MSCI Q4 2020 Earnings Review

MSCI Q4 2020 Earnings Review

This piece is part of a series on exchange & market data industry earnings - please SUBSCRIBE below for more earnings reviews & weekly writeups on the top stories in exchanges:

Links

Results

(Source: MSCI Investor Relations)

One thing that always makes it hard to understand & follow MSCI in my opinion is how many buzz-words are thrown around in their earnings calls and investor decks. “ESG”, “Climate”, “Factors”, “Thematics”, “Run-Rate”, the list goes on. Slide 7 in their earnings deck proves my point perfectly - quite simply a slide full of only buzz-words:

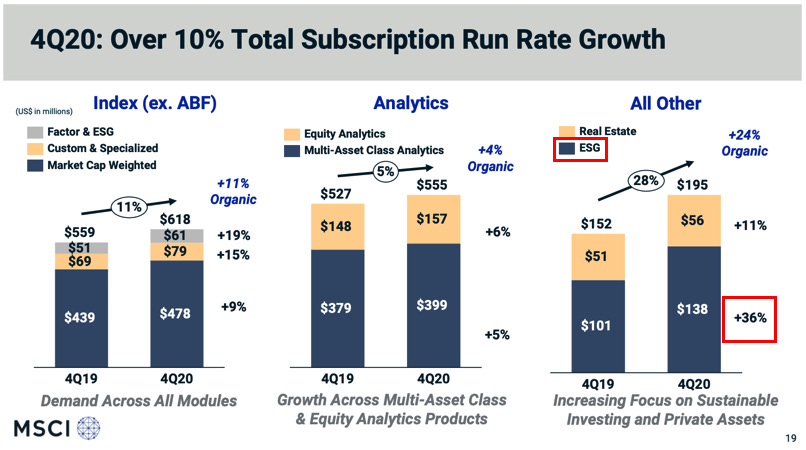

It can be hard to cut through the noise and understand MSCI’s position, but it’s not impossible. MSCI has grown earnings at a +20% annual pace since 2009. Much of this growth has come from demand shifting away from active management towards passive ETF management - those ETFs need indices to track, and MSCI owns many of the highest quality indices in existence. As younger generations steer nearly 100% of their investment inflows into passive products, MSCI’s associated index fees have steadily grown year after year.

Q4 2020 results showed this trend in action - MSCI‘s largest segment, Indices, notched +10% growth YoY driven by higher subscription & AUM fees as MSCI-linked assets surpassed $1 trillion globally. MSCI’s top customer is BlackRock’s iShares business, and BlackRock reported record EPS and assets under management this quarter. It only fits that MSCI would share in this success & grow with its largest client.

This strong, steady growth has pushed MSCI’s multiple into the high 50x range - consistent growth is a valuable commodity worth paying up for. As the passive thesis plays out over the next number of years, what’s next? What can surprise investors and convince more buyers to own the stock at this premium valuation?

Enter ESG. ESG investing is seen as a win-win for all parties involved - more climate-conscious millennial investors can choose funds they think are helping the world, and the financial community can pat themselves on the back for meeting this demand. For example, MSCI created an index called “MSCI ESG Leaders”, which packages large cap equities with the highest ESG ratings (supplied by MSCI) into one place. BlackRock operates an ETF that tracks this index - the iShares ESG MSCI USA Leaders ETF (ticker symbol SUSL). If you look at the top 10 holdings of SUSL compared to a normal S&P 500 ETF like IVV, they’re very similar:

(Source: BlackRock iShares ETF Summaries)

Since both these ETFs are quite top-heavy, investors get exposure to largely the same stocks regardless of which fund they choose. The kicker however is that SUSL charges 3x the fees of IVV. This is just one example, but it drives home a larger point that while ESG is marketed as a noble endeavor to clients, in many cases it serves as a way to extract more fees from the same basic asset management service.

MSCI doubled down on ESG during their Q4 earnings call, announcing the creation of a new “ESG and Climate” segment where they will combine their ESG ratings and analytics products into one more transparent reporting unit. ESG has been the fastest growing part of their business for multiple quarters with the expectation for a long runway of future growth ahead:

A bet on MSCI is a bet on the future of ESG. Demographics & regulation are pushing customers to demand more environmentally friendly investment options, and Wall Street is more than happy to oblige and extract higher fees from willing customers. While I understand the thesis and agree the industry is heading that way very quickly, I’m not a buyer of MSCI at current prices. I don’t fully believe the ESG hype & the quality of the underlying products, and am not willing to pay a premium price for exposure to it.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this post, I am long ICE, CME, CBOE, NDAQ and VIRT. I am also long Bitcoin.