[UNLOCKED] OMX: The Deal That Defined Nasdaq

[UNLOCKED] OMX: The Deal That Defined Nasdaq

Why Nasdaq's purchase of OMX matters more than you think

This week I chose to unlock a paid post published back in July about Nasdaq’s blockbuster purchase of OMX in 2007. If you enjoy this post please consider subscribing to Front Month Premium, the paid portion of this newsletter where I dive into market structure topics like this. Thank you for your support!

2007 may be considered the most active year for exchange M&A in the industry’s history.

There’s of course the flashy, contentious bidding war between ICE & CME for the Chicago Board of Trade, ending in July 2007 with CME as the victor. There are the smaller deals inked during & after this bidding war ended - ICE bought ChemConnect, Chatham Energy Partners, Winnipeg Commodity Exchange, and the New York Board of Trade all around this time. the NYSE merged with Euronext in April 2007, closely followed by the $3 billion Deutsche Borse acquisition of ISE. The London Stock Exchange merged with Borsa Italiana in October 2007 after fending off multiple takeover attempts throughout the year. The pace of deals was dizzying, even overwhelming at times.

Amidst the M&A chaos that year, I believe a particular set of exchange transactions gets overlooked - those of Nasdaq, the US equities platform vying for diversification & global influence. Nasdaq was on an M&A spree of its own entering 2007, with the $2 billion purchase of Instinet in 2005 and a ~30% stake in LSE in 2006 after full takeover attempts failed. Nasdaq’s spending spree continued in ‘07 with the purchases of Directors Desk & the Philadelphia Stock Exchange.

I don’t want to talk about any of these deals today, though they’re all interesting in their own right. I want to talk about Nasdaq’s largest & most important deal of the year, and likely the decade, that began on May 25, 2007:

The $3.7 billion transaction was set to turn Nasdaq from a regional competitor among a crowded US exchange field into a global powerhouse, more than doubling its size in the process.

Getting this deal over the finish line would prove to be much more difficult than Nasdaq could have expected.

Setting the Stage

What did Nasdaq see in OMX? The European exchange operator was comprised of three distinct business units, each with their own valuable assets:

(Source)

Nordic Marketplaces (~48% of revenue): OMX owned a portfolio of regional stock & derivatives exchanges in Europe, including Stockholm, Copenhagen, Helinski, and Iceland. Most of the revenue from these exchanges came from cash equities transaction fees as trading activity among regionally listed securities ebbed & flowed. OMX also listed various equity index contracts on Eurex & LSE, tracking benchmarks of the top 25 or 30 companies in each region.

Information Services (~17% of revenue): Nearly every exchange transaction business with meaningful volume generates a treasure-trove of market data from its activity. Think of it like an exchange’s exhaust - after the trading day is finished & transaction fees have been collected, the exchange is left with a massive record of that day’s trades & orders, which banks & other institutions are eager - sometimes required by law - to buy. OMX also housed their stakes in various international clearinghouses in this segment.

Market Technology (~35% of revenue): Here’s where OMX’s assets really shine, and where I believe Nasdaq saw opportunity in M&A. OMX operated a significant exchange infrastructure business that built & maintained trading platforms & back-end systems for exchanges around the world, including the major stock exchanges of Australia, Singapore, and eastern Europe. Exchange groups looking to outsource costly & time-consuming technology projects would sign long-term contracts with OMX to manage these projects for them. OMX’s key products included trading systems CLICK-XT, SAXESS and CONDICO, each with their own unique set of interested clients. To help visualize, below is a simple mock-up of where CLICK-XT fits into an exchange’s lifecycle:

(Source)

On May 25, 2007 Nasdaq launched their bid for OMX offering a mixture of cash & stock valuing the company at $3.7 billion, a +19% premium to OMX’s previous closing price. Nasdaq’s then CEO Robert Greifeld put the bid’s rationale simply:

“The future of exchanges is about technology, flexibility and scale. NASDAQ and OMX together deliver all of these benefits.”

The deal had to be approved by both sets of shareholders & regulators, but both seemed likely to pass with little headache. Nasdaq’s long hunt for a transformative acquisition and influence outside of North America now seemed only a matter of signatures & a few months time.

That is, until an exchange on the other side of the world spoiled Nasdaq’s party.

Old Colleagues, New Companies, Same Old Song & Dance

Nearly three months after Nasdaq’s initial bid was announced, a new bid emerged for OMX - Borse Dubai, the national stock & derivatives exchange of the UAE, made a $4 billion all-cash offer for the exchange, trumping Nasdaq’s price by nearly 10%.

This bid may seem like an out-of-the-blue intrusion from an unrelated company, but closer inspection helps add context. Borse Dubai’s then CEO Per Larsson had spent 18 years at OMX before his transition, including eight years as its chief executive. Under Larsson’s leadership OMX had mounted a hostile takeover bid for LSE in 2000, which had sputtered out & failed before the year was over. Larsson not only understood OMX’s business better than most, he had experience with and an appetite for large exchange deals. Making a bid for his former company seemed like the perfect opportunity to leverage his expertise for Borse Dubai’s benefit.

Nasdaq now found itself in a difficult position. Borse Dubai’s offer was legitimate & its CEO knew OMX’s value just as well as Nasdaq did. Borse Dubai’s owner - the UAE government - had deep pockets & global ambitions. How could Nasdaq get its deal done without overpaying?

I have no idea what kind of back-door meetings happened between Nasdaq, OMX and Borse Dubai during the tense negotiation period from August to September 2007. I have no idea what words were exchanged or what potential deals were proposed that never saw the light of day. I’d love to imagine it looking something like a scene from Mad Men, one of my favorite TV shows of all time. on some level I think many of us imagine something like this when we hear about fast-paced, billion dollar transactions like the one Nasdaq found itself fighting to complete:

After a long month of competing OMX bids on the table, Nasdaq and Borse Dubai finally came to an agreement that saw Nasdaq win the bidding war, but at substantial non-cash cost. Borse Dubai ended up purchasing OMX for $4 billion as planned, then effectively traded it to Nasdaq for three major assets:

Nasdaq’s 30% stake in LSE, valued at ~$1.7 billion.

A 20% stake in Nasdaq itself, valued at ~$1 billion.

A partnership with Nasdaq in its Dubai futures exchange, allowing Dubai to use Nasdaq’s name for commercial purposes & new products.

This may seem like a losing deal for Borse Dubai (trading a $4 billion asset for ~$3 billion of value), but the exchange saw more long term opportunity from large stakes in two emerging companies than a lump-sum pile of cash. Dubai could now participate in the upside of Nasdaq’s OMX integration, Nasdaq’s other investments, and LSE’s future growth.

Nasdaq officially closed on its OMX deal in February 2008, a full nine months after its initial announcement and in a completely different fashion than it once thought. Its assets, shareholder base & global presence had radically changed, but its cross-border mega-deal was finally over.

Aftermath

More than a decade later OMX is still a critical part of Nasdaq’s DNA. Nasdaq has aggressively pivoted away from transaction businesses to subscription market data products, many of which began with OMX. Remember OMX’s Market Technology segment? It’s now a key pillar of Nasdaq’s strategy & value proposition to investors - signing long-term contracts with exchanges around the globe to build & maintain trading systems & back-end infrastructure. Without OMX’s client base & experience in this area, Nasdaq’s offering wouldn’t be anywhere near as robust.

Even Nasdaq’s shareholder base is still impacted by OMX. Nasdaq’s top shareholder is still Borse Dubai with an 18% ownership stake as of Q1 2021 valued at ~$5.2 billion. Not bad for a $1 billion cost basis. Nasdaq’s second largest shareholder - Investor AB - was a large holder of OMX when the merger closed and owned a substantial portion of the combined company. After additional stakes were purchased over the years, Investor AB now holds ~12% of Nasdaq. That makes nearly one-third of Nasdaq’s ownership under the control of two OMX-related shareholders.

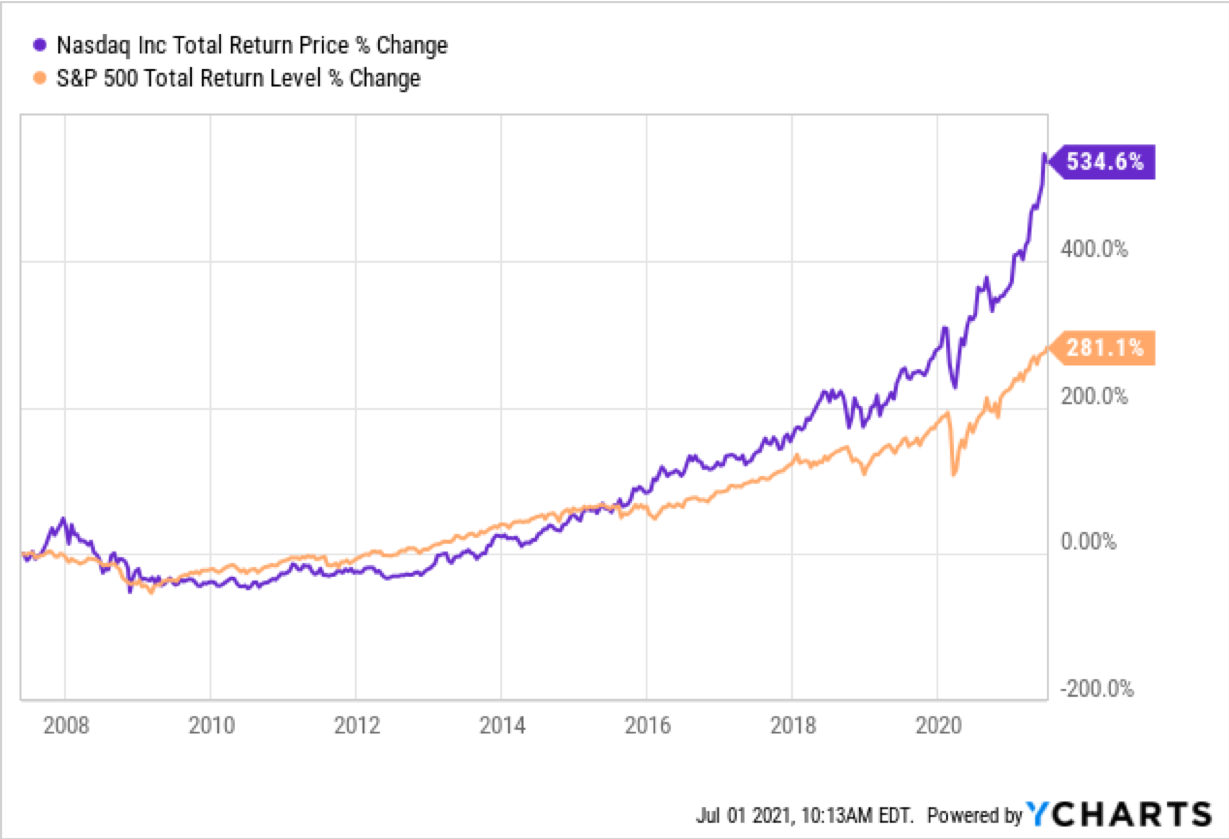

The impact of the OMX deal on past and present dynamics in Nasdaq’s stock cannot be overstated. Nasdaq made a bold set of compromises to secure OMX and radically changed its business & shareholder base in the process. The bet has paid off in spades - Nasdaq has crushed the S&P 500 since the OMX deal as investors applaud their shift to recurring market data revenue & a global portfolio.

Transformative M&A is a risky business with a low chance of success. Nasdaq’s deal of the decade seems to have decisively bucked the trend:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, COIN and VIRT. I am also long Solana.