The Earnings Are Coming! The Earnings Are Coming!

The Earnings Are Coming! The Earnings Are Coming!

Plus: Robinhood, investor letters, and the HFT arms race

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

News

Nasdaq Earnings: The good times kept rolling for Nasdaq in Q2 2021. The company reported earnings on July 21 and revealed +15% organic revenue growth, +23% EPS growth, and a $475M accelerated buyback program to be completed by Q4. Nearly all business units contributed to the strong quarter; Transaction revenue grew +10% on the back of historic options industry volumes. Listing & IR services revenues got a SPAC-mania boost for yet another quarter. Even Market Technology, a unit that’s been more of a drag than a point of pride recently, put up mid single digit revenue growth & a recovery in margins.

The real star of the show since early 2020 has been Nasdaq’s Index business - Q2 was the sixth consecutive quarter with Index revenue growth above +20%. A combination of tech stock concentration, passive investing demand & new ESG products has ballooned interest in the exchange’s indices since COVID began. I think Nasdaq can ride the tech index wave for a bit longer before tough comps bring growth back down to earth. I’m continuing to hold my Nasdaq shares as long as trading AND data revenue outperform simultaneously.

MarketAxess Earnings: MarketAxess had quite a packed schedule of news updates this week. First, the company announced the addition of Charles Li, former CEO of the Hong Kong Exchange, to its board as it eyes deeper expansion in Asia. Second, longtime CFO Tony DeLise announced his transition out of the role - Head of Finance & Accounting Christopher Gerosa is set to succeed him. I find the announcement a bit peculiar considering DeLise will still be with MarketAxess for the time being as its head of IR and Corporate Development.

Lastly, MarketAxess released Q2 earnings on July 21, reporting a decline in revenue & EPS against difficult YoY comps in 2020. CEO Richard McVey gave a few insights during Q&A that I think will have an important impact on the stock going forward:

When asked about sluggish market share gains vs. competitors (ie Tradeweb), McVey said MarketAxess share is more sensitive to volatility and has been suffering from a quiet market of late.

McVey estimated that the corporate bond market can become 60-70% electronic over time vs. ~40% electronic today, which I think is a lower upper bound than the market has been expecting.

McVey also said that trading velocity is now an equally big, if not bigger driver of volume growth than market share gains in the future.

The fact that MKTX is now trying to take the focus off market share and onto something else (like trading velocity & volatility) makes me think the sluggish growth numbers are set to continue. I’m still avoiding the stock for now.

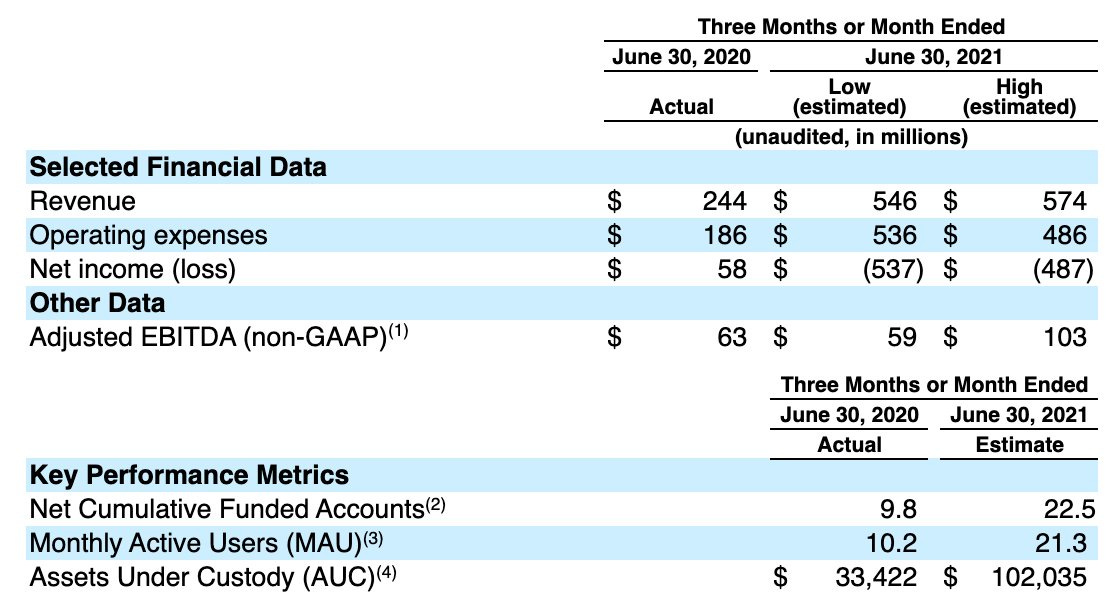

Robinhood Expects IPO to Value Trading App at About $33 Billion: On July 19 Robinhood released an amended S-1 to the public which included more specifics about its upcoming IPO. Included in the filing was an estimate of Q2 2021 performance (pictured below) - it ended the quarter with revenue +130% YoY, 22.5 million accounts, and average account balance of ~$4,500, up +50% from the end of 2020. At $33 billion Robinhood is being valued as if historic growth in retail trading interest will continue on forever at its current pace - I don’t recommend getting into the stock on day 1. I did a full Robinhood write-up in preparation for thier IPO next week - you can find this writeup here.

(Source)

Nodal Exchange Achieves New Records In Power And Environmental Futures: Another under-followed story in the futures markets this year is that of Nodal, the Deutsche Borse owned exchange that’s been quietly taking over the US power & emissions market. In June 2021 Nodal set new volume records in US power futures with 175 TWh traded during the month, or enough power to light up New York City for three years. Since launch in 2009 Nodal has slowly taken market share from ICE and CME by offering differentiated products, strategic M&A (it bought Nasdaq’s futures business in 2019) and competitive fees with help from powerful exchange backers. Power futures by itself isn’t a massive market, but even the tiniest foothold can quickly mean serious pressure for competitors in adjacent products as liquidity & market influence builds.

I recently launched a paid tier to this newsletter where I provide more deep dive research on exchanges & market structure stories that matter. If you sign up before August 1, 2021 you can use the below link to get 20% off an annual subscription. Thank you for your support!

Other Stories I’m Reading

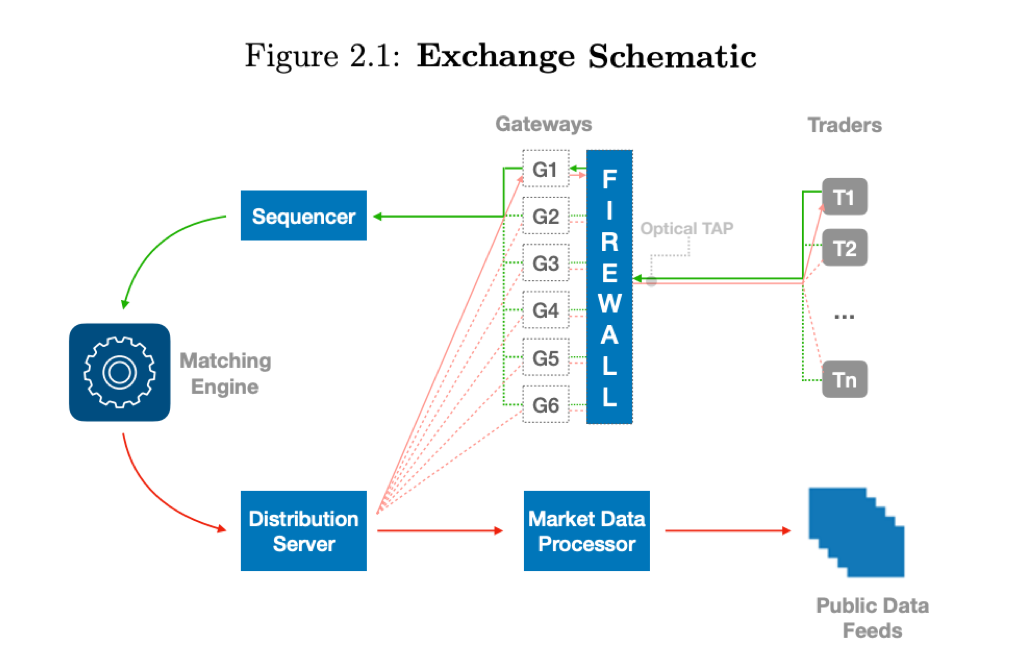

Quantifying the High-Frequency Trading “Arms Race”: This academic paper was published in January 2020 and re-appeared in the news recently, making it a good time to revisit the study. Researchers obtained detailed market data from the London Stock Exchange over a 43 day period covering all FTSE-350 stocks, amounting to over 2.2 billion messages. They used this data to reconstruct a day in the life of a high frequency trading firm engaged in the profitable but controversial business of “latency arbitrage”, using speed to exploit market fragmentation. The messages revealed that HFT races account for ~20% of daily trading volume & involve 3-5 firms competing for ~£60 million per year in arbitrage profits. Extrapolating this across global equity markets brings the total latency arbitrage profit pool to $5 billion; many believe it’s even greater than that.

The paper also includes a great primer on the design & operation of a traditional exchange, making it a timeless read regardless of the argument about HFT. Included in the background research is a detailed explanation of limit order books, exchange gateways, and the core matching engine (pictured below):

Upslope Capital Management Q2 2021 Investor Update: George Livadas, a portfolio manager based in Colorado with an active Twitter presence, puts out very insightful quarterly letters to investors & the public with updates on his portfolio. Livadas owns a few exchange stocks including CBOE & TMX and until recently was a longtime holder of MarketAxess. In his Q2 update Livadas details a change of thesis on the stock, citing uncomfortably high valuation in the face of poor market share results in 2021 compared to Tradeweb, its fast-emerging corporate bond rival. I liked the below section in particular:

“…for a number of years market observers worried MKTX could lose ground to TW due to its lack of treasury/hedging capabilities. In late 2019 MKTX moved to address the issue by making its largest-ever acquisition and buying LiquidityEdge. That TradeWeb has gained so much ground against MarketAxess 20 months after the deal closed suggests potentially deeper innovation issues.”

MarketAxess is a corporate bond exchange through and through while Tradeweb is more diversified with US Treasuries as its flagship product. Recent share gains in corporate bonds may be a sign that customers are opting for Tradeweb as a one-stop-shop for multiple fixed income markets (including corporates) over the singular product of MarketAxess. I agree with Livadas on his thesis and am expressing this view by owning TW rather than shorting MKTX.

Chart(s) of the Week

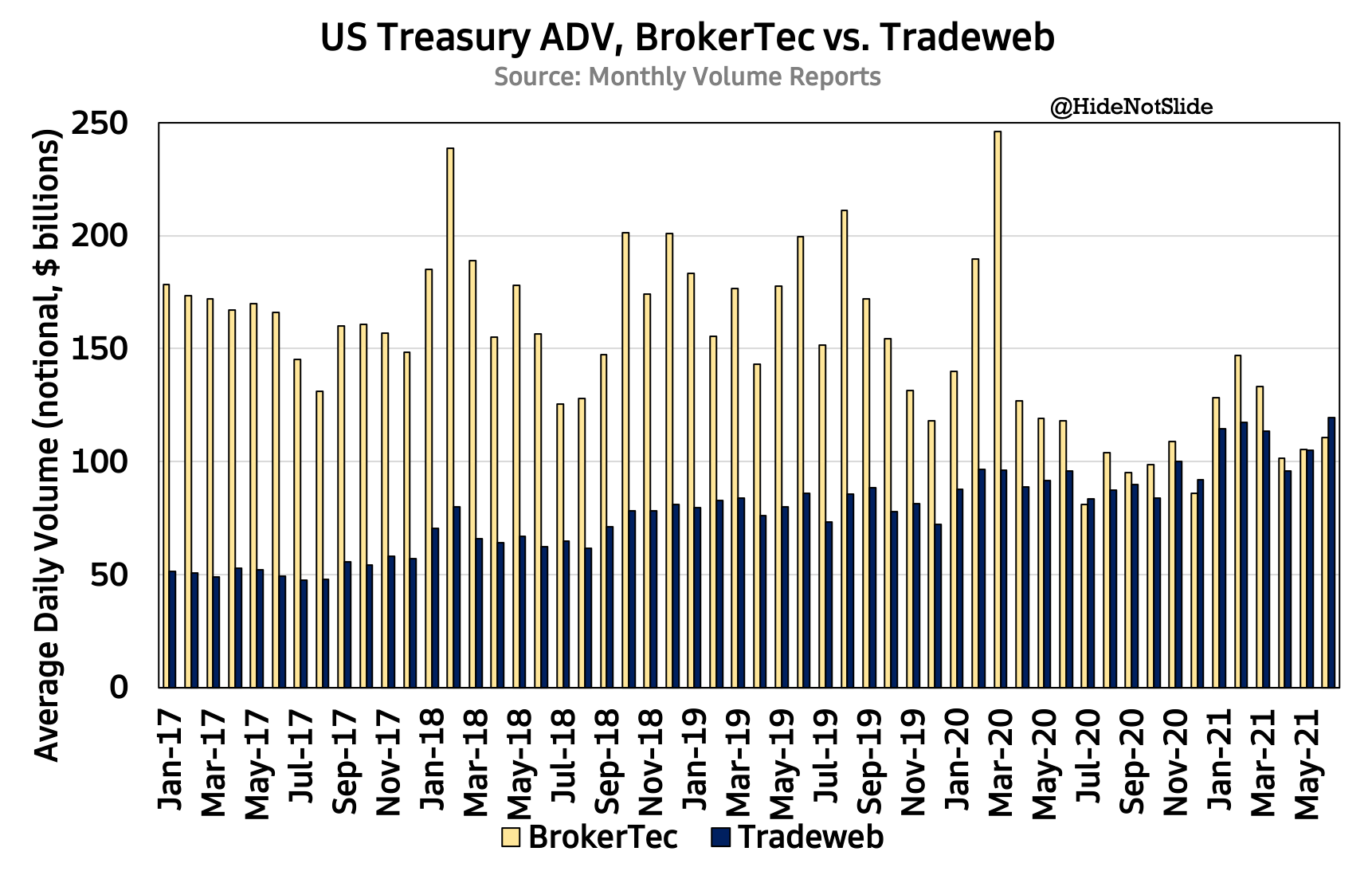

Speaking of Tradeweb, the fixed income exchange hit another big milestone last month in its battle with BrokerTec for the US Treasury market. As a reminder, the spot US Treasury market is one of the largest in the world & can be split into two halves: the dealer-to-dealer market (D2D) and the dealer-to-client market (D2C). The D2D space is mature, fully electronic & largely controlled by BrokerTec, a unit of CME since 2018. The D2C space is more dynamic and competitive - the shift to electronic trading hasn’t finished yet and competition is neck & neck between Tradeweb & Bloomberg for market share:

In June 2021, Tradeweb’s total US Treasury volume surpassed BrokerTec for the third time in its history (the first being July 2020). This is due to a few catalysts - first, the D2C market is becoming more electronic, giving Tradeweb a secular growth boost BrokerTec can’t capture. Second, Tradeweb is benefitting from what George Livadas highlighted above - customers wishing to trade corporate bonds & US Treasuries at the same time are using Tradeweb in greater quantity, making their platform more valuable than a pure-UST exchange like BrokerTec.

Third, Tradeweb closed on its acquisition of eSpeed on June 25, giving it three days of added D2D volume for the month of June. I expect BrokerTec market share to begin eroding as Tradeweb integrates eSpeed into its larger ecosystem and gives the business more focus than what Nasdaq was able to give.

I’m long both CME and Tradeweb at the moment, but I’m more excited about Tradeweb in the short term given its wins in both corporate bonds and US Treasuries against all competitors.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, COIN and VIRT. I am also long Bitcoin, Ethereum, and UNI.