ICE Q4 2020 Earnings Review

ICE Q4 2020 Earnings Review

This piece is part of a series on exchange & market data industry earnings - please SUBSCRIBE below for more earnings reviews & weekly writeups on the top stories in exchanges:

Links

Results

(Source: ICE Investor Relations)

ICE came into Q4 2020 at an inflection point in its trajectory as a public exchange. The company has now owned Ellie Mae for more than a full quarter, completed a re-segmentation of its financials, and announced its spinoff of Bakkt in a SPAC listing later in 2021. ICE’s new segments are a good way to view both the evolution of the company since its IPO in 2005 & its Q4 results.

Exchanges Segment - Act One

This segment is the oldest, most mature part of ICE’s business, and can be viewed as their “Act One” as a pure-play exchange. Since the beginning ICE has been an energy exchange more than any other asset class, and its Q4 results echoed this in spades. Exchange segment revenue was +6% constant currency driven by +8% growth in Energy revenue, the segment’s largest business. While globalization of oil trading & Brent’s success was the historical driver of energy growth, the new phase of growth is coming from natural gas. Gas revenue makes up ~1/3 of energy revenue & is rapidly growing with help from European TTF & global LNG volumes - again, a play on energy globalization:

(Source: ICE Q4 earnings deck)

Although the Exchange segment is no longer the main focus of analysts, it’s a high margin foundational part of the business that is still posting strong volumes despite garnering the “slow growth transaction business” label. In my opinion ICE’s energy assets are an under-appreciated part of the business that could be a material contributor to outperformance in 2021 and the medium-term thereafter.

“FIDS” Segment - Act Two

This segment, until the end of 2020, had been the most closely watched by investors & the Street after ICE’s acquisition of Interactive Data in 2015. The last five years of ICE’s evolution have shifted towards building a recurring, subscription fixed income data business that would grow with electronification of the asset class. In Q4 2020, the segment’s large recurring revenue base grew +6% constant currency, in-line with historical growth rates & management guidance. +5-6% growth is expected in 2021, continuing a stable, reliable trend that formed the core of ICE’s strategy until late last year.

(Source: ICE Q3 2020 Earnings Presentation)

As we’ve seen from fixed income exchanges like MarketAxess & Tradeweb, the bond market still has plenty of opportunities to improve liquidity & access via new technology. ICE owns a slice of the technology that fixed income participants need to comply with regulations, lower costs & become more efficient. Even with new acquisitions changing the focus, data services remains a significant part of ICE’s long-term performance, and I believe reliable growth in this segment will remain strong for the foreseeable future.

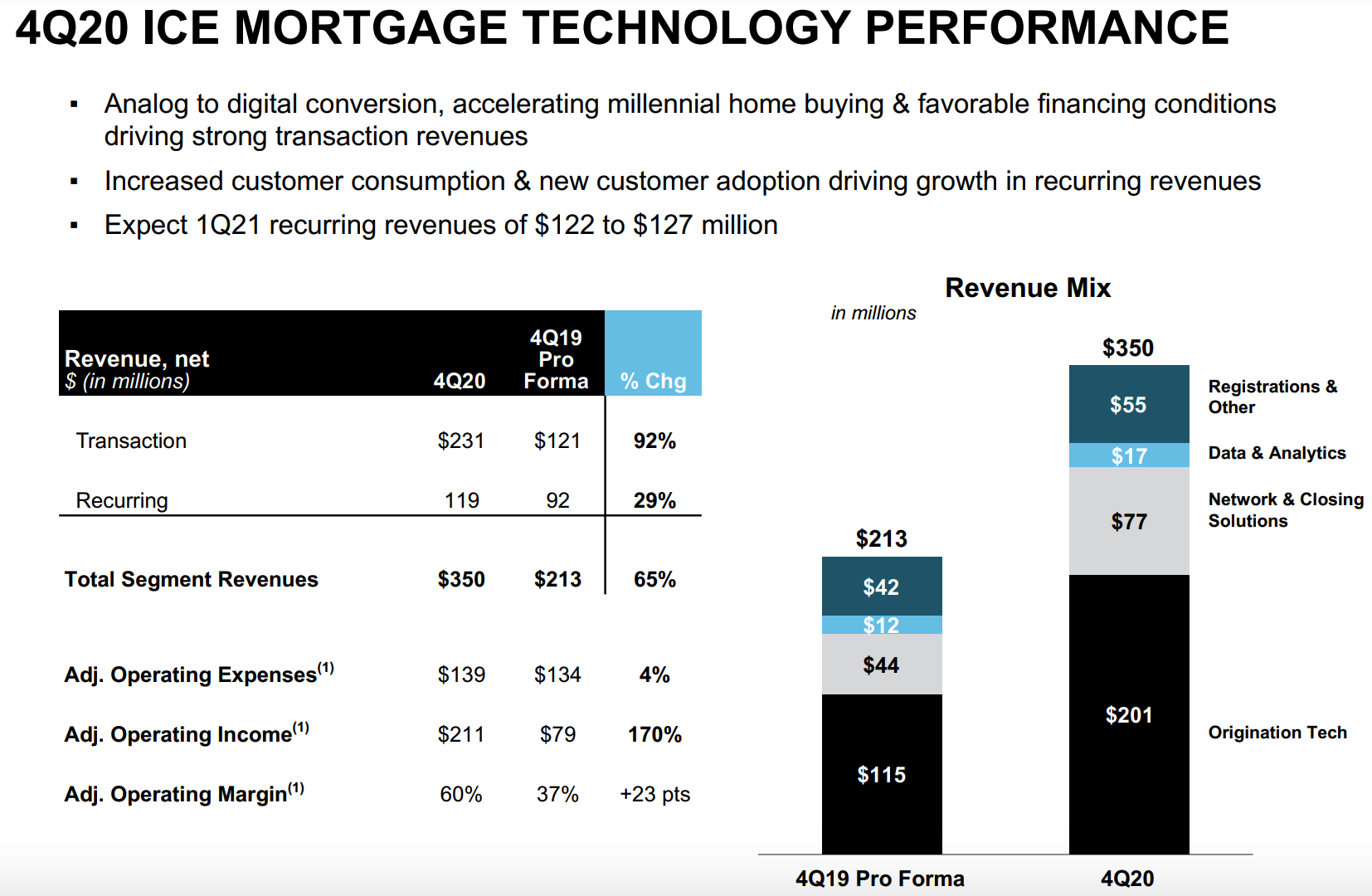

Mortgage Technology - Act Three

When ICE bought Ellie Mae in late 2020, the exchange’s evolution quickly turned to a new market entirely: mortgages. At the time, investors (myself included) viewed the purchase as attractive but expensive - the $11 billion deal is the largest in ICE’s history. Execution (and maybe a bit of luck) was key to the deal showing early returns on investment.

That bit of luck quickly revealed itself in the form of a red-hot housing market. Driven by low interest rates, aggressive fiscal stimulus, and COVID forcing people to work from home, demand for houses has surged to record levels. Redfin recently reported that the market supply of houses reached a new all-time low in the US. Mortgage originations had their best year ever in 2020 - the exact type of activity that makes up Ellie Mae’s bread & butter services. ICE’s origination tech revenue grew a whopping +75% vs. Q4 ‘19 pro forma figures, and the new segment’s transaction business as a whole grew +92%:

(Source: ICE Q4 Earnings Presentation)

Looking forward, even if/when origination activity slows down, there are reasons to be excited about this segment’s growth prospects. ICE management talked about Mortgage Tech’s subscription products that are seeing accelerating adoption by the industry - particularly AIQ, a machine learning tool that helps automate the entire origination process. As the product improves & clients start to see costs come down materially, we should see the segment’s recurring revenue growth accelerate and become a more material part of the business long-term, even when the macro environment becomes a headwind rather than a tailwind.

Overall, I like what I saw from ICE in 2020. The business is enjoying the best of all worlds right now - higher volatility & globalization trends in its Exchange segment, consistent growth in its core data business with a clear path of growth ahead, and phenomenal performance in its newly acquired mortgage business. ICE is my largest exchange holding today & Q4 earnings give me confidence that my investment decision was a good one.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this post, I am long ICE, CME, CBOE, NDAQ and VIRT. I am also long Bitcoin.