What Jim Chanos Gets Wrong - And Right - About Coinbase

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

News

Jim Chanos Speaks with CNBC’s Scott Wapner on “Closing Bell: Overtime”: Famed short-seller Jim Chanos appeared on CNBC on March 18 to unveil a new short of his - Coinbase, the popular crypto exchange that’s followed most coins lower in 2022 with a YTD return of -30%. Chanos gave a bit of detail behind his short thesis during the interview - below is a transcript of his main comments:

“Coinbase is what we would call one of the bubble stocks. Obviously, it’s got a unique market niche as the, pretty much the only public crypto exchange and consequently has the valuation to go with it. So Coinbase is about a $40 billion market cap company. Stock was trading in the fall between $200 and $300, got down to about 150 recently, it’s bounced, I think it closed somewhere around 185 today. But Coinbase is again exactly what I’m referring to.

So, in the fall when the stock was trading between 200 and 300, the adjusted EPS estimate for this year was $7. It’s now, that same estimate, is now $3. So the multiple’s actually got up. On a GAAP basis because of course like many tech stocks, they add back share base comp, on a GAAP basis, the estimate for this year has gone from $6 in the fall to a loss. We basically think Coinbase is over earning.

If you do the numbers, their revenue base is roughly 3% to 4% of their custodian assets, their customer assets. They have a, over $200 billion of customer assets in their system. And if you look at comparable kinds of exchanges or trading operations, and Coinbase is an amalgam of a lot of these because it has different functions. You know, Charles Schwab has revenues of about 25 basis points of client assets. Trading operations, bank trading operations typically have revenues of 1% to 1.5% of assets. And there you have Coinbase at 3% to 4%. So we think that as competition increases in crypto and this is not a call on, on crypto or Bitcoin prices or anything like that, but we think as as competition increases amongst the exchanges, you’re going to see fee compression, and as it is Coinbase will probably not be profitable this year with a $40 billion market cap.”

Chanos made a number of interesting assertions in this interview - some I agree with, and some I do not. Let’s go through them piece by piece:

First, Chanos cites Coinbase EPS estimates that have dropped substantially, from $7 to $3, as a reason to still find Coinbase overvalued despite its steep price drop in recent weeks. These EPS estimates, by the nature of Coinbase’s business, have to include a volume forecast. Earnings = revenue - expenses and taxes. Revenue = mostly trading fees (at least 90%). Trading fees = volume. If you can guess what Coinbase’s trading volumes will be this year, you’ll likely get pretty close to an accurate EPS estimate & valuation for the company.

The problem is, no one can accurately predict trading volumes in the exchange industry, especially in a nascent & volatile asset class like crypto. In 2021, for example, Coinbase EPS estimates were quite low to start the year until crypto prices & volumes ballooned higher in late Q2 - as volumes shot up, so too did EPS estimates and the stock price. Now that volumes have stagnated as crypto prices retrace, estimates have returned to a relatively low level. I find this metric a rather weak foundation for a short thesis given its inherent unpredictability over short & medium time frames.

Second, Chanos makes the claim that Coinbase is “over-earning” when comparing fee revenue to custodial assets. On a longer-term time horizon (5+ years), I agree with him. Given Coinbase’s primary customer is retail, and traditional markets like equities, options & even futures charge little to no fees for retail trades, I believe Coinbase is due for significant fee compression as crypto markets mature & competition intensifies.

On a shorter-term horizon, I don’t think the fee compression thesis is worth the risk of shorting the stock. Crypto exchanges are spending enormous amounts on marketing to keep retail traders engaged on their platforms & willing to pay high fees for access to their markets - Coinbase spent ~$660 million on sales & marketing in 2021 alone, and guided for 2022 to be even higher. I believe this amount of marketing expense will keep retail fees abnormally high for the immediate future - from Chanos’s perspective, retail fees can certainly stay high longer than his short can stay solvent.

In summary, I agree with Chanos’s broader argument that Coinbase’s prosperous retail fee revenue won’t stick around forever, but I don’t think the company is a good short at this point in 2022. If crypto prices start to move higher & serious retail focus returns to the space, Coinbase can still capitalize on the hype to mint many billions of dollars in trading fees & cash flow, and the odds of that happening at any moment are still substantial. Chanos didn’t confirm if his trade was hedged with any kind of long crypto exposure, which is how I would play a Coinbase short if I were in his position. In my view a naked short of Coinbase is too risky at this point in the company’s life.

US activist urges TP ICAP to sell: One of the last bastions of the analog trading age is having a rough start to 2022. TP ICAP is a large energy & fixed income broker business that’s struggled to manage the global shift to electronic trading & extreme volatility in the post-COVID era. The firm’s stock has fallen -70% since 2018 amid shrinking margins & diversification efforts that haven’t impressed investors.

On March 23 TP ICAP received a letter from one of its largest shareholders, hedge fund Phase 2 Partners, urging the company to pursue strategic alternatives amid what they deem as radical underperformance & managerial incompetence. Phase 2 CEO Justin Hughes has experience with activist deals in the exchange space - his previous fund, Philadelphia Financial, made a large investment in ITG and picked up a board seat before the firm’s sale to Virtu in 2019. It seems TCAP is Hughes’s next target.

How does Hughes suggest TP ICAP unlock value? By pursuing a sale to either a financial or strategic buyer. These include exchanges like ICE, Deutsche Boerse or TMX with European energy & equity adjacencies, market makers & banks with European brokerage operations, or private equity. Whoever takes the firm over will be tasked with returning TP ICAP’s margins to their former glory, diversifying revenue streams away from its volume-dependent broking businesses, and managing a largely analog, human-based trading model in the face of automation across the industry.

Front Month now has over 20 premium articles in the archive on topics including Citadel Securities, FTX, European energy markets, NFTs and much more. If you like the free research I publish in this newsletter each week, I invite you to check out these premium articles & a growing library of high quality market structure research.

Thank you for your support!

Other Stories I’m Reading

Market Lens: Why Do Most Markets Trade Continuously Rather Than In Auctions?

Yuga Labs pitch deck on the financials & future plans for the Bored Ape Yacht Club

Trafigura’s finance chief warns of commodity industry stress

Robinhood’s new debit card will automatically invest in stocks and crypto as you spend

FactSet Reports Results For Second Quarter 2022

Chart Of The Week

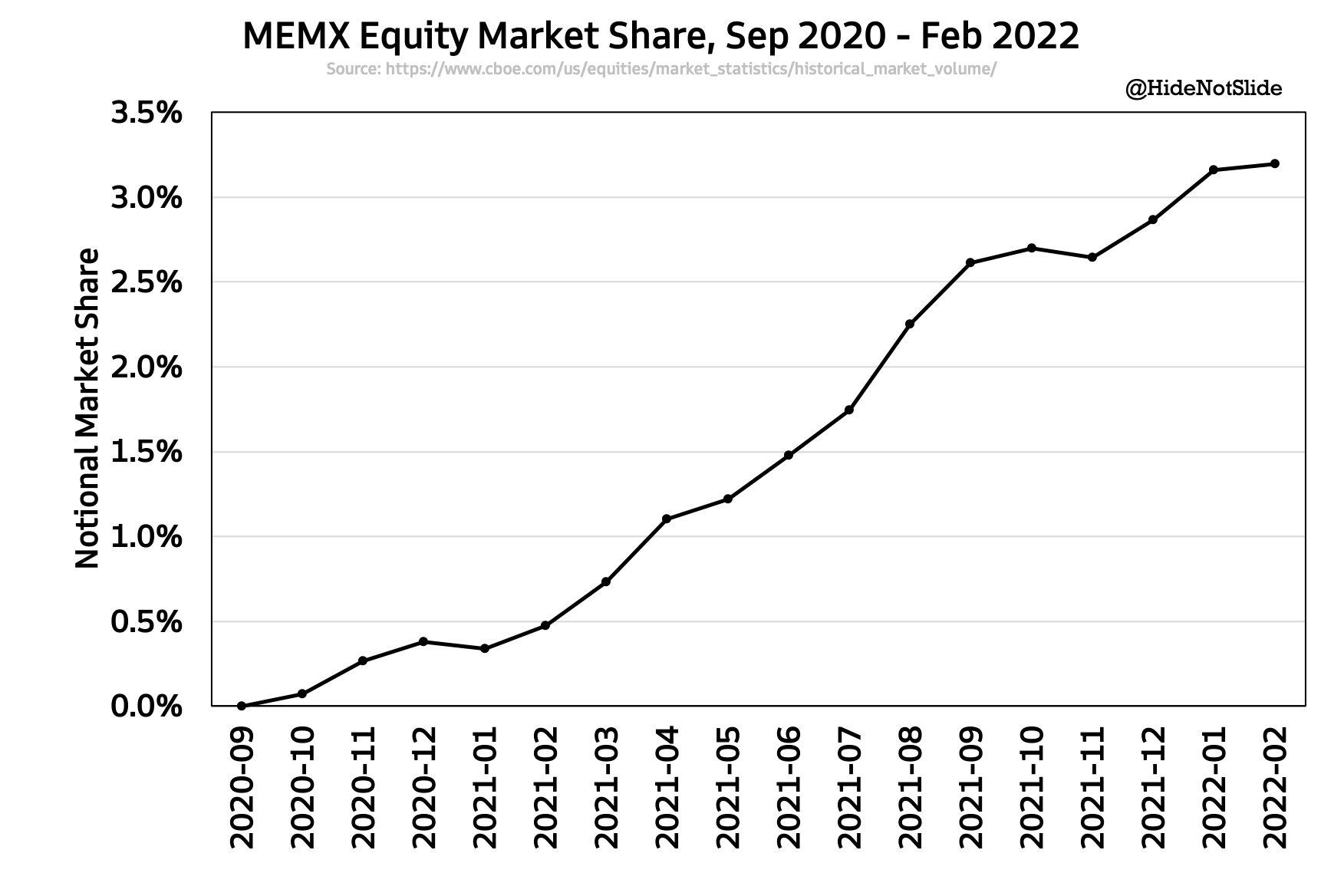

When the Member’s Exchange announced its plans to launch a stock exchange in 2019, not everyone accepted the news well. Legacy exchanges like Nasdaq, CBOE and the NYSE saw their top customers, including Citadel Securities, Virtu, Charles Schwab and others, seek to upend their hold on US equities trading through their ownership in MEMX. Industry spectators saw another catalyst for market fragmentation, where a small exchange challenger siphons off a few points of market share & pushes up connectivity & trading costs in the process. Since MEMX’s launch in September 2020, this more or less has happened - the exchange has won just over 3% of notional US equities volume after ~18 months in operation:

This week the exchange announced plans for its next chapter of growth - launching an options exchange to challenge the same legacy competitors in a new market. These competitors shouldn’t take the news lightly - options are a wholesaler-dominated market, and Citadel Securities - the top options wholesaler in the US - is an investor in MEMX. I think there’s a good chance we see MEMX’s options market share outpace equities after launch as its top owners leverage their market power to give the exchange it owns an advantage. MEMX says it’s targeting a Q4 2022 launch pending SEC approval.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, SPGI, NDAQ and VIRT. I am also long BTC, ETH, LOOKS and SOL.