Welcome To The Big Leagues, Trumid

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

The 2008 financial crisis sowed the seeds of radical changes in corporate bond trading.

Before the global meltdown, banks unequivocally dominated the market. Acting as primary dealers, they held large inventories of bonds on their balance sheets and built deep relationships with the largest firms on Wall Street. The banks maintained a tight grip on the market by keeping trading data close to the chest - only they could see the full view of a bond’s supply & demand. Traders wishing to move bonds in size had nowhere else to go.

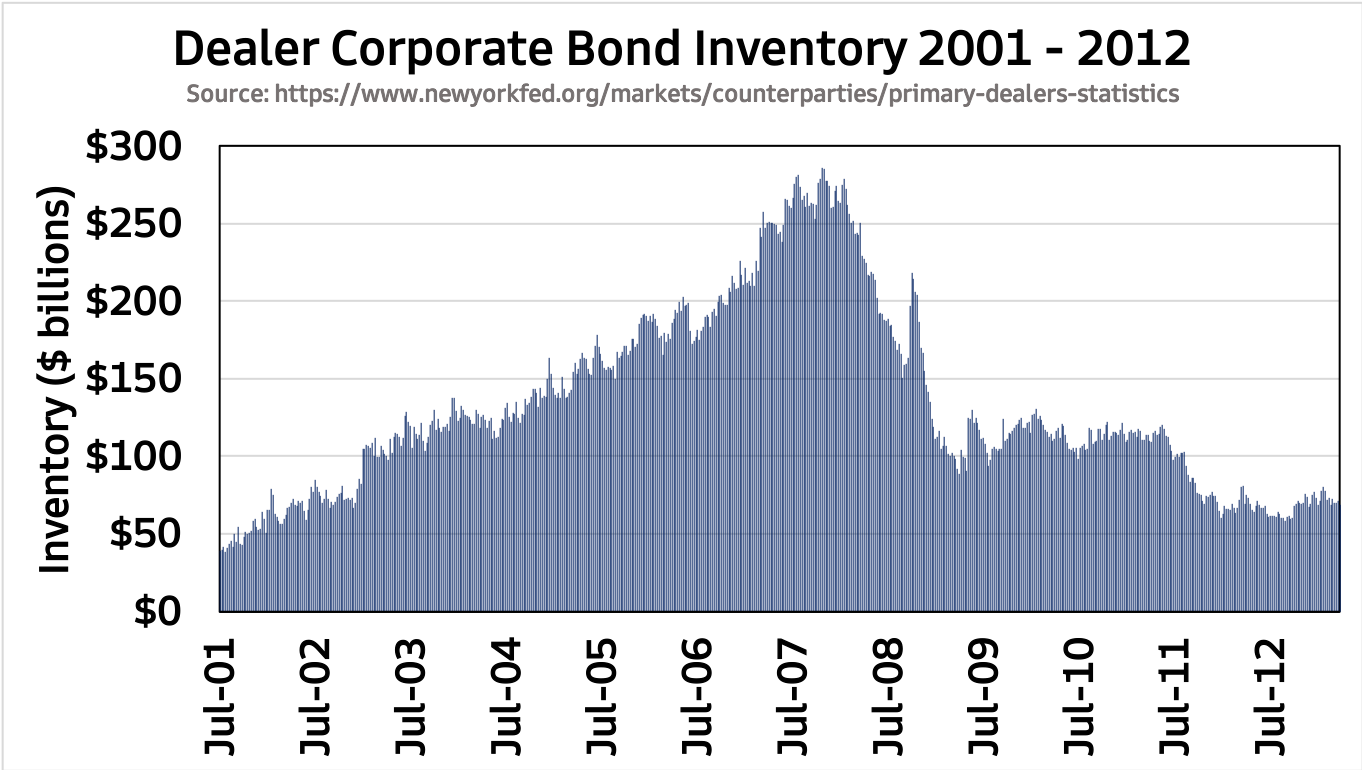

When wrongdoing at these same banks nearly imploded the financial system, regulatory pressure forced them to give up market power. Tighter capital requirements led to corporate bond dealer inventory dropping from ~$280 billion at the end of 2007 to ~$75 billion by the end of 2012:

As market tectonic plates began to shift, corporate bonds became a less liquid asset - at least at first. Scores of startup trading platforms emerged to fill the gap left by the dealers, and as the field became more crowded, liquidity quickly fragmented. New entrants into the corporate bond race made it harder for any one company to succeed as trades were spread over a wider array of platforms.

One such entrant was Trumid, launched in early 2015. A few key advantages made Trumid a stand-out competitor from the beginning. First, Trumid’s management team were industry veterans and had close ties to the legacy dealers - CEO Ronnie Mateo was an MD at Citigroup, and President Mike Sobel & Head of Product Jason Quinn held leadership roles at Lehman Brothers. Longstanding relationships with many big banks and buyside firms helped boost the pitch to come try out electronic trading with their technology.

Second, Trumid had a deep bench of influential, high profile investors, giving the firm a substantial boost to credibility & media coverage above competitors. Paypal co-founder Peter Thiel and legendary investor George Soros led an early $25 million funding round in the company, valuing Trumid at ~$100 million in 2015. Shumway Capital, a Connecticut fund with over $9 billion in AUM, also participated in the raise as well as Trumid’s first external funding round earlier that year.

Third, Trumid chose a unique market structure to attract liquidity - trading sessions called “swarms”. Instead of trying to build an active market for all bonds at all times of the day, Trumid set up short, eight minute trading windows for specific sets of bonds where participants could log on and be active at the same time. If a big fund manager needed to offload a large amount of Apple 2022 bonds, for example, their best chance to get a fill would be to show up at Trumid’s Apple swarm and find a buyer. This technique helped solve the problem of different buyers & sellers looking for liquidity at different times of the day & missing each other - the “ships passing in the night” problem according to Trumid.

This manager-investor-tech combo gave Trumid a strong starting foothold, but gaining meaningful market share proved difficult. Over a year after launch, trading volumes stood at ~$45 million per day, a paltry figure compared to industry volumes of $30+ billion. More needed to be done before Trumid could build the momentum needed to survive.

The problem with corporate bond liquidity is the massive amount of unique bonds outstanding at any point in time, each with their own supply & demand dynamics. While a company has only one market for its stock, it may have five separate bond issuances outstanding, all with different yields, maturity dates & markets. Traders need to be able to properly value these illiquid bonds, pass trades through their compliance checks, and find someone to take the other side of their trade, all fast enough to take advantage of market movements. Now on top of this, they needed to shift their schedule to be active during Trumid’s pre-set swarm for their interested bond. The logistics became too daunting to manage.

In response, Trumid adapted with two important updates. First they improved their bond pricing data, helping traders value bonds & spot potential trades. More importantly, Trumid launched a second iteration of their swarm function, this time letting users trigger their own swarms. If enough buyers and sellers broadcasted interest in trading, a swarm would form and trades could take place. This improvement helped traders find liquidity on their terms, which tipped the scales enough in Trumid’s favor to attract more market share. By 2018, Trumid’s platform traded ~1% of the total corporate bond market.

As performance improved, Trumid was able to leverage its newfound momentum to win over more strategic investors. Deutsche Borse annouced an investment in Trumid in 2017, followed by Singapore Exchange in 2018 - both global multi-asset exchanges with fixed income expertise. Partnerships with Wall Street heavyweights followed - Citigroup, Barclays, Goldman Sachs and even Nasdaq all began working with Trumid & giving input to the growth of its markets.

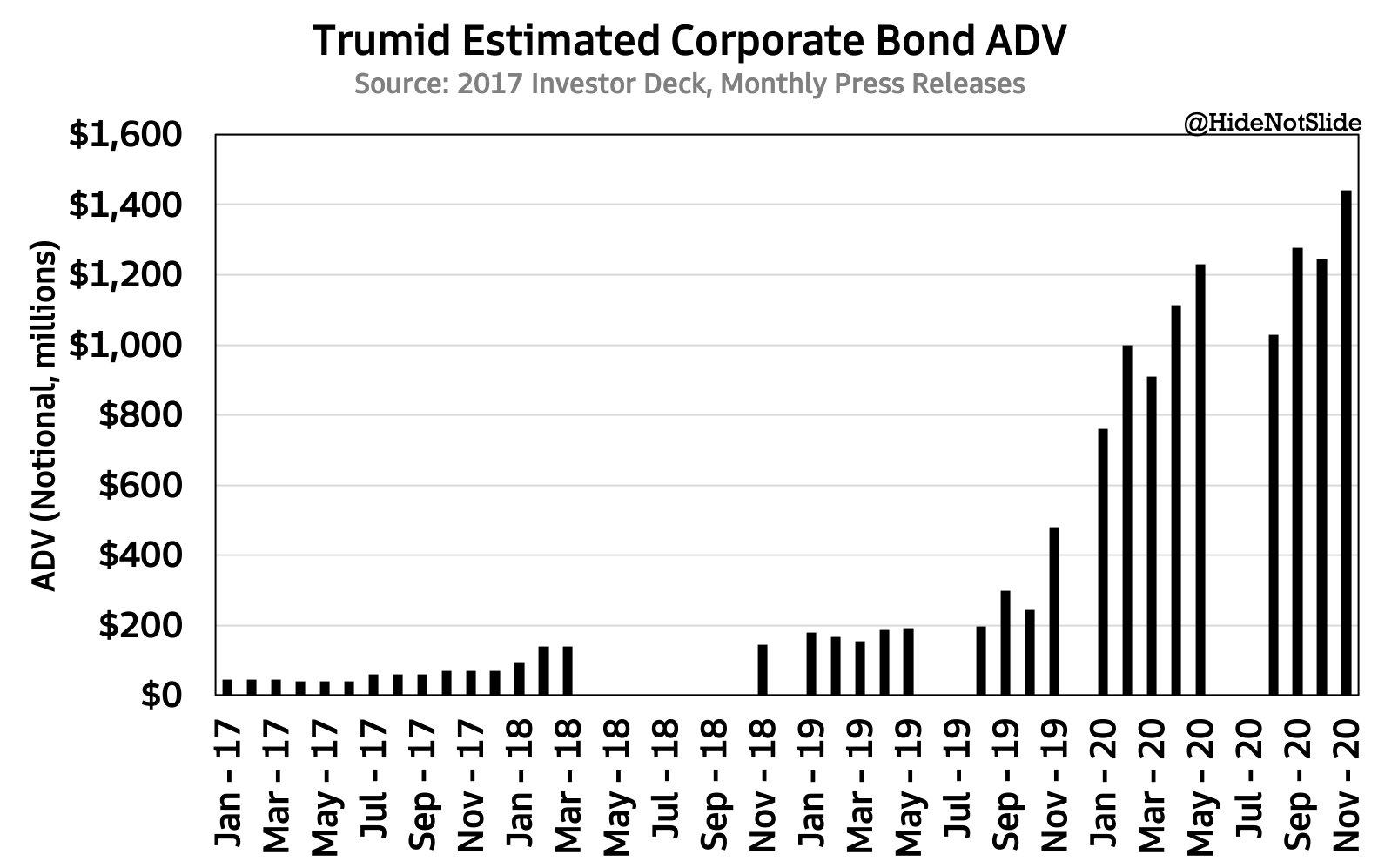

It took five years of methodical market tinkering, but Trumid entered 2020 ready for the big leagues. Even before COVID trading volumes were hitting records, with January growing at a +300% clip YoY. The ensuing pandemic chaos only accelerated volume growth; by November 2020 Trumid’s average daily volumes hit an astonishing $1.4 billion per day, 32x higher than early 2017:

(*Trumid’s volume releases are inconsistent hence the various gaps in the above graph)

To put Trumid’s year into perspective, volumes are now 1/4th the size of Tradeweb’s corporate bond business and 1/7th that of top player MarketAxess. While Trumid may still be considered a mid-level exchange, the explosive growth for a company only five years old is what’s worth noting here. In January 2021 Trumid finished another funding round, pushing its valuation well past the $1 billion mark. That’s more than a 10x return for Thiel and Soros five years removed from their initial investment - not too shabby.

2021 is looking to be another exciting year for Trumid. Historic levels of corporate debt outstanding combined with more work-from-home trading has pushed adoption of electronic trading to new highs. New exchange & bank partnerships are still in their early stages. Who knows, we could even see the start of an IPO process forming before the year’s up. Whether Trumid becomes a public company this year or down the road, exchange investors and competitors need to keep an eye on this young challenger that’s quickly catching up.

IHS Markit Earnings

Links:

Results:

($ in millions. Source: IHS Markit Investor Relations)

($ in millions. Source: IHS Markit Investor Relations)

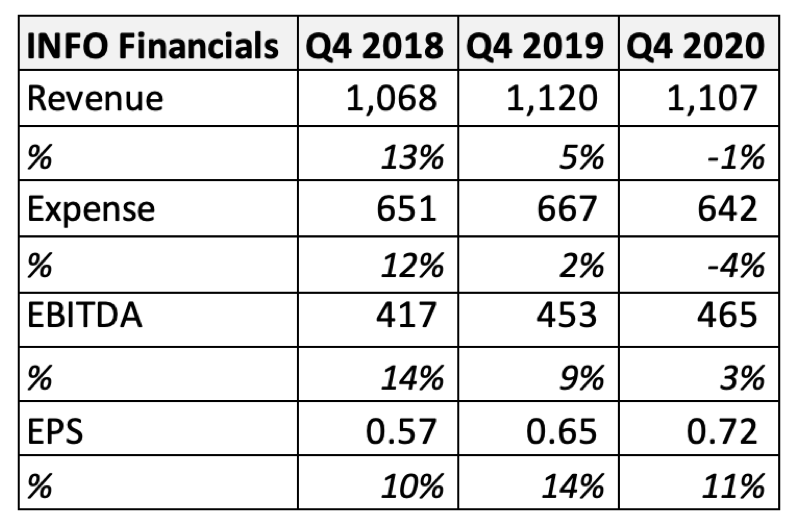

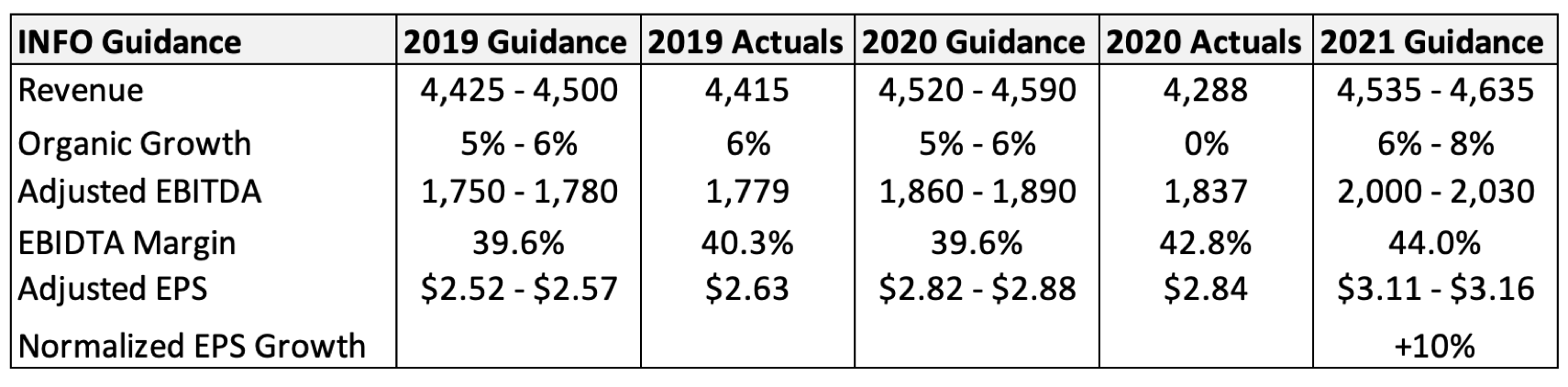

IHS Markit came into Q4 2020 earnings on the tail end of an eventful if rather bi-polar year for the company.

Their Financial Services segment did quite well in 2020. Ballooning corporate debt issuance and greater adoption of electronic trading boosted demand for IHS’s bond pricing services. ESG investing (now all the rage in case you haven’t heard) helped grow their indices business. We even saw strength from Ipreo, particularly in alternative market data sales & loan processing. Financial Services has been growing revenue at a 5-7% clip since 2017, and 2020 saw more of the same on this front. 2021 is projected to be an even better year with a 6-8% growth target.

IHS’s non-finance segments were where 2020 turned ugly. The company’s Transportation segment struggled heavily this year in-line with the automotive industry, as recurring revenue was hurt by price concessions & one-time fees were hurt by the cancelling of all in-person sales events. Resources looked just as concerning - upstream energy companies cut back significantly on CAPEX amid low commodity prices, dimming demand for IHS’s consulting services. Q4’s results, while showing some sequential improvement, saw this narrative largely continue.

This was also the first earnings call since IHS Markit announced its pending merger with S&P Global, a $40 billion mega deal that combines two top players in data & indices. I consider this earnings release “S&P Global Earnings Part 1” given SPGI shareholders will soon be impacted by IHS results.

During the earnings call management called for broad-based recovery in 2021. IHS’s energy & auto assets should run into better comps starting in Q2, and vaccine roll-outs should help IHS customer demand return. CEO Lance Uggla went so far as to call 2021 a “normal year” for IHS Markit. EPS grew 11% this quarter and FY guidance is for ~10% growth next year, in line with expectations for the company post-S&P merger.

I view IHS’s Q4 earnings as a general confirmation of the company’s health before they’re swallowed up by S&P. The financial assets prove attractive and should marry well with Cap IQ and Dow Jones Indices. Even the energy assets of both companies look to have a better future together post-merger. IHS’s Transportation business is the only piece I’m less excited about, given its cyclical customer base & lack of meaningful synergies with S&P. Investors are in wait-and-see mode for deal closure & resulting decisions, and I find myself in a similar camp.

Honorable Mentions

It’s been a busy week for IHS Markit - in addition to reporting Q4 earnings, the company announced a 50/50 joint venture with CME to combine their post-trade businesses. CME will commit assets it bought with NEX - Traiana, TriOptima and Reset; IHS will commit MarkitSERV and $113 million in cash. The news comes over two years after IHS scrapped plans to sell its MarkitSERV business outright with no interested buyers appearing. The deal combines two of the top competitors in trade processing & reporting for OTC interest rate swaps & FX.

BlackRock reported earnings on the morning of January 14, beating analyst expectations with revenue +13% and EPS +22% YoY. Broad equity market gains combined with net inflows into its ETFs drove AUM to a record $8.7 trillion.

CME, Nasdaq, CBOE and ICE all paused political donations after the violent US Capitol riots on January 6. ICE’s reactions in particular are worth noting given ties to Kelly Loeffler, a pro-Trump senator from Georgia who lost her seat in a January runoff election along with David Perdue.

Chart of the Week

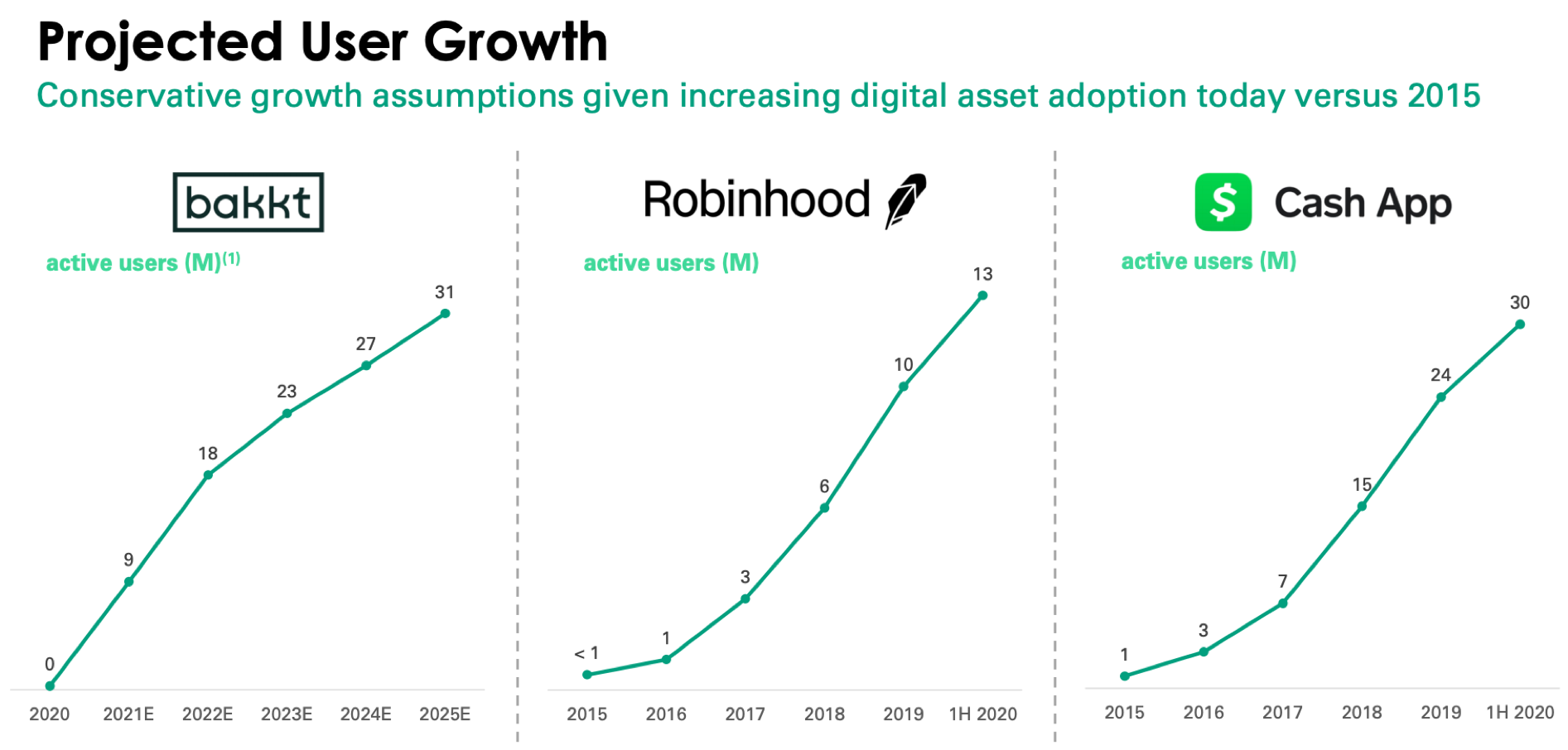

Last week’s rumors were confirmed - Bakkt, ICE’s crypto unit, announced intentions to go public via a SPAC in Q2 2021. In connection with the announcement, Bakkt released a detailed investor deck walking through their projections & strategy as a public company. You can find this deck here.

Today, Bakkt comprises a Bitcoin futures & options market integrated with ICE’s trading infrastructure, digital asset custody, and a soon to be launched retail payments & trading app. Post-merger Bakkt will have $574 million of cash to invest in growing its app & launching new digital asset products, competing with the likes of Robinhood, Coinbase, and Square.

Bakkt has set aggressive targets over the next four years to grow into its lofty $2.1 billion valuation. The company projects more than 30 million app users, $500+ million in revenue & $280+ million in EBITDA by 2025. For context, Square’s Cash App has ~30 million monthly users as of Q3 2020. Bakkt will need to show it can meaningfully execute on these targets for its valuation to not fall into “just another crypto SPAC bubble” territory.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, CBOE, NDAQ and VIRT.