One Country, Two Systems, Little Choice

One Country, Two Systems, Little Choice

The complex past & uncertain future of the Hong Kong Exchange

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

In late November 2019, the eyes of the world descended on a small college in downtown Hong Kong, anxious to learn the outcome of an increasingly violent political rebellion.

The people of Hong Kong were engaged in the largest series of protests the city-state had ever seen, speaking out against an extradition bill that effectively subjected Hong Kong civilians to Chinese law & authority. Peaceful marches during summer 2019 quickly descended into violent clashes between police & protesters, resulting in over 10,000 arrests & multiple deaths.

By the fall protests had reached their most violent stage, culminating in the police siege of Hong Kong Polytechnic University. Students & pro-democracy supporters sealed themselves in the college over a two week period, fighting police forces with bricks, Molotov cocktails and even chemicals from the college’s science lab. Hong Kong government forces responded with tear gas, water cannons & live ammunition to break through the barricade & quell the protest. Thousands were arrested & nearby hospitals were overrun with injured civilians. Media outlets covered the action around the clock, and Western governments denounced China’s effective takeover of Hong Kong and the violence their actions were causing.

All the while, just a few miles away across Victoria Harbor, Hong Kong’s stock exchange was about to finish its second consecutive year of record trading. Blockbuster listings including Alibaba & Budweiser APAC helped the Hong Kong Exchange secure another year as the world’s #1 choice for IPOs. Nearly $3 trillion of annual transaction volume further boosted results. Apart from a couple weeks of choppy performance in the Hang Seng Index during the fighting, exchange activity continued on as if nothing unsettling was taking place just across the bay.

This stark image of Hong Kong’s top exchange enjoying a record year while violent riots fill its streets is a good way to view this market venue’s peculiar situation. Viewed in one light, HKEX could be considered one of the world’s most powerful exchanges, frequently called the “Nasdaq of Asia” with a market-leading position in the world’s fastest growing set of economies. In another light, HKEX could be viewed as nothing more than an emerging financial arm of the Chinese government, both propped up & constrained by Hong Kong authorities & its Beijing handlers.

What are we to make of these conflicting narratives? Should the world be taking HKEX seriously? What kind of future can the exchange expect going forward?

As Goes A Nation, So Goes Its Exchange

Hong Kong Exchanges & Clearing didn’t exist in its current form until March 6, 2000. A fragmented field of national stock & derivative exchanges launched in the early 1900s slowly morphed into three major venues: The Stock Exchange of Hong Kong, the Hong Kong Futures Exchange, and the Hong Kong Securities Clearing Company. Impressive growth in the Hong Kong economy combined with the advent of electronic trading compelled regulators to update & reform its financial system. It did so by pressuring its three exchanges to merge into one conglomerate, helping to improve liquidity & compete with Western capital markets. After many months of negotiations between the government and shareholders of the three companies, a merger was completed in early 2000 and HKEX was officially born.

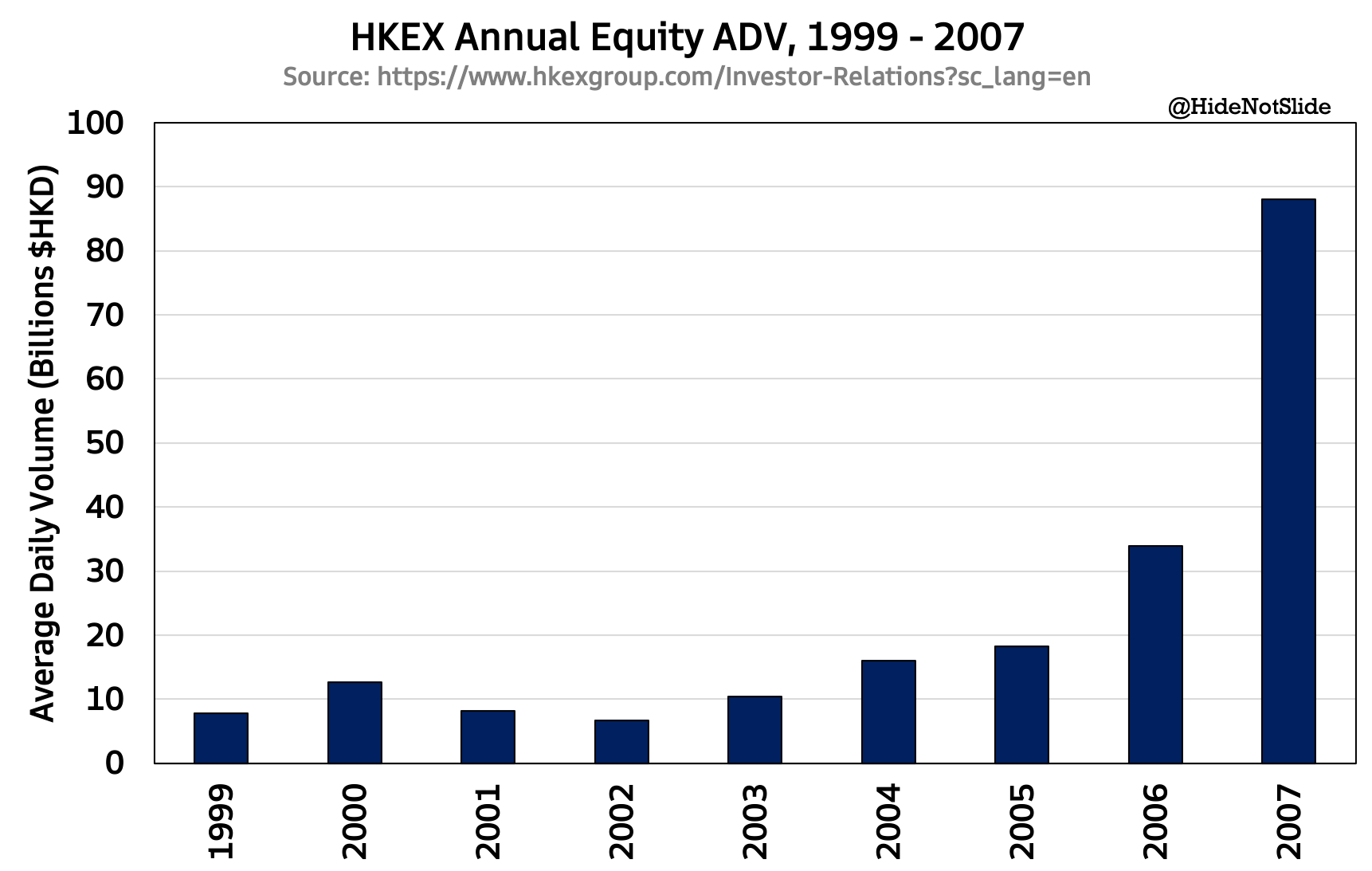

The next phase of Hong Kong’s evolution would prove the government’s decision to merge its exchanges together as a good one. Hong Kong’s flagship Hang Seng Index saw spectacular performance coming out of the post-tech bubble recession, buoyed by Western capital inflows & the prospect of China allowing its citizens to purchase stocks on HKEX. Hong Kong equity & derivative volumes grew by nearly 7x between 2000 and 2007 as its indices soared:

(Source)

With a secure grip on Hong Kong’s equity market in tow, HKEX began focusing on building relationships abroad. News surfaced in mid 2007 that the NYSE & Nasdaq were planning to open offices in Beijing, looking to attract Chinese listings to the US and prompting rumors of a partnership with Shanghai or Hong Kong. The global financial crisis of 2008-09 delayed these expansion plans, and by the time a recovery was in the works, HKEX had set its eyes on a new target: London.

HKEX’s first major move on the world exchange stage came in 2012 with the blockbuster acquisition of the London Metal Exchange. HKEX’s $2.2 billion purchase price reportedly beat rival bids from ICE, CME, and NYSE Euronext, giving it control over the world’s largest base metals market & a sizable presence in the UK. HKEX CEO Charles Li also touted distributing LME metals data in Asia as a key strategic reason to pay top dollar for the exchange, over 100x LME earnings at the time. The HKEX-LME acquisition came at a time of intense M&A jockeying in the exchange space - notably the multiple attempts by Nasdaq, Deutsche Borse and ICE to buy the NYSE, ending with ICE’s successful purchase of NYSE and spin-off of Euronext in early 2013. Taking LME off the market likely sparked renewed urgency by other global exchanges to ink deals while M&A targets were still available.

Your Greatest Gift - And Your Deepest Curse

As Hong Kong’s flagship exchange group grew ever more powerful, the shadow of government intervention could no longer be avoided. When Hong Kong was handed over to China in 1997 the CCP established the principle of “one country, two systems”, giving Western markets hope that Hong Kong markets would stay relatively free & China would slowly open its economy to match.

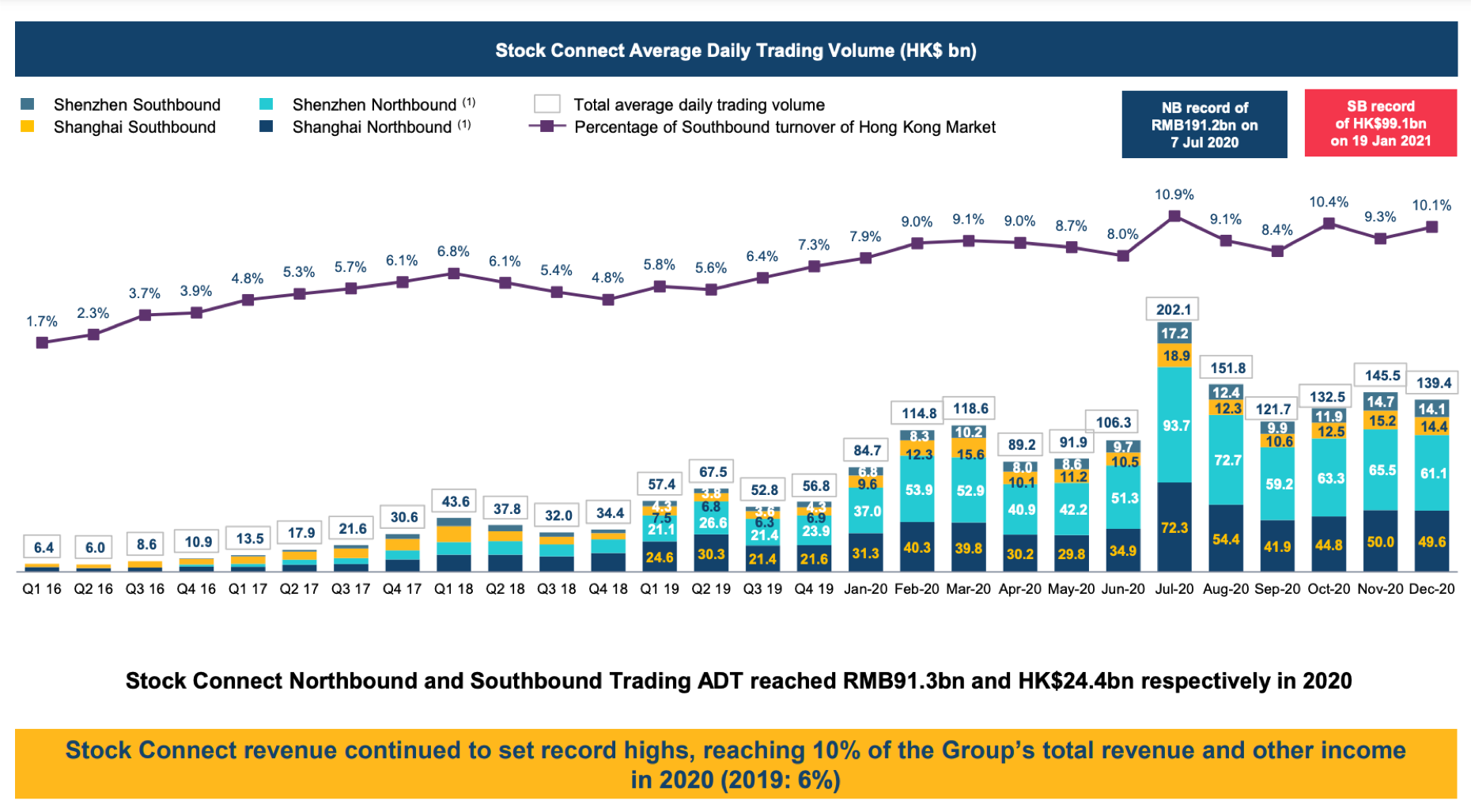

China looked to be making good on its “one country, two systems” promise when it approved HKEX’s Stock Connect program in 2014, allowing mainland Chinese investors to trade Hong Kong securities & vice versa. With new access came a surge in trading volume, interestingly more from “northbound” trading (Hong Kong investors trading Chinese markets) than “southbound”. Stock Connect activity now accounts for 10% of HKEX’s total revenue:

(Source)

While a close working relationship with China certainly has its benefits, HKEX has also become well aware of the mounting costs. Today the Hong Kong government is HKEX’s largest shareholder with ~6% ownership of the company and control over 6 of its 13 board seats. While not a majority holder of either shares or voting power, it’s safe to say that major changes at HKEX don’t happen without government approval. Taking it one step further, it’s safe to argue that China exerts significant if not complete control over Hong Kong government policy and its exchange assets as a result. When investors hear rhetoric coming from the desk of Hong Kong Exchange management, they need to assume that Chinese motivations are a big driving force behind their agenda.

Viewing HKEX through a Chinese-controlled lens helps us understand why the exchange’s biggest M&A attempt yet proved an utter failure. In mid-2019 the exchange made a bold, out of the blue bid for the London Stock Exchange, valued at a staggering $39 billion. HKEX management touted closer Asia-European ties & integration with LME as reasons for the deal, but were swiftly rebuffed by LSE shareholders. Apart from working on their own blockbuster bid for Refinitiv, LSE cited national interests as a reason to reject Hong Kong’s bid. Does Britain really want two of its top exchanges owned by a Chinese-controlled entity?

Within three weeks of announcing its bid, HKEX walked away from the deal citing a lack of engagement from LSE management. The exchange’s close ties with China had spoiled its biggest global foray to date.

With foreign expansion plans dashed, HKEX seemed to be left with one viable growth path - leaning into its status as the largest exchange connecting global markets to Chinese assets, strategically labeled “China Anchored, Globally Connected”. Top Chinese companies wishing to go public looked to Hong Kong as their listing venue of choice, bringing waves of IPOs and equity trading volume to HKEX. Stock Connect activity reached new highs & became a bigger percentage of revenue. Everything HKEX touched in the past related to China has now become its main sources of sustainable growth.

The 2021 Tightrope

HKEX enters 2021 at a major crossroads. The exchange has partnered with China under the promise of “one country, two systems”, but this promise is turning out to be little more than a wishful dream. Chinese political intervention in Hong Kong is causing violent unrest from its citizens. The US is considering a ban of Chinese listings in domestic markets. Fears of Western capital flight out of Hong Kong have spread rapidly. Military action in Taiwan & the South China Sea has become a real possibility in the coming months.

And yet despite the chaos erupting all around it, HKEX keeps putting up record numbers and rivals many US exchanges in size. The exchange has & will continue to benefit from protectionist Chinese economic policy, funneling IPOs and trading volume to Hong Kong in returns for influence & control. HKEX has little choice but to comply.

Honorable Mentions

S&P Global paid a $9 million fine to settle SEC charges related to its construction of indices underpinning the now infamous XIV ETN that blew up on Feb 5, 2018. According to the SEC, S&P Global did not disclose that its volatility indices contained an “auto-hold” feature that caused its value to remain static even as the VIX itself was spiking higher.

Cryptos crashed this week as Bitcoin dropped -40% since May 1, bringing the rest of the industry down with it. Catalysts for the selloff include Elon Musk whipsawing narratives via Twitter & renewed support of a crypto crackdown by Chinese authorities. During the most intense part of the selloff around 10 AM eastern US time, Coinbase experienced another app crash, preventing customers from logging in or even seeing quotes for certain coins.

ICE announced a strategic investment in BondLink, a platform that helps public sector CFOs raise money through municipal bond offerings.

Chart of The Week

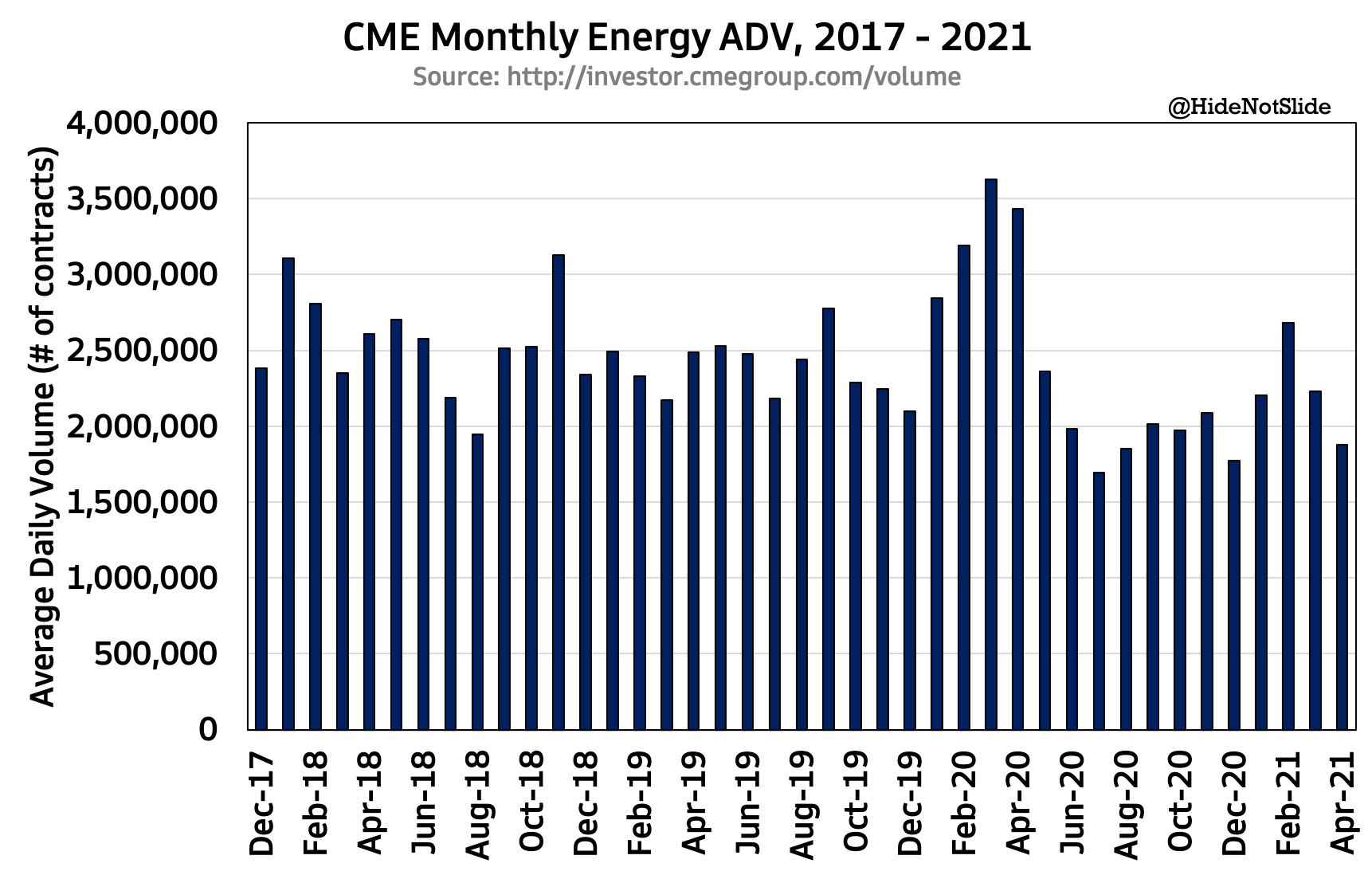

CME this week announced the upcoming launch of Micro WTI Futures, contracts 1/10th the size of its larger counterpart giving retail users more nuanced access to the market & institutional customers another arbitrage opportunity to keep the prices of each contract in line with each other. The move comes as CME relishes the success of two other mini/micro contract launches: Micro equity index futures & mini Bitcoin futures. Its only logical to assume this trend of “mini-ization” will continue for markets with a large retail user base and high contract prices. CME’s energy complex could use a new product or two - volumes have been stagnant since late 2017:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, COIN and VIRT. I am also long Bitcoin and Uniswap’s UNI governance token.