Sourmash & Hedge Clipper

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

January 17, 1989 was the last real day of open outcry trading on the CME.

It was a cold & busy morning that Wednesday as the loud, colorful Chicago trading community made their way to the futures pits. Markets were digesting new political rhetoric out of West Germany and its impact on commodities & the US dollar. The joyful haze of the Christmas holidays was quickly fading & Wall Street was returning to work. The pits felt like they always did in their 1980s heyday - shouts of bids & offers filled the warehouse-sized exchange floor as thousands of thick-skinned veterans transacted billions of dollars in futures for their global clients. As the afternoon brought markets to a close the pits slowly emptied & traders made their way home, not knowing how different life would be when they returned the next day.

That night federal authorities put their carefully planned, years-long operation into motion. FBI agents were dispatched to the homes of dozens of CME & CBOT traders to disclose an investigation into alleged racketeering, market manipulation & fraud in the trading pits. Many hours of audio & video records had been collected incriminating participants across all parts of the exchange, leading to indictments of 46 traders in what remains one of the largest FBI sting operations in US history.

Other than a great story, the genesis, execution & fallout of this now famous operation can teach us much about how markets, traders & regulators succeed - and fail - to this day. How did the FBI pull off a sting of this size in Chicago’s trading pits? Were futures traders really breaking the law? Was justice served?

Infiltration

Our story begins in 1985 - four years earlier - with Anton Valukas, the newly appointed U.S. Attorney for the Northern District of Illinois under Ronald Reagan. Valukas had his sights set on financial crime from day one on the job and knew precisely where he could find a case worth pursuing. Before his appointment Valukas had spent years working for Jenner & Block, a Chicago law firm with many CME & CBOT traders as clients. Valukas first heard about wrongdoing in the pits while defending traders from the very authorities he now led. If anyone knew what kind of skeletons were hiding in the closets of commodity traders, it was him.

Interest in a case intensified when authorities received a complaint from Archer Daniels Midland (ADM), a large corn & soybean processing firm & broker on the CBOT, about rigged markets & unfair trading practices. The combination of Valukas’s experience & complaints from customers was too great to avoid any longer, and in 1986 a full-fledged FBI probe began to form. Operation Sourmash (the CBOT probe) and Operation Hedge Clipper (the CME probe) had been launched.

To try and infiltrate the trading pits the FBI sent two undercover agents - Richard Lee Carlson & Michael McLoughlin - to pose as floor clerks working for ADM. Each agent spent the next year working, learning & slowly blending in with their fellow clerks, using fake backstories, academic records & resumes to stay under the radar. While a good first step inside, a floor clerk was considered the lowest position on the trading floor & didn’t come with access to top traders or their potentially illegal dealings. Carlson & McLoughlin needed closer proximity to the action if they were truly going to blow a racketeering case open in the futures pits.

In December 1987 both agents purchased official seats on the Chicago Board of Trade for a total of $800,000. The FBI used a special fund to pay for the seats & spent considerable resources setting each agent up to look the part of a successful CBOT trader. Carlson leased an expensive Chicago apartment, wore a gold Rolex & drove a Mercedes to work. Both agents frequented luxury gyms, restaurants & clubs where other high-profile traders spent their time. To befriend CBOT veterans one had to act like a CBOT veteran, and Carlson & McLoughlin made it their mission to play this part with extreme precision. Both operatives even tried their hand at pit trading, using government funds to bet on commodity prices. Both lost money trading but were able to comfortably befriend the CBOT community in the process. After more than a year & hundreds of thousands of dollars in costs, the FBI had finally breached the pits.

Observation

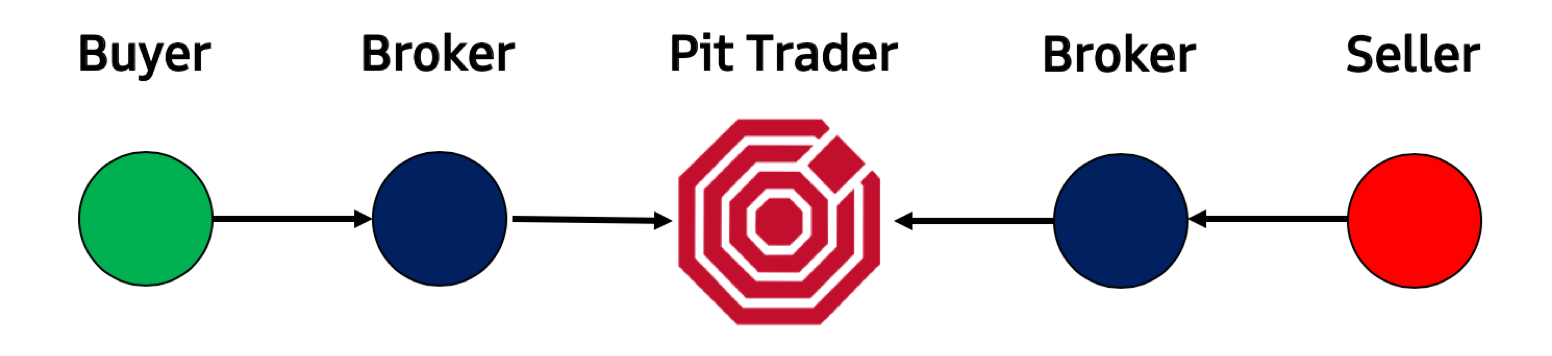

By securing their seats on the Chicago Board of Trade, Carlson & McLoughlin had bought front row access to the largest, most active commodities trading venue on the planet, with real institutional clients & an important role to play in the global economy. Banks, governments, farmers & companies like Archer Daniels Midland needed CBOT’s liquid markets to hedge the price risk associated with their business on a daily basis. For example, if a farmer wanted to grow & sell soybeans for a guaranteed profit, it needed a way to lock in selling prices & create certainty with which to plan their crop - something only CBOT’s soybean futures contract could give them.

To buy or sell a soybean future, a farmer would call their broker, the middle-man who could provide margin & hold their assets for safekeeping, to place an order. These brokers either partnered with pit traders to execute the order for them or owned exchange seats directly to execute trades themselves. The pit trader would receive the order & work within the soybean pit to get the best price for their client, relaying final settlement price & quantity back to its customer after the trade was done.

Other than brokers & their traders, everyday speculators bought exchange seats & traded for their own account to make a living. By taking the other side of farmers & other clients in the pit, speculators took risk by holding positions in a volatile market but collected wide spreads & could make significant money if their bets were right. Electronic trading hadn’t taken over the futures market yet, meaning all trades & their associated information had to go through the open outcry trading pits. Pit traders controlled the liquidity, could see the entire market ebb & flow in one place, knew which brokers represented which big money clients & how those brokers acted when prices were about to make a major move. CBOT seat owners had coveted, exclusive access to a club that let them catch a piece of the riches flowing through its floor.

As the FBI’s probe continued into 1988, they finally saw what Valukas and ADM had suspected was occurring in the pits. Traders would make back-door deals to execute trades at certain pre-set prices that put their account over their customers. If a trader sold a soybean future at $5.50 per bushel, they’d sometimes forge the trade’s receipt to show a sale at $5.55, pocketing the extra $0.05 for themselves. Sometimes a big trader would engage in what’s now called “spoofing”, feigning a big buy or sell order to make markets react & then profiting off that reaction. For example - a trader would make it seem like they were about to submit a huge buy order in soybeans, tempting surrounding brokers & market makers to join in & let long positions run. If the trader’s act resulted in a short-term uptick in the price of soybeans, it could sell into the short term exuberance & make a profit without ever finalizing its initial buy order.

Some would argue these tricks & others like it were simply part of the cost of trading. If brokers & exchanges set their own prices & leveraged monopoly power for their own good, why shouldn’t pit traders do the same thing? Traders took enormous risk every time they stepped into the pit, and not everyone made it out rich. Many lost everything on days like Black Monday in October 1987, just a few months before the FBI purchased their CBOT seats. If a few forged receipts & manipulated trades kept food on the table & dozens of other pit veterans were doing it, how bad could it be?

My guess is this slippery slope, this dangerous internal justification of crime is what allowed the FBI to collect so much evidence. Why keep quiet about a few unsavory trades when it was so prevalent, at least in certain circles?

Carlson & McLoughlin wore wires constantly while meeting with fellow traders in and outside the pits, collecting dozens of hours of audio recordings. They involved themselves in many of these back-door price-fixing trades & recorded crimes at every step of the transaction. They even smuggled cameras into frequent meeting spots & added videotapes to their growing collection of evidence. By early 1989 the Feds felt they had a strong enough case to begin releasing their findings & bring action against their pit trader targets. The night of January 17 marked the end of the government’s silent sting operation & the beginning of a long & complex court battle that would take everyone by surprise.

This post is an example of the kind of content you can expect from Front Month Premium, the paid portion of this newsletter where I explore the companies, stories, and catalysts affecting the future of exchanges & market structure. Subscribers get immediate access to a long list of exchange research & at least two new posts per month.

Thanks for your support!

Execution

I wasn’t in the CBOT & CME futures pits on January 18, 1989, but I can imagine the paranoia & uneasiness that must’ve been palpable on the trading floor that day. Had fellow traders ratted each other out to the Feds? What evidence had they nabbed? Could FBI agents still be watching & recording them in the pits at that very moment? Who could be trusted anymore?

In total 46 traders were indicted on over 1,500 counts of racketeering, fraud, and lying to authorities. At a news conference later that year U.S. Attorney Valukas & Attorney General Dick Thornburgh shared more details of the investigation & the court battle that was to come:

“This probe is part of an expanding Department of Justice crackdown on white-collar crime from Wall Street to LaSalle Street to Main Street with all stops in between. The activities uncovered at these exchanges, the largest of their type in the world, cannot be tolerated.

We are talking about hundreds of customers and thousands of trades. We are not talking about technical violations. It can be fairly described as wide-ranging activity.”

(Source)

Trials took place in three phases, beginning with traders in the Swiss franc pit. Phase One showed prosecutors first-hand how difficult closing commodities fraud cases could be. Sixteen defendants admitted guilt & avoided maximum punishment through plea bargains, but cases that made it to trial found a surprisingly high number of split juries & outright acquittals after arguments had been heard. One trader named Robert Mosky served only four months in prison after pleading guilty to one count of wire fraud for cheating an investor out of $12.50 in a Swiss franc trade. $12.50!

If Phase One was described as a bad showing for the government, Phase Two turned out even worse. When twelve Japanese yen traders faced trial on 238 counts of criminal activity, not one guilty verdict was rendered. Lawyers claimed that prosecutors lost their case because they couldn’t find any tangible victims linked to their alleged crimes or lost money as a result of fraud. According to the defendant’s lawyers, “this is a death knell for this investigation.”

Phase Three focused on ten traders in CBOT’s soybean pit & did produce a majority of guilty verdicts in a last-minute save of face for the prosecution. Defendants were sentenced to more than three years in prison & fined nearly $1 million for their crimes.

Conclusion

After the dust had settled & all related cases had been closed, Operation Sourmash & Hedge Clipper were viewed with mixed opinions about its impact on crime in the futures pits. On one hand the government had won multiple guilty verdicts, sent several traders to jail & caused exchanges to change their policies to cut down on manipulation. On the other hand, prosecutors had spent millions of dollars & five long years bringing actions against traders with an underwhelming trial record to show for it. Was the investment of time & resources worth it?

Open outcry trading wasn’t the same after news of the sting operations were unveiled. Shortly after Sourmash & Hedge Clipper had officially ended, in 1992 CME launched their Globex electronic trading platform, marking the steady but certain end to the human trader’s monopoly on volume & information at the exchange. Veterans of the pit saw their way of life slip from their fingers as indictments & arrests in their midst gave way to computerized trading & the shutting down of physical trading floors.

Thanks to technology, government action & the actions of a few rogue traders, January 17, 1989 might have been the last time the normal, decades-long routine of an open outcry physical commodities trader was ever seen.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Solana.