The Archegos Supernova

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

A supernova is the final, explosive act of a dying star.

When a supernova begins, a star emits massive amounts of energy & light that make it clearly visible from millions of miles away. Below is an image taken from the Hubble Space Telescope in May 1999 capturing a supernova in the lower left-hand corner. The explosion’s intensity rivals that of the galaxy itself:

(Source)

{kind=link}

On Friday, March 26, the galaxy of Wall Street experienced its own supernova that has since captivated markets & regulators. Although not at risk of endangering the galaxy by itself, this supernova comes with serious implications for banks, exchanges & global market structure, and could be a sign of more explosions to come.

A Wounded Tiger Cub

The supernova in question comes from Bill Hwang & his now infamous firm, Archegos Capital Management. Hwang’s career began as a rising star in the shadow of legendary hedge fund Tiger Management, lead by Julian Robertson. Tiger launched with $8 million under management in 1980 and grew into the world’s largest hedge fund in the late 90s with over $20 billion is assets. After working at Tiger from 1996 to 2000, Hwang launched his own Asia focused fund in 2001 with backing from Robertson, giving him coveted “Tiger Cub” protegé status.

Robertson’s blessing turned into stellar success for Hwang & his fund. By 2007, Tiger Asia had over $8 billion in assets and boasted returns in excess of +40% annually using a classic long/short strategy developed at his predecessor. Hwang had struck out on his own & became a Wall Street superstar in his own right.

The 2008 financial crisis saw Hwang’s good fortune reverse as returns began to lag & client defections increased. Tiger Asia’s performance followed the global markets lower and ended 2008 with a -23% return. The years afterward gave Hwang no reprieve. As stocks bounced back from crisis lows, Tiger Asia posted returns of +3% in 2009 and a mere +0.5% in 2010. Meanwhile, assets under management continued to shrink, ending 2011 under $2 billion.

The bottom fell out of Hwang’s situation when US and Chinese regulators opened investigations into his firm, alleging insider trading & market manipulation in various Chinese bank stocks. The firm paid fines to settle the charges out of court, but the reputational damage was irreversible. Tiger Asia returned outside money & became a family office in 2013, changing its name to Archegos Capital Management. One of the industry’s brightest stars had been tainted & nearly snuffed out.

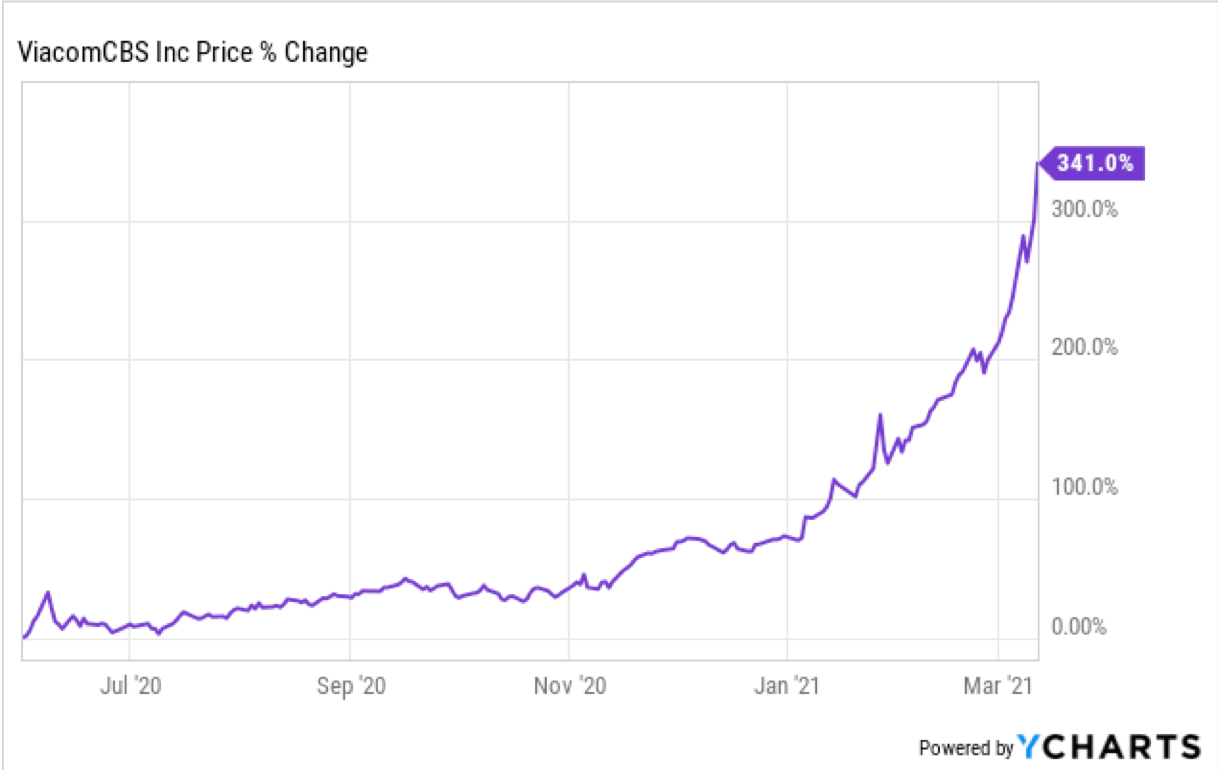

As a family office, Hwang was confined to managing his own still sizable fortune & stayed out of the limelight for many years, where his investments did well. By 2020 Archegos was managing $10 billion with concentrated stakes in mostly large US and Chinese companies. Towards the end of the year, the fund started focusing its bets on just a few stocks, buying massive positions in RLX Technology, Baidu, Discovery, Shopify and ViacomCBS, among others. Hwang’s purchases help explain why these stocks spiked considerably into 2021, with Viacom as the poster child:

How could a low-key family office move the price of these stocks so meaningfully without attracting attention? Derivatives, specifically total return swaps. Total return swaps are a way for hedge funds to get exposure to an equity’s price movement without owning the underlying asset, paying a bank to buy the asset for them & transfer the gains or losses back to the client. These swaps are normally traded off a regulated exchange & involve significant leverage.

Archegos went to as many banks as it could to paper separate swap deals with Nomura, Credit Suisse, Morgan Stanley, and Goldman Sachs, paying hefty fees in the process. At this point, while Archegos’s net exposure is still unknown, its gross exposure swelled to many times its $10 billion in capital, skewed towards betting their stocks would continue going up.

The Supernova Begins

During the week of March 26, Bill Hwang’s time as a successful family office manager would end in flames. With such a leveraged, concentrated portfolio, it only took a few unlucky headlines from the fund’s positions to spark a panic. On March 22, RLX Technology fell after China announced an e-cigarette crackdown. ViacomCBS began a $3 billion capital raise to fund investments in Paramount+. SEC pressure on Chinese listings in the US hurt shares of Baidu. As their positions turned against them, Archegos’s poorly constructed hedges failed to offset the losses, and banks came calling looking for extra collateral.

The only problem was, with the size & speed of losses suffered, Archegos had quickly run out of money. Faced with the grim reality of default, banks convened an emergency meeting to plan their next move, something they haven’t done since the 2008 financial crisis. Meetings like this highlight a classic prisoner’s dilemma situation - if all the banks work together to unwind Archegos’s positions, they could limit losses in total. But if a bank were to cut ranks and sell first, they would save themselves at the expense of everyone else. The emergency meeting ended with no truce in sight, and chaotic selling began the next day, on Friday, March 26.

What follows reads like a frenetic, climactic scene from the movie Margin Call, a fantastic drama set on the trading floor of a Wall Street bank.

8:00 AM EST: Goldman Sachs announces three block trades of $BIDU, $TME, and $VIPS for $3.7 billion in total.

9:00 AM: Block trades are upsized to $6.6 billion.

9:30 AM: US markets open.

10:06 AM: Goldman Sachs block trades hit, sending the three stocks down -10% each.

10:40 AM: Morgan Stanley announces four block trades of $DISCA, $DISCK, $FTCH, and $SHOP for $4.1 billion in total.

12:45 PM: Goldman Sachs announces a block trade of $VIAC for $1.75 billion.

1:00 PM: Morgan Stanley announces five block trades of $BIDU, $TME, $GSX, $VIPS and $IQ for $4.1 billion in total.

1:55 PM: Goldman Sachs announces three block trades of $IQ, $FTCH and $DISCA for $3.2 billion in total.

2:45 PM: Goldman Sachs announces a block trade of $GSX for $600 million.

4:00 PM: Markets close. $BIDU -9%, DISCA -30%, $VIAC -34%, $GSX -52%.

By the end of the day, nearly $20 billion in stocks had been sold from Archegos’s account, and his portfolio companies had been decimated. Here’s that same Viacom chart after Friday’s bloodbath:

By Monday, banks who didn’t get a head start in the fire sale began reporting big losses - mainly Credit Suisse and Nomura. CS in particular seems to have taken the brunt of the supernova’s blast, with their stock -20% in the past week amid rumors of more than $7 billion in losses, or two years of profit.

Implications

Following Archegos’s supernova, many were quick to give their take on the downstream impacts to US markets. Politicians are using the chaos to push for more regulatory control. Some are stressing that this blowup is nothing more than an isolated hedge fund collapse, while others are saying it’s a sign of more trouble ahead.

Here’s what I think are the most important takeaways:

Hedge funds are blowing up - in spectacular fashion - during a roaring bull market. The S&P 500 is near all time highs. Interest rates are low. Liquidity is quite easy to access. And still markets are revealing places where smart, successful investors have bitten off more than they can chew. First it was Melvin Capital, who got steamrolled by r/wallstreetbets when it used extreme leverage to bet against GameStop. Now it’s Archegos, who got steamrolled by a few unlucky headlines when it used extreme leverage to bet on Viacom & other stocks. If markets run into any sort of surprise turbulence like we saw with COVID in March 2020, I expect more funds to come out of the woodwork with empty pockets and egg on their faces. Even the best investors are becoming lulled to sleep by forever-ZIRP and stimulus every few months.

The system will likely not be threatened by isolated hedge fund supernovas. Post-GFC regulations are largely working as intended. Sure, a few banks lost a lot of money because they took on Archegos’s account and underestimated its risk. Some people may get fired. Shareholders will be displeased. But this supernova likely won’t become a black hole that sucks the entire financial system down with it like in 2008. Banks are better capitalized now & have less exposure to exotic financial products like total return swaps. Regulators can pat themselves on the back knowing that Archegos could have been a much bigger problem for banks & markets than it ended up being.

The need for better risk analytics could not be clearer. Even though Archegos didn’t jeopardize the global financial system, the supernova did vaporize billions in market value because banks like Credit Suisse extended them too much leverage. Did banks realize how much combined business they were doing with Bill Hwang? Did they know how easily losses could accelerate to the downside? How could their system allow for this kind of blowup & impact to their business? If anything, this saga shows how risk management technology has plenty of room for improvement. This is where market data companies like Moody’s, S&P Global, Refinitiv, Nasaq & ICE come into the picture. Their analytics products are designed to help banks handle risks like Archegos. I have more confidence in the addressable market for risk analytics products after hedge fund blowups like the one we saw last week.

Exchanges come out of this scot free. In general it’s good to assume that when banks take on too much risk & get burned, exchanges win. It happened in 2008 when banks were forced to de-leverage & let exchanges electronify dealer-owned markets, and it might happen again today. Since their inception, clearinghouses like those owned by ICE & CME have not experienced a default, and continue to serve as a viable solution for OTC markets gone wrong. If regulators do make changes to existing market structure as a result of the Archegos supernova, I suspect it will put even more power in the hands of exchanges & data providers who already control a large amount of market influence today.

Honorable Mentions

FactSet reported fiscal Q2 earnings on March 30, with revenue +5% organically and EPS +7% vs. Q2 2020. The stock fell after releasing results due to the curious case of 2021 guidance, which calls for full-year EPS growth of only ~1%. So far this year, FactSet has markedly outperformed their EPS guidance range yet refuses to raise their outlook, begging the question - why? Either FactSet management is being too conservative or the second half of 2021 will see a serious slowdown in growth. Consensus EPS estimates sit at ~$11.14 vs. management’s range of $10.75 - $11.15.

CBOE received SEC approval to launch periodic auctions for its US equities business, which it expects to begin sometime in Q3 2021. Periodic auctions help attract block trading to a lit exchange & helps CBOE compete with off-exchange block trading venues for market share. This complements the company’s recent acquisition of BIDS, the largest independent block trading ATS in the United States.

CME announced plans to launch micro Bitcoin futures on May 3, with each contract worth 1/10th of one Bitcoin (~$6,000 at current prices).

ICE launched its new oil exchange in Abu Dhabi on March 30 with over 6,000 contracts of its Murban crude product trading hands on day one. The launch comes as Brent struggles with shrinking supply & the potential for new global oil benchmarks grows stronger.

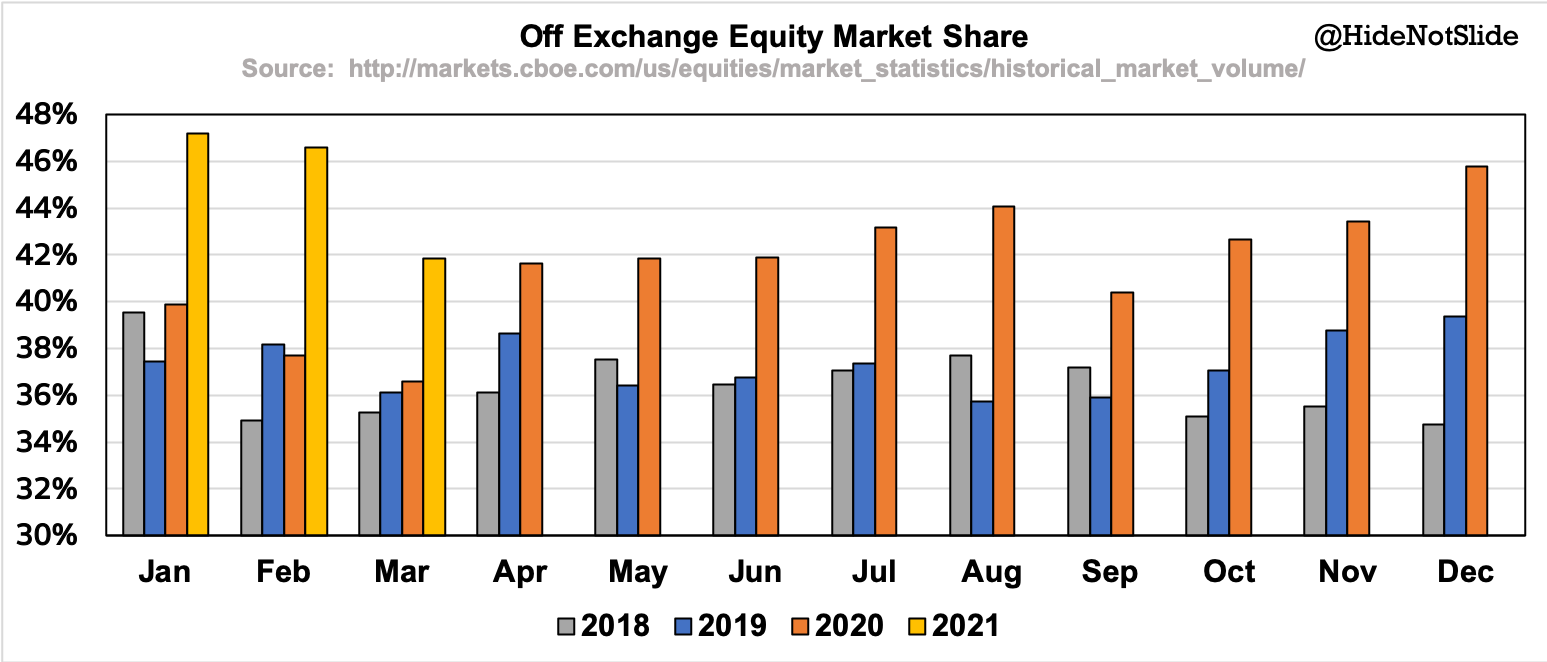

Chart of the Week

March marked a reprieve for the equity exchanges - off-exchange market share ticked down after spending multiple months near all-time highs. This move could be a sign that retail participation in the equity markets is starting to die down as COVID lockdowns subside and consumers choose to spend their new round of stimulus checks rather than trade stocks.

It’s worth noting however that March levels still track significantly above historical averages despite the recent pullback. Sure, retail trading has cooled off a bit, but only back to summer 2020 levels, which were mind-bogglingly record highs at the time.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Bitcoin & Ethereum.