that covers their costs & takes risk out of their operations.

Apart from energy companies, speculators like Brian Hunter & Amaranth were active in the market to buy the risk these energy companies were selling. For example, let’s say a storage company could lock in enough profit to fund its operations with gas at $4.00 per 10,000 MMBtu’s. So it sells a futures contract at $4.00, guaranteeing that it can sell its stored gas at that price when the contract expires. Amaranth would buy this contract from the energy company. If the price of natural gas was lower than $4.00 at expiration, Amaranth would lose money because it would have to buy gas from the energy company at a higher than market price. If prices were higher than $4.00, everyone would win - the energy company would still make its desired profit but Amaranth would also profit by buying gas at below market prices. Amaranth performs a key function in this example by taking on market risk & assuming the profit or loss potential the energy company doesn’t want. Most markets can’t work without speculators willing to take on risk. This is how Amaranth & Brian Hunter engaged with the natural gas market in the mid-2000s, using both NYMEX and ICE to put their massive energy portfolio to work.

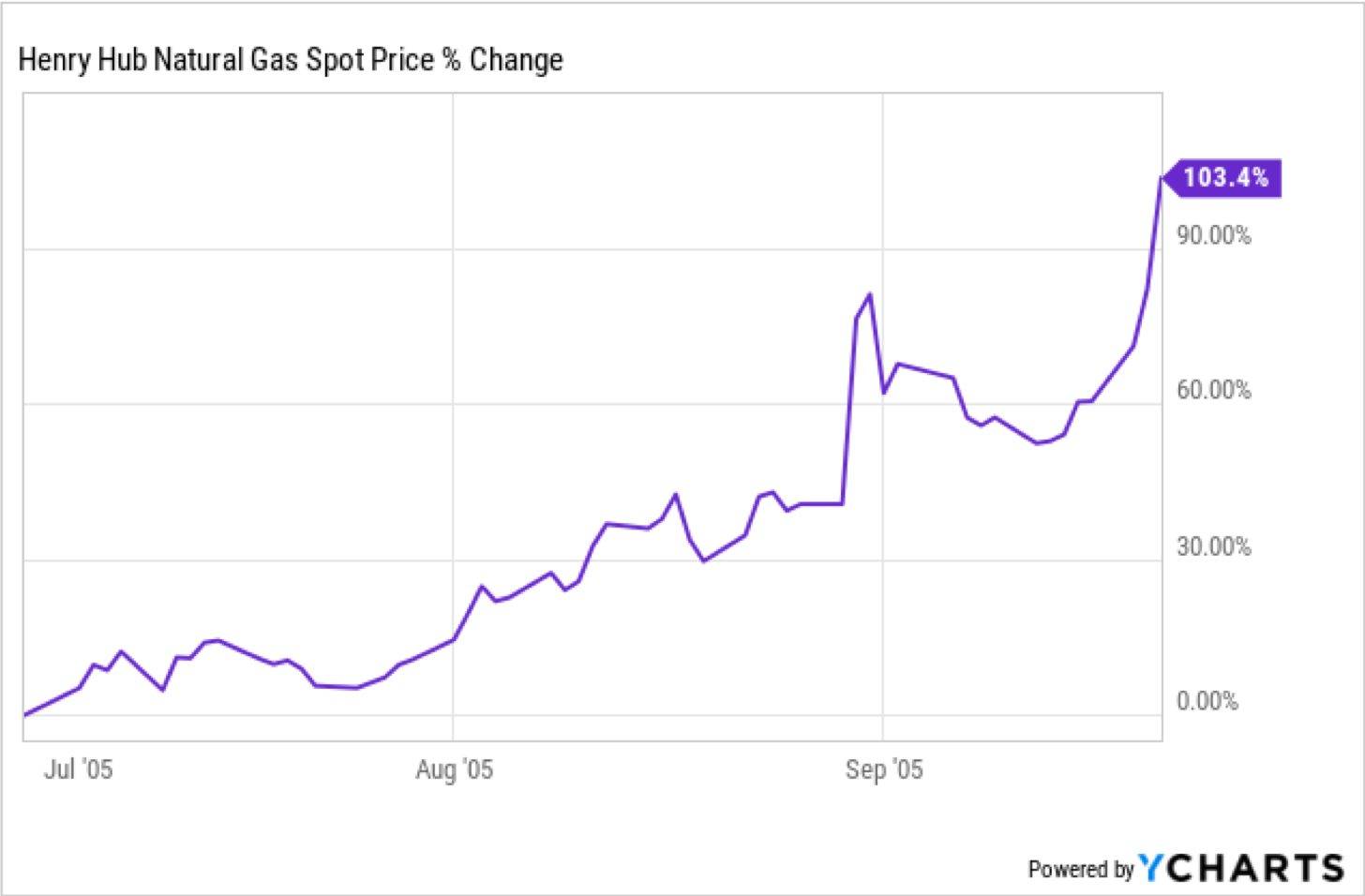

2005 served as the pinnacle of Hunter’s trading career. Employing the above strategy (called “long winter, short non-winter” in the industry), Hunter & the Amaranth energy desk made a $1 billion profit in 2005. The price of natural gas more than doubled in the fall of 2005 as lower gas production combined with hurricanes Katrina & Rita created much tighter supply conditions than the market expected. Natural gas prices topped out at over $14.00 per 10,000 MMBtus in late 2005, a record high in the US to this day.

(Natural gas spot market, July - September 2005)

As a reward for his extreme success, Hunter (now 31 years old) was paid between $75 - $100 million in compensation that year. His reputation as a legendary energy trader had been cemented across Wall Street for good. He was allowed to move back to Canada with his team to trade from home, and the risk team in charge of managing his trades loosened their supervision over his account. If Hunter’s life was a movie, this would be the part where he gets on his horse and rides off into the sunset, big bags of money thrown over his shoulder.

But, like most of us (and especially traders), Hunter didn’t know when to stop. He didn’t have a number in mind that served as “enough”. As 2006 came into view, the trading - and extreme risk-taking - continued.

Brian Hunter’s Downfall

Coming off its legendary year in the natural gas market, Amaranth returned in 2006 with more heavy betting that prices would rise sharply in the fall & winter, similar to 2005. They took massive long positions in natural gas futures & swaps on both NYMEX and ICE, brushing up & ultimately blowing way past normal fund risk limits. At one point Hunter’s trading desk held more than 1 trillion cubic feet of natural gas futures, representing nearly 1/4th of annual US residential gas consumption.

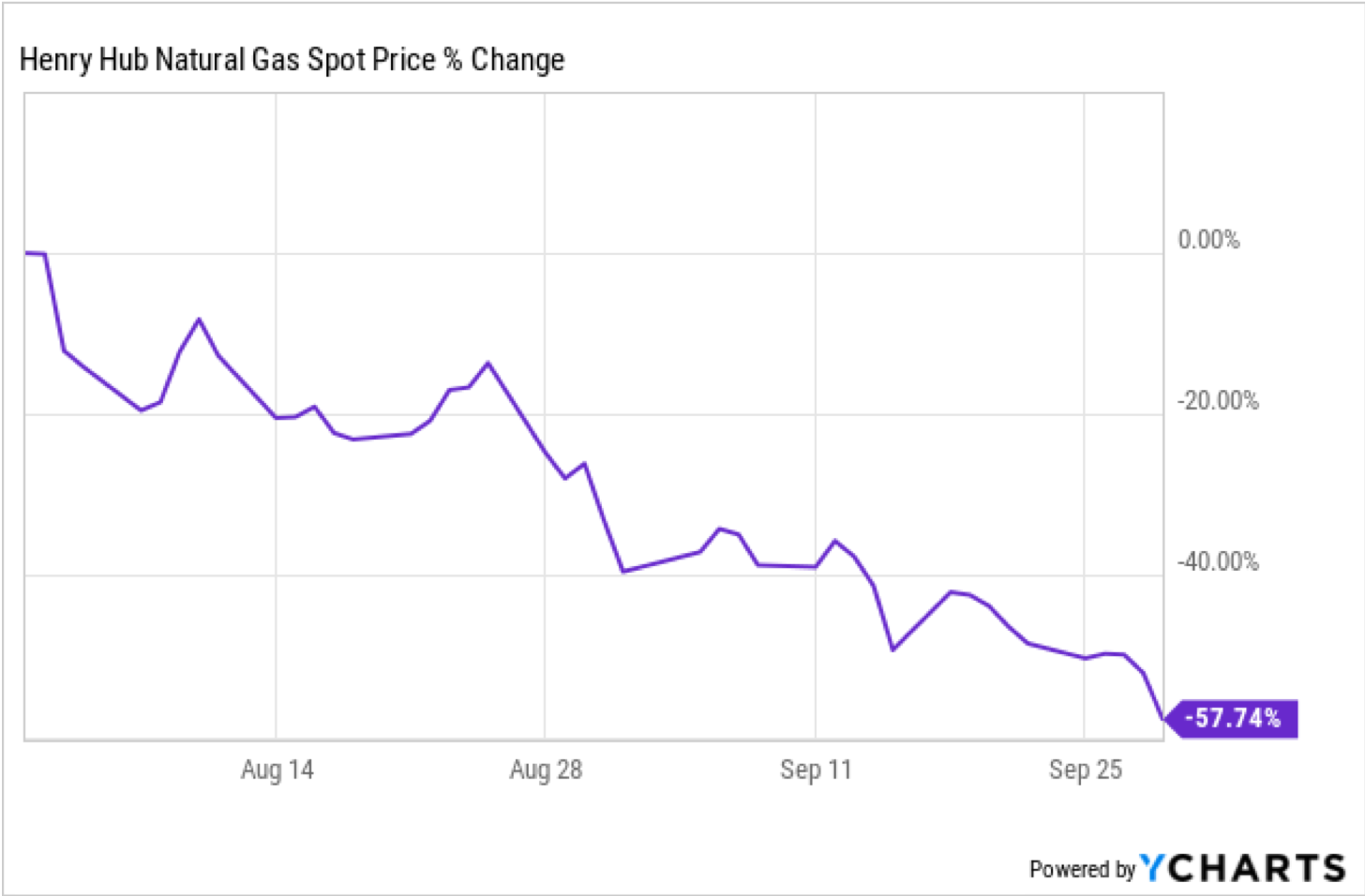

Amaranth’s bets towered above any other market participant and began giving NYMEX cause for concern. The exchange repeatedly warned the fund about their excessive position sizing & demanded that they scale back aggressively. The more NYMEX pushed Amaranth to reduce exposure, the more the fund simply moved money to ICE’s swaps market where regulators couldn’t reach. By mid-August 2006 Amaranth held an $8 billion net long position in natural gas futures & swaps across NYMEX and ICE, equal to 100% of the fund’s AUM. Brian Hunter’s risk team & senior management allowed this position to grow throughout the summer, ignoring routine procedure & trusting Hunter to repeat his billion dollar magic trick. All eyes turned to the spot market - would cold weather, hurricanes & supply shocks send natural gas prices spiking as they did one year prior? Would Brian Hunter do it again?

(Natural gas spot market, July - September 2006)

Bloodbath.

Brian Hunter’s $8 billion bet quickly soured as August bled into September and gas prices continued to fall. The catalysts he was looking for - cold weather, supply shocks, higher demand - simply weren’t materializing. A few million in losses became hundreds of millions in a matter of days, prompting that nervous email from Shane Lee weighing Hunter’s options. There was simply no other way to view the situation - Hunter was wrong when everyone assumed he’d be right. Pure euphoria the year prior had now become sheer terror, and this time the fund was more exposed than at any point in the past.

Losses weren’t Amaranth’s only problem - the fund’s positions were so big, it had no way of unwinding its bets quickly or even at all. Unloading 1 trillion cubic feet of natural gas inventory quickly isn’t something easily done. It would take months of forced selling to get the fund out of this trade, and by then it would be too late. The only way for Amaranth to survive would be for the market to turn around. And the market was not turning around.

On September 15th Amaranth got a call from the CFTC about $4 billion in rumored losses. The game was over. Two days later, Amaranth sold off its energy portfolio to Goldman Sachs, JP Morgan & Citadel to pay its margin call. Faced with no money, angry investors & looming regulatory crackdown, Amaranth quickly closed its doors for good.

Brian Hunter’s Lasting Impact

On September 17, 2007 - the one year anniversary of Amaranth’s firesale - Michigan Senator Carl Levin introduced a bill that would bring electronic energy exchanges like ICE under CFTC authority. After months of Congressional investigation & debate, Levin’s bill was officially signed into law. ICE was now held to the same regulatory standards as its NYMEX counterpart, now owned by CME. Amaranth’s blowup would continue to influence legislation like Dodd-Frank & other bills after the 2008-09 financial crisis, pulling even more off-exchange, dark markets into the light. The exchange industry cheered these regulatory moves as it improved their image as the safe, controllable way to run markets, and their stocks rode the wave of new products & fees they were able to collect.

Even ICE, the perceived loser of the Amaranth saga with more regulatory burden, continued to crush the S&P 500 in the following years:

Brian Hunter never served jail time. After sparring with the CFTC and other regulators for years in the courts, he was finally punished with a minor trading ban & a $750,000 fine, unusually light for such a high profile blowup. Amaranth’s executives got off relatively scot-free as well, and after laying low for a few years reunited to open a new hedge fund, called Verition. The fund is still active today.

Fifteen years later we’re still facing many of the same challenges surfaced during the Amaranth debacle. Traders are still blowing up using excess leverage, off-exchange products & regulatory grey areas, and these same traders are largely escaping serious punishment. Regulators are still trying to corral every market they can touch under strict control, and they’re still using exchanges as their main regulatory tool.

My guess is the next time a Brian Hunter-esque character risks it all and loses, we’ll see the same decades-old reactionary cycle spring into action. Today’s environment looks ripe for excessive risk taking to spur another regulatory crusade that will see the wrong-doers survive unscathed & exchanges the owners of even more market power.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, COIN and VIRT. I am also long Bitcoin, Ethereum, Uniswap & Solana.