How Exchanges Die: The Story Of T.O.M.

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

During my time researching the exchange industry I’ve read many stories that make me think wow, owning & managing an exchange seems so easy.

Invest enough in technology, make sure your biggest clients are happy, and enjoy un-Godly profit margins & near-monopolies in certain markets. Return excess capital to shareholders & close a strategic acquisition here & there, and watch your stock price rise year after year.

Learn the formula, enjoy the rewards. Simple as that, right?

Then I came across a story that made me rethink how difficult it really is to survive & thrive as an exchange, especially an upstart, underdog exchange looking for a seat at the table. The story revolves around a European exchange called The Order Machine, or TOM for short, that launched in summer 2009. By 2016, TOM had amassed 50% market share in Dutch options and growing, boasted powerful owners including Nasdaq, Optiver and ABN AMRO, and was eyeing global expansion. Spectators were calling TOM the victor of a new Battle of the Bund, remembering the dramatic shift of market share in Bund futures from LIFFE to Deutsche Borse. The EU government had given TOM its blessing, allowing it to trade new markets & promote competition on the continent. Everything a winning exchange could want, TOM had.

A year later, TOM was dead. Its biggest customers had jumped ship, revenue had dried up, and investors were withholding further funding. The exchange remains dormant to this day.

How could an exchange with seemingly everything going for it suddenly go bust? How can exchanges & their investors learn from TOM’s death?

Welcome to Amsterdam

Most successful exchanges follow a similar path from startup to rich incumbent - find big trading clients & give them ownership in their company in exchange for order flow. ICE did this with energy futures. Tradeweb did this with US Treasuries & swaps. MEMX is doing this in US equities & MIAX in options.

The Order Machine had this path in its sights when it launched in June 2009, co-owned by HFT firm Optiver & European brokerage BinckBank in a joint venture. TOM’s goal was to break Euronext’s monopoly in Dutch options, the most active options market in Europe with high trading fees & little incentive to innovate. The combination of Optiver’s institutional order flow & BinckBank’s retail client base routed to TOM gave it a real shot to achieve this & make Euronext sweat. Influential bank ABN AMRO bought a 25% stake in the exchange shortly after launch, further elevating its profile & competitive prospects.

To build an initial book of business, TOM used a combination of brokers & market makers to give customers execution at prices formed in Euronext’s more liquid market. If an order was placed on TOM & Euronext was quoting a better price, a broker would buy the Euronext trade and pass it to a market maker, who would then execute the order against TOM’s customer. This tactic, known as “stat trading”, gave TOM the ability to copy Euronext’s prices and compete on an even playing field.

TOM’s growth was further boosted by another classic exchange catalyst - changing regulation in wake of the financial crisis, in this case the advent of Mifid II. Under Mifid II, index products that before were licensed exclusively to one exchange could now be listed freely by multiple venues. TOM used this change to launch options on the AEX Index, a benchmark tracking the top 25 traded Dutch companies previously owned by Euronext, in early 2013. This combination of owner/customer backing, copying Euronext prices, and new products proved highly effective at attracting volume. By early 2013 TOM had amassed nearly 30% market share in Dutch options, and Euronext looked to be slowly losing grip of a market it once dominated.

TOM Gets The Call

So far TOM’s understanding of the exchange success formula had paid off in spades, and global exchange groups were beginning to take notice. US venues looking to establish a foothold in Europe suddenly had a way to pressure Euronext & expand further in a market known for gridlock & fragmentation.

In late 2012, Nasdaq bought a 25% stake in TOM with an option to buy majority ownership at a later date. It also signed on as TOM’s market technology provider, helping it prepare to expand outside of Dutch options. A few months later ICE joined the party with its purchase of Holland Clearing House, TOM’s options clearing solution. The ICE deal is notable in particular as it comes during its blockbuster deal to buy the NYSE and spin out Euronext, the exchange it was now looking to make a move against.

With an influx of investor cash & interest, TOM moved to London and launched markets for European equities & single stock futures in a deeper push on Euronext territory. Its market share in Dutch options now neared 40% as more institutions routed order flow to TOM to capture rebates & improving liquidity.

But Euronext wasn’t about to give up its market without a fight.

Remember those index license changes implemented as part of Mifid II? Turns out the rules were more ambiguous than once thought, as Euronext challenges would soon confirm. In mid 2013 it sued TOM in EU court alleging intellectual property theft of its AEX index, sparking a drawn out legal battle between the two exchanges that would last for years. In the end both parties would claim victory - TOM was ordered to pay Euronext damages for copying many of its products, but was allowed to keep them active. With significantly less resources at its disposal than Euronext, legal settlements would prove to be a heavy blow to TOM’s investment plans & financial situation.

Downfall

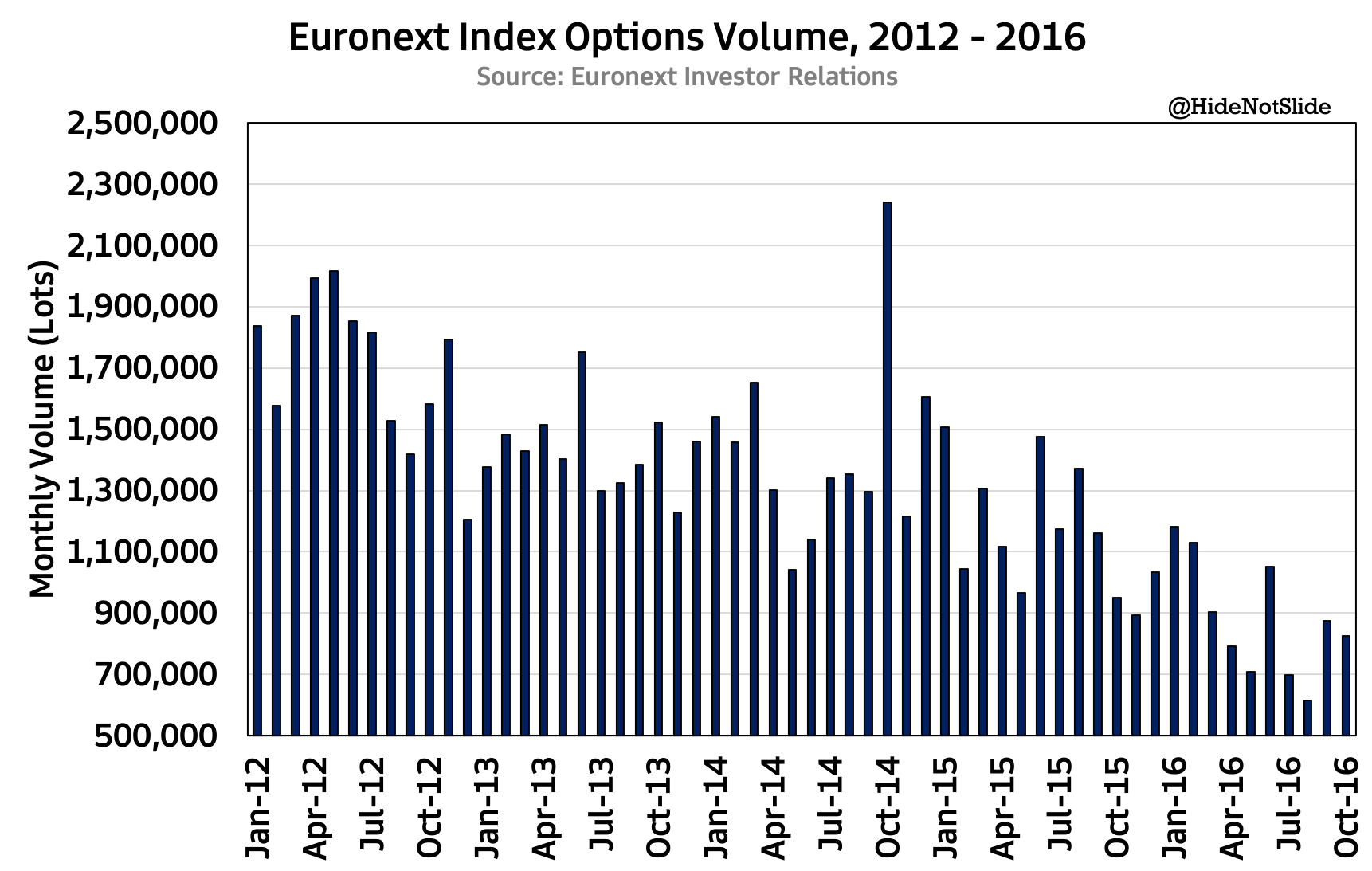

Fast forward to late 2016, and TOM’s Dutch options market share has continued to grow, surpassing 50% of the entire market. Euronext is looking soundly beaten - volumes have hit multi-year lows and its liquidity is dwindling:

(Source)

But in spite of its raging options success, TOM is still unprofitable. High rebates & crippling legal costs have weighed on expenses, and investments outside of options trading are proving difficult. Its equities exchange was accused of catering to HFT latency arbitrage and was shut down. Its futures exchange failed to build liquidity & never attracted material volume. A few firms sending TOM options order flow was one thing, but building a diverse pool of institutional AND commercial customers across asset classes proved much more difficult. TOM couldn’t rise above its ‘one trick pony’ status despite multiple expensive attempts.

Another problem plagued TOM as 2017 began - too many powerful backers with differing visions for the exchange. BinckBank and ABN AMRO wanted lower trading fees for their retail client base. Optiver & fellow HFT owner IMC wanted lower institutional fees for their market making businesses. Nasdaq wanted to expand in Europe & challenge other regional exchanges. Each owner’s influence over TOM’s strategy bred uncertainty among other investors & clouded the exchange’s future. Was TOM really the European disruptor they had envisioned? Would institutions continue sending order flow to the exchange without serious incentives to do so?

In late 2016 TOM’s CEO William Meijer announced he was stepping down as head of the exchange, and rumors surfaced that his replacement would be tasked with selling the company to a willing buyer. The exchange’s owners wanted out, and Nasdaq wasn’t looking to exercise its 51% majority purchase option. Who was left to buy TOM if a deep bench of exchanges & HFT firms didn’t want it?

Amidst mounting skepticism about TOM’s path to profitability & expansion outside of Dutch options, Euronext played its trump card & snuffed any chance that remained of its rival’s survival. It announced a new options rebate program intended to attract ABN AMRO and Binck back to its exchange, capitalizing on their anxiety about TOM’s prospects.

The program worked. ABN AMRO & BinckBank decided to cut their losses and return to Euronext, leaving their former exchange out to dry. Faced with no looming buyers, no money, and its top customers jumping ship, TOM decided to dissolve in mid 2017. Euronext options volumes quickly recovered to pre-TOM highs and have been steady ever since:

Lessons Learned

Alright. We’ve taken some time to stop, bow our heads, and pour one out for The Order Machine. We can’t make the mistake of forgetting stories like TOM’s, lest we repeat its failures and suffer the same fate. What should today’s exchange investors & managers take away from this story?

Profits AND vision matter equally - If an upstart exchange can find a sustainable source of profitability, it will be able to survive regardless of its vision. Think IEX or CBOE here - long term vision can be uncertain for these exchanges at times, but their current business pays the bills, and as long as that’s true these companies have time to figure their strategy out. If profitability is lacking, exchanges need a clear, concrete path to it quickly, or it’s doomed for eventual failure. Upstart equity exchange MEMX is undercutting competitors on price & giving free market data to customers, but its vision to capture enough market share to become profitable is still intact.

TOM found itself with an unprofitable business and no clear path to remedy its cash burn anytime soon. Its impressive growth in Dutch options came through offering deep discounts to its member-owners; if it were to raise prices, customers would likely leave as fast as they came. How else could TOM have gained an advantage? This brings me to point #2:

Competing on price isn’t enough - I think the moment when TOM’s imminent death became clear was when its expansion into adjacent products failed to show returns. Why did TOM’s equities & futures exchanges fail? Couldn’t it entice volume with low trading fees just like options?

It’s important to remember that a customer’s all-in trading costs extend far beyond headline fees. Clearing costs, slippage, regulatory reporting & compliance fees, market data subscriptions, etc all factor into a customer’s decision to choose one exchange over another. My guess is Euronext’s large clients were so integrated with its systems across so many assets that it was prohibitively expensive to choose TOM and sacrifice this integration, even with lower fees in one or two products. Barriers to entry were higher than even TOM could reach.

If after reading TOM’s obituary you still think starting an exchange sounds like an easy path to wealth & success, I genuinely wish you good luck in your attempt.

You’re going to need it.

Honorable Mentions

Another month has come and gone, and that means more volume reports from the major exchanges this week. CME reported a +15% jump in volumes YoY driven by recovery in its top interest rate products and a wild spike in lumber prices benefitting agricultural futures. ICE reported +8% volume growth led by energy futures, particularly its global TTF and JKM natural gas contracts. I continue to be pleasantly surprised by the resilience of ICE’s energy segment given the market’s focus on Ellie Mae & its now sizable portfolio of data businesses. Nasdaq & CBOE added to the industry’s strong showing with nearly +50% growth in US equity options - thanks retail bros!

On the fixed income front, the thrilling market share battle between MarketAxess & Tradeweb continues with another month ending in the underdog’s favor. MarketAxess corporate bond market share has slid nearly every month in 2021 and is now lower than this time last year, while Tradeweb’s share has nearly doubled YoY and is holding steady. I will be bearish on MarketAxess & bullish on Tradeweb until this trend reverses itself or a bigger (ie macro) catalyst emerges.

Nasdaq announced the acquisition of climate change marketplace Puro.earth this week for an undisclosed sum. Puro helps match companies looking to reduce their carbon footprint (carbon “sellers”) with companies that can store, minimize & eliminate CO2 emissions (carbon “buyers”) - clients include Microsoft, Shopify & other ESG-focused corporations.

Chart of the Week

Miami - the new Silicon Valley, the new Hollywood, the new… Wall Street? Miami Exchange has been relentlessly taking options market share since COVID began in early 2020, growing from less than 9% of the market to nearly 15% today.

MIAX has famously used equity rights programs to give ownership in its exchange to customers when they hit certain volume targets. With each new target hit, MIAX equity becomes more valuable, giving program participants more incentive to cooperate & creating a vicious cycle of market share gains. If the trend continues, more options may trade in Miami than the New York Stock Exchange sooner rather than later…

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, COIN and VIRT. I am also long Bitcoin and Uniswap’s UNI governance token.