My Coinbase Gameplan

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

On February 25, Coinbase dropped its detailed S-1 filing to the public, causing the same frenzied & elated reaction among the crypto community that Taylor Swift fans give to the announcement of a new world tour. Coinbase’s market debut is expected to be one of the largest of 2021, with valuations reaching as high as $100 billion in the private market. That’s more than any public exchange in existence today, including ICE, CME & Nasdaq.

As informed investors in the exchange & market data space, what are we to make of Coinbase? Should we buy into the hype & think about getting in on day 1, or stay on the sidelines and avoid a crypto exchange bubble in the making? This post serves as an organized analysis of Coinbase’s prospects & realistic future, helping to answer that very question.

Regardless of your thoughts on Coinbase & even crypto at large, this direct listing is worth your attention. beginning with CME’s demutualization & IPO in the early 2000s, all but one major exchange has outperformed the S&P 500 since going public. CBOE is the only exception - they began underperforming in 2018 when Volmageddon hurt the exchange’s VIX business & resulting returns. Coinbase certainly counts as a major exchange. Will they keep the streak alive?

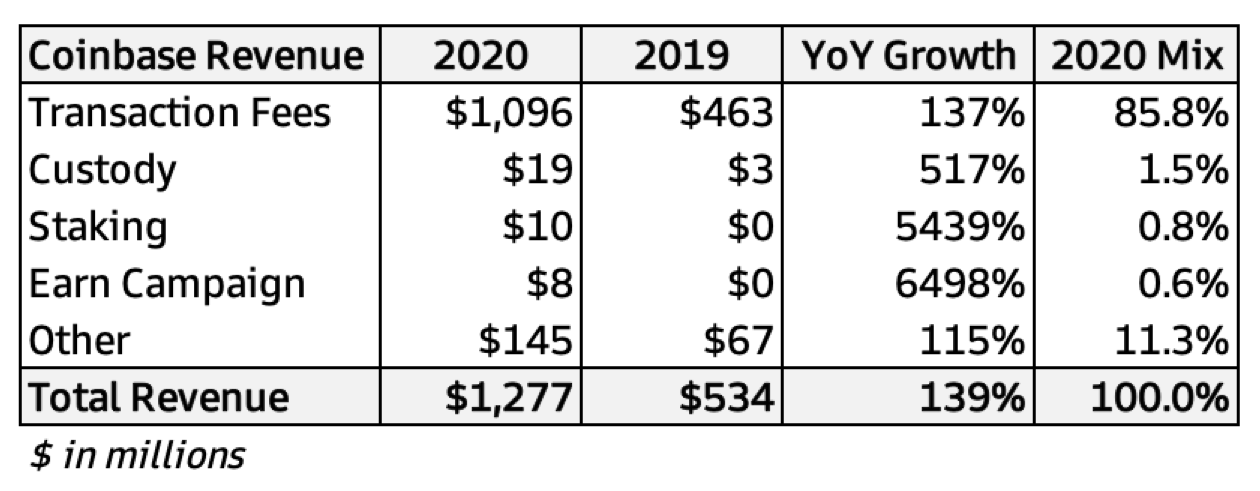

Coinbase’s S-1 filing revealed the true size & scope of their operations, as well as their key sources of revenue. I’ll give a brief summary below:

(Source)

Transaction Fees (86% of revenue): This is Coinbase’s bread & butter service and what many think of when referring to or interacting with their ecosystem. When customers trade cryptocurrencies through Coinbase’s app they’re charged a % of notional traded depending on the asset & size of the trade. The core service Coinbase is providing here is liquidity - the ability to buy or sell eligible crypto assets conveniently, securely & with near instant execution. The way Coinbase does this is similar to other successful exchanges - they entice institutional customers with sizable fee discounts to absorb flow from their 2.8 million active retail users, who pay full price. As of Q4 2020, institutional customers accounted for two-thirds of Coinbase’s trading volume but only 5% of transaction revenue. Most of their transaction fees come from two trading pairs - Bitcoin & Ethereum - but the company recently tweaked its institutional rebate program to incentivize trading in less popular, illiquid currencies.

Custody (1.5% of revenue): In addition to trading, customers can use Coinbase to safely store crypto assets & protect them from being stolen or lost to hackers & thieves. Coinbase then collects a daily fee based on the value of these assets held under custody. A high-profile user of Coinbase’s custody solution is Grayscale’s Bitcoin Trust (GBTC), currently the largest exchange-traded product retail investors use to get exposure to Bitcoin, with over $13 billion in AUM.

Staking (0.8% of revenue): While a small part of their business, Coinbase does get a bit of revenue from supporting the underlying blockchain of certain cryptocurrencies, including validating transactions & receiving crypto rewards for doing so.

Earn campaign (0.6% of revenue): Coinbase also makes money by facilitating education of new cryptocurrencies to its userbase. When customers receive rewards for watching videos & performing certain tasks, Coinbase gets a small commission from the cryptocurrency sponsoring the educational resources.

Other (11.3% of revenue): This includes gains from selling crypto held on Coinbase’s balance sheet, licensing & analytics revenue, and interest income received on its cash.

A Coinbase Investment Framework

In my opinion, it is extremely difficult to build a strictly quantitative investment case for Coinbase at its current valuation. A ~$100 billion valuation against 2020 revenue of $1.3 billion implies a 77x price/sales ratio, orders of magnitude above other exchanges & most public companies for that matter. Before shaking our fists and shouting “Bubble!” at this, we need to understand & pressure test the narrative supporting Coinbase’s valuation. I believe this narrative has 4 pillars:

Coinbase will dominate crypto market infrastructure in the US.

Coinbase is more than just an exchange.

The “cryptoeconomy” will become a sizable portion of the real economy.

Bitcoin & Ethereum will continue to rise in price relative to USD.

Coinbase bulls believe these predictions will come true over a medium to long term time horizon, with the expectation that revenue & profitability catch up to the narrative as it plays out.

I largely agree with the narrative’s first pillar - Coinbase will dominate crypto market infrastructure in the US. When we look at the global crypto exchange landscape, Binance, Huobi & OKEx outpace Coinbase in reported trading volumes & size. While these exchanges do compete with Coinbase for users & market share around the world, I don’t believe they will ever have much success in the US. A critical differentiator in the crypto space is trust - users need confidence in the safety of their assets & the integrity of the exchange with which they do business.

The non-US exchanges are sorely lacking in this regard. Binance has been hit in the past with debilitating hacks & stolen crypto assets, and has recently been accused of setting up an elaborate corporate structure to avoid punishment by US authorities. Huobi’s COO was arrested in late 2020 amid a Chinese crypto crackdown. OKEx had to suspend part of its operations around the same time as it disclosed investigations & regulatory scrutiny of its own. All three exchanges have had to move headquarters to Malta & the Seychelles to avoid the prying eyes of legitimate governments, and have been accused of artificially inflating trading volumes to appear larger than they really are.

Compare this with Coinbase, a US-headquartered exchange with strict oversight by the CFTC, the SEC and financial regulators in the UK and Europe. Coinbase hasn’t suffered a large scale hack or theft of its exchange, despite numerous attempts that Coinbase has successfully defended & quashed. The exchange’s integrity is unmatched by similar sized competitors. As the largest crypto exchange under US regulatory authority, Coinbase acts as a lightning rod for retail & institutional money looking for safe exposure to Bitcoin.

This brings me to pillar #2 - Coinbase is more than just an exchange. Again, I believe this argument has merit. In the classic US financial system, institutions have found success by each owning different parts of the market value chain. We see companies like Robinhood, TD Ameritrade & Schwab own the retail brokerage space, State Street & BNY Mellon own custody, Paypal, Visa & Mastercard own payments, and the NYSE & Nasdaq own the core equities exchange business.

When we switch to the crypto financial system, Coinbase is a serious force if not a market leader across all parts of the value chain. Coinbase owns the retail brokerage, the custody solution, the core exchange matching engine, and is a tough competitor in crypto payments. A mega-bullish potential future for Coinbase could see their business become not just “NYSE for crypto”, but “NYSE + Robinhood + State Street + PayPal for crypto”. No wonder their valuation is so inflated.

Coinbase’s dominance via vertical integration won’t matter if the crypto industry as a whole doesn’t grow substantially in the coming years. Pillar #3 - The “cryptoeconomy” will become a sizable portion of the real economy - is where opinions begin to vary widely among investors & where I’m not fully bought in. In my opinion, for this prediction to come true there needs to be a commercial reason to buy & sell cryptocurrencies as part of a company’s normal course of business.

Think about large, established markets that have stood the test of time - agricultural commodities, oil & natural gas, even interest rates. All of these markets thrive because companies profit from selling the underlying good to consumers. The oil market is not just people speculating on the price of oil - it’s upstream & downstream energy producers buying & selling oil to operate their business. The corn market is not just people speculating on the price of corn - it’s farmers & manufacturers trading & hedging their corn exposure so they can offer cheap groceries to consumers. Who are commercial participants in the crypto markets?

Right now, very few people truly consume Bitcoin, meaning use it as a form of payment. From this perspective, I personally don’t believe US consumers will ever be paying for groceries or everyday expenses in Bitcoin or Ethereum, two highly abstract & volatile assets. In the US consumers hold Bitcoin as a speculative investment vehicle - they think prices will continue to rise relative to USD. Why pay for Pop Tarts with your treasured moonshot investment?

I believe there are long term use cases for Bitcoin (& Coinbase by extension), but they all center around its value as a speculative vehicle. For example, the broader crypto ecosystem & Coinbase in particular will benefit handsomely from the eventual approval of a Bitcoin ETF in the US. A Bitcoin ETF would be an effective “commercial use” for the crypto markets if only a frictionless way for retail masses & 401K holders to hold Bitcoin in their retirement accounts. Investment pillar #3 depends on how big the cryptoeconomy truly becomes. I think the cryptoeconomy will grow enough to facilitate cheap, widespread speculation, but I don’t think it will be as commercially viable in the US as Coinbase’s biggest fans might hope.

This brings me to the final pillar of the Coinbase investment case - Bitcoin & Ethereum will continue to rise in price relative to USD. Coinbase charges customers a fee based on the value of assets traded or held in their platform. Their custody business charges a percent of notional stored. Their transaction business charges a percent of notional traded. Coinbase even holds a non-trivial amount of Bitcoin on its balance sheet. Coinbase really really wants Bitcoin’s price to increase.

Will Bitcoin keep rising? In the short term I believe it will. Inflation is finally starting to creep upward. Prodigious fiscal & monetary stimulus is beginning to spur rises in consumer & producer prices. The market is waking up to the downstream impacts of inflation, and it’s narrowed safe haven assets down to two primary choices: gold & Bitcoin. A fixed supply of Bitcoin combined with growing demand from retail & corporate buyers looking for inflation protection should equal higher prices.

Pillar #4 plays into the notion that investors are using Coinbase - and Bitcoin - as a call option on rising universal crypto adoption & a way to satisfy their FOMO. If everyone has a tiny position in Bitcoin they won’t feel like they missed the boat if crypto does indeed take over the world at some point down the road. I think this narrative still has room to run, and Coinbase’s valuation implies others think so as well.

My Plan

After taking a closer look at the four pillars of a Coinbase investment case, I’m deciding not to buy the stock on day 1. While I believe Coinbase will have a stellar 2021 as Bitcoin FOMO continues to run wild, I’m not fully bought in to the idea that the crypto economy will grow enough to support a $100B exchange valuation. I need to see more institutional & core economic use cases for crypto before I pay that kind of premium.

While I’m not a buyer on day 1, I would absolutely build a position in Coinbase at the right price. Coinbase is in a perfect position to capture the ongoing Bitcoin bonanza & will grow as a facilitator of widespread crypto speculation in the US. I would very much like to own a piece of this story, but not for $100B. I think Mr. Market will give investors a chance to buy into Coinbase at lower prices in the coming months - I’m waiting on the sidelines & will be watching closely for opportunities to get in.

Honorable Mentions

Exchanges released mostly encouraging monthly volume reports as February came to a close. Rising inflation expectations & yields helped ICE & CME hit record volumes in key interest rate contracts. Equity & option activity stayed elevated in February as well, boosting CBOE & Nasdaq performance. MarketAxess was the only exchange that sold off after their release, as market share growth underperformed high expectations.

Piper Sandler analyst Rich Repetto upgraded CBOE to Overweight this week, citing improving volumes & RPC vs. prior estimates. The strong RPC is particularly notable & encouraging given ongoing competition with upstart exchanges MEMX, MIAX and LTSE. CBOE also filed a new Bitcoin ETF proposal with the SEC this week.

ICE CFO Scott Hill announced his retirement on March 2 after 14 years. His replacement is Warren Gardiner, former head of ICE’s Investor Relations group.

Chart of the Week

After 20 weeks of writing this newsletter, I’m happy to share that Front Month’s total email subscribers have surpassed 1,000. I wanted to take a moment to say thank you to all who’ve given this newsletter a try & have shared it with others. It really makes a difference.

Here’s to another 20 weeks of informative, relevant research & discussion of exchanges!

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Bitcoin.