Tradeweb Q4 2020 Earnings Review

Tradeweb Q4 2020 Earnings Review

This piece is part of a series on exchange & market data industry earnings - please SUBSCRIBE below for more earnings reviews & weekly writeups on the top stories in exchanges:

Links

Results

(Source: Tradeweb Investor Relations)

When digging through Tradeweb’s Q4 earnings & forming a 2021 outlook for the company, it’s important to remember - Tradeweb was made by banks, for banks. Many large dealers still own sizable stakes in the exchange today. Tradeweb’s core products help banks & their customers trade fixed income faster, cheaper & with less manual work. Tradeweb’s success is dependent on creating new technology that helps banks & the buy-side trade, and then convincing them to change their current way of business and adopt their new service.

To me, Q4 2020 earnings sent a clear message - Tradeweb’s efforts are working. Despite a low interest rate environment, Tradeweb’s US Treasury volume grew +19% YoY in Q4. Total revenue grew +18%, margins expanded +230 bps, and earnings grew an impressive +31%. The drivers of this growth came from Tradeweb’s two largest product groups - Rates and Credit, both of which are directly tied to new technologies that customers are changing their trading processes to use.

Rates

Tradeweb’s Rates business accounts for more than half of total revenue, and consists of three product pillars - Treasuries, mortgages, and swaps, each with its own set of innovations that are growing market share.

In Treasuries, management highlighted streams as a driver of market share growth in Q4. With streams, a Treasury market maker sends traders a continuous feed of prices & sizes they’re willing to execute against. This feed is tailored to each specific customer & allows them to see the market without risking “information leakage” by submitting trade requests and broadcasting their intentions. When streams are aggregated across multiple market makers & combined with Tradeweb’s other trading options, it gives customers a wide view of the market & more opportunities to find a trade they want to take. Tradeweb reported streaming volumes have more than doubled annually between 2018 and 2020, particularly among institutional customers.

In the spirit of giving clients as many options to trade as possible, Tradeweb made another interesting move by buying Nasdaq’s fixed income platform (formerly known as eSpeed) shortly before announcing earnings. There are plenty of reasons to like this purchase - it gives Tradeweb new customers to integrate into its Treasury network, gives it new technology (a full central-limit order book for US Treasuries) and adds another way for existing traders to find liquidity. Tradeweb CEO Lee Olesky is very familiar with eSpeed’s business - in the late 1990s, Olesky launched BrokerTec to challenge eSpeed when they dominated the Treasury market as a part of Cantor Fitzgerald. Ironically, Olesky now owns eSpeed as an underdog to take on today’s dominant Treasury platform, BrokerTec (now owned by CME). Best of all, Tradeweb’s acquisition of eSpeed is cheap - it cost only $170 million which could be easily covered by cash on hand. I’m very excited to see how eSpeed changes the trajectory of Tradeweb’s largest business in the coming years.

Mortgages are quickly becoming an equally important part of Tradeweb’s Rates business, with a new feature attracting volume to its market - spec pool trading. Mortgage-backed securities can be split into two general categories - to be announced (TBA) issues and specified pools, with the difference being visibility into the underlying mortgages. Buyers of TBA mortgages don’t know much about the underlying mortgages until delivery. Specified pools, on the other hand, are mortgages that are grouped by their underlying characteristics (like credit score, geography, etc…). The TBA market is highly electronic today, but spec pools are only ~5% electronic and represent Tradeweb’s next logical growth path. Electronic spec pool trading nearly doubled YoY in 2020.

Credit

Credit has been the shining star of Tradeweb’s growth for a few quarters now, and Q4 2020 was no different.

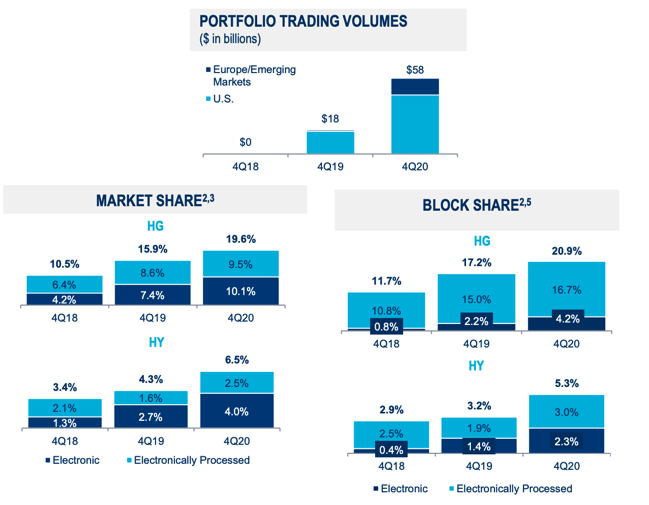

Corporate bond trading grew substantially industry-wide in 2020 driven by record debt issuance & growth in fixed income ETF trading driving activity in their underlying bonds. Tradeweb is benefitting not only from these macro tailwinds, but from a share perspective as well. At the end of 2020 Tradeweb controlled nearly 20% of the investment grade corporate bond market & 7% of the high yield market. Impressive share growth has been driven by yet another new technology - portfolio trading. As fixed income ETFs grow in popularity and size, market makers in these ETFs need a way to trade the underlying basket of bonds at a low cost using automated processes. Tradeweb has been able to give the market makers what they’re looking for, allowing for seamless transition to an electronic world as ETF demand soars. Portfolio trading is also a way to break into block trading of corporate bonds, the part of the market with the most volume & the tightest grip by legacy dealers. Credit is only 25% of Tradeweb’s revenue today, but it’s been the largest driver of overall revenue growth and is expected to make up an even greater part of the business as ETF trading keeps roaring higher.

Tradeweb’s Q4 earnings have caused me to re-think my position on the stock. I don’t own the company today (as of 2/6/2021), but recent developments may cause me to start an initial position soon.

Tradeweb’s purchase of eSpeed is a great addition to the business at a reasonable price that could accelerate Treasury growth in the medium term. Mortgages are another key pillar of the business that have a clear growth path ahead through spec pool trading. The demand for both global debt & ETF trading is only expected to grow in the coming years, boosting Tradeweb’s already successful Credit products. The only thing keeping me from owning the stock today is valuation (it trades at ~40x 2021 earnings), but I may stomach the premium to own a high-quality business with multiple ways to keep impressing the market.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this post, I am long ICE, CME, CBOE, NDAQ and VIRT. I am also long Bitcoin.