Exchange Earnings Season Begins

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

News

The earnings blitz begins! The first batch of exchange & market data companies reported fourth quarter earnings this week, giving us a good idea of how the industry as a whole is likely to fare. Results look promising so far - my stock-specific takes below:

Nasdaq Reports Fourth Quarter and Full Year 2021 Results; Delivers Strong Growth in Revenue and EPS: Q4 2021 proved that the Goldilocks scenario continues to hold for Nasdaq as it has for nearly all of the post-COVID era. Market volatility & record options activity continues to favor Nasdaq’s exchange businesses. The company ended 2021 with a three year win streak vs. the NYSE in IPOs and stellar +25% growth in Listings revenue. SaaS products now make up 1/3rd of Nasdaq’s recurring revenue base, putting it on track to achieve its goal of 40-50% SaaS mix by 2025. If investors were wondering why Nasdaq crushed the S&P in 2021 with a +58% return, this quarter helped explain why.

I remain a Nasdaq bull heading into 2022 with some themes from this week’s earnings call supporting my view. I think the exchange’s cloud deal with Amazon gives it a first-mover advantage in a new era of market technology, which management hinted may become a significant source of not just expense savings, but new revenue over time. I’m encouraged by Nasdaq’s modest expense guidance this year & believe the themes that have supported it the past two years, while potentially due for a slowdown, have not yet run out of steam. Strong volumes combined with favorable growth trends in high margin business units give me confidence to keep Nasdaq a material part of my portfolio.

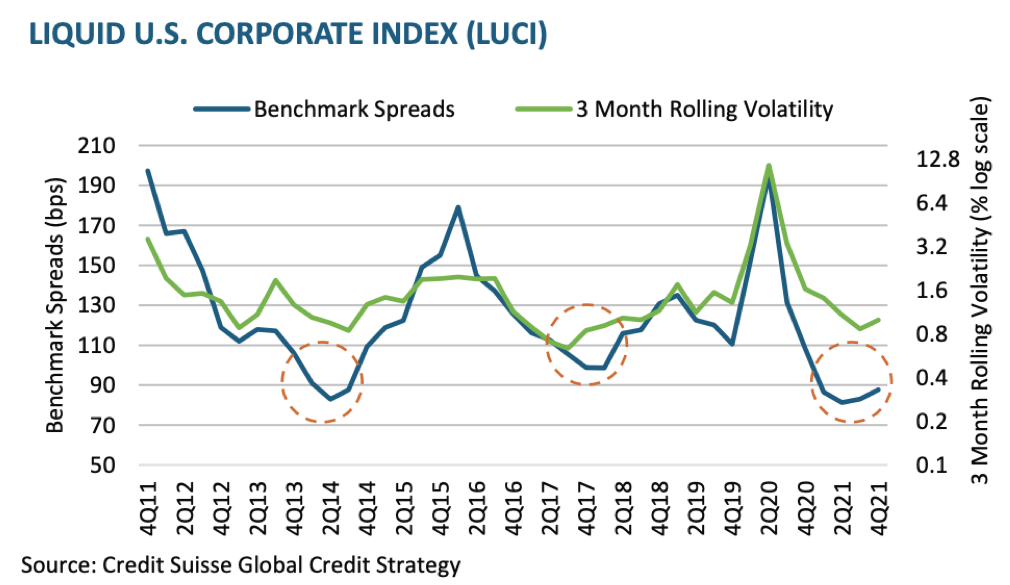

MarketAxess Reports Fourth Quarter 2021 Results: Fourth quarter earnings closed the book on a rather dismal 2021 for MarketAxess shareholders. Revenues ended the year more or less flat YoY, margins shrank as investments took their tole on expense growth, and EPS dropped -14% from 2020 levels. MarketAxess thrives on volatility in a narrow range of metrics that may have been the only non-volatile metrics in the entire market - corporate bond credit spreads. That, combined with poor market share gains compared to its rival Tradeweb, made the stock one of the worst performers in the entire exchange industry last year.

Going forward, the outlook still looks precarious for the stock in 2022, but some silver linings are beginning to shine through. First, MarketAxess suffered a brutal -28% drop in 2021 which brings its price & valuation back to pre-COVID levels. Investors that were valuing the company as if it would capture 100% of the electronic corporate bond market fairly quickly seem to have sold, taking some risk out of the stock at current prices. Second, MarketAxess has kept investment in the business its #1 priority over outsized buybacks or dividends, giving them a higher chance to capture more market share in EM credit & their core US corporate business over time. Third, given increasingly hawkish Fed language & stubborn inflation data, we could easily see credit spread volatility return in 2022 and beyond, giving a boost to MarketAxess volumes regardless of market share. While valuations are still high at a ~40x-50x forward multiple, the risk/reward is starting to favor buyers at today’s prices. I remain on the MKTX sidelines but am considering a long position if the stock keeps dropping in the first half of this year.

MSCI Reports Financial Results for Fourth Quarter and Full Year 2021: Since the late 2010s nearly every quarter has felt the same for MSCI’s core index business. More end users demand investment products that leverage MSCI’s indices, driving AUM and related subscription fees up. The infrastructure surrounding ESG continues to broaden & become more robust, making MSCI’s market leading position in ESG even more apparent. Revenue grows double digits. EPS grows double digits. Guidance remains positive. Quarter after quarter after quarter after quarter. Q4 2021 was no different - revenue grew +20% organically YoY driven by standout performance in variable asset-based fees & recurring subscription revenues in its ESG & Climate segment. This relentless growth streak pushed MSCI’s multiple to hyper-growth stock levels which have since come down significantly YTD:

Does this drop present a buying opportunity? There is no argument about MSCI’s incredible pricing power in the index & ESG business. If global demand for these kinds of products remains strong, MSCI will directly benefit & continue to put up world-beating growth figures. However, even after its recent drop, I believe MSCI’s valuation already prices in much of this view. I recently bought shares of MSCI’s rival, S&P Global, because I think its valuation is more tolerable & its business more diversified. MSCI is a great business trading at too high a price for my taste, keeping me on the sidelines for now.

If you like this free newsletter I invite you to subscribe to Front Month Premium where I post more high quality exchange & market structure research each month. The premium archive now has 18 articles on topics like FTX, Robinhood, Citadel Securities & more that instantly become available to paid subscribers.

Thank you for your support!

Other Stories I’m Reading

Faces are red at Refinitiv as figures prove far from definitive

LME's outgoing boss Matt Chamberlain takes CEO role at Komainu

Why the Sustainable Investment Craze Is Flawed

Kaiko and ICE partner on crypto data

Crypto exchange FTX US valued at $8 billion as first fundraise draws SoftBank, Temasek

Chart Of The Week

I bring this fact up from time to time because it’s such an impressive statistic - nearly every exchange stock has outperformed the S&P 500 since inception, and most of them outperform the market most years. Monopolistic business models, consistent pricing power & favorable macro trends have a way of showing up in stock performance.

With this stat in mind, we’re left to assess the surprising underperformance of exchange stocks so far in 2022. Only two related companies - CME Group and Virtu Financial - have outperformed the S&P in 2022, with the rest lagging by a wide margin.

If I had to guess, I’d say this underperformance is likely due to two factors: general mean-reversion after most exchanges crushed the S&P in 2021, and some potential concerns around the impact of inflation on companies with high subscription revenue mix. I personally have been using this as a buying opportunity for high quality names like S&P Global and Nasdaq. Market volatility has remained alive & well so far this year with global energy, equity & option volumes remaining quite strong. I think exchanges are likely to recoup relative performance in the coming months as Fed hawkishness & geopolitical uncertainty keep the exchange money printer running.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ, SPGI and VIRT. I am also long Solana.