Exchange Bears Are People Too

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

Being bearish is no fun these days.

With Jerome Powell at the Fed and stimmy checks coming in the mail every few months, we all know stocks only go up. Anyone who says otherwise should just have fun staying poor, right? Who needs bears in their life?

Jokes aside, understanding a stock’s bear case is a key part of the due diligence process, even if you own the stock & have confidence it will outperform the market. If investors aren’t sure what would cause the stocks they own to go down, they arguably don’t understand their positions well enough & won’t know what to do when sell-offs do happen.

I want to take some time to outline the top bear catalysts for the exchange industry as a whole, then go through the unique bear case for each stock in the sector. Putting on the bear hat for just a week or two should help us weather periods of volatility & separate story-changing news from noise.

Let’s dive in:

Industry-Wide Bear Catalysts

Operational Failure - Exchanges have collected an incredible amount of power & profitability since the ‘08 financial crisis as regulations push influence away from big banks directly into the hands of exchanges & their partners. With this power comes immense public trust that the operations of an exchange are able to handle the trillions of dollars that run through their platforms. If an exchange experiences a systems glitch or a technological failure, it quickly & directly brings public outrage & financial harm.

There are plenty of examples of this catalyst occurring in the past - the most high profile of which was the 2012 Knight Capital glitch that quite literally destroyed the firm. On August 1, 2012, a software update to the market-maker’s order routing system wasn’t installed properly, and when released into production caused Knight’s trading algorithms to malfunction. The company lost $440 million before the algorithm was turned off & fixed, nearly double its normal quarterly revenue. Knight’s stock dropped 70% in a day and the company was acquired by Getco later that year. While an extreme example of operational failure, events like this are possible & highlight the paramount importance of investment in an exchange’s technology & operations. The threat of cyberattacks & customer clearing defaults would also fall into this category.

Regulation - While some regulatory changes have helped exchanges in the past, the threat of increased oversight & regulatory burden has always clouded the sector’s prospects. Bear catalysts in this area can show up on multiple fronts - be it pressure on market data pricing by the SEC, antitrust suits blocking future M&A, and even some form of a financial transaction tax. These pressures have the same net effect on exchanges: lower margins, slower future growth, and constrained strategies giving way to complacency. These threats are very real as evidenced by the industry’s coordinated response to fight certain regulatory threats. The industry went so far as to form a coalition to lobby Congress as a combined force & make plans to move operations out of states if new taxes are introduced.

Unfortunately new regulations are a near-certainty with a new US administration taking the reins and looking to make its mark on Wall Street. Incoming SEC Chairman Gary Gensler was head of the CFTC following the financial crisis, overseeing sweeping changes to regulation of the futures & swaps markets during his tenure. A similar sweeping agenda is likely in store for the equity markets with Gensler as head of the SEC.

Whether regulatory changes will be all bad for exchange performance remains to be seen. Exchanges & trading firms have found ways to adapt & even take advantage of new regulations in the past - I don’t think this time will be any different.

Stock-Specific Bear Catalysts

CBOE - As chronicled in my recent review of Q4 earnings, the CBOE bear case is in my opinion the closest to reality of all the exchanges. Skepticism & worry can be spread across multiple core segments, including derivatives, cash equities & Europe.

While CBOE’s VIX futures and Index Options businesses don’t have direct competitors, they are highly saturated & exposed to the market’s appetite for volatility. The bear case here would be more VIX blowups that cause large volatility ETP outflows as traders get shaken out of their positions. We saw this bear case play out in early 2018 when the VIX doubled in one trading session and VIX futures open interest crashed in the following days & weeks:

(Source)

As we all can see from the constant barrage of chaotic headlines, it’s pretty likely the VIX could spike dramatically in the future & remain elevated for a considerable period of time. If this happens, CBOE’s derivatives business will continue to struggle.

Bearishness remains when moving to CBOE’s equities business, where competition from all sides is squeezing margins and market share. CBOE’s equities RPC is down nearly 40% since early 2018 as new exchanges like MEMX and MIAX enter the market & undercut legacy players on pricing, along with the ever-growing impact of off-exchange trading. Yes, industry volumes have been way higher across the board since March 2020, but those higher volumes haven’t proportionally flowed to the bottom line in CBOE’s case. It’s difficult to see a future where market share rebounds significantly when looking at the current number of competitors vying for the same volume.

CME - Accepting CME’s bear case means holding three beliefs:

Interest rates are not going up for the foreseeable future

New products won’t contribute to future growth

Competitors will take market share

The most obvious of these is the assumption that interest rate volatility remains permanently damaged by the Federal Reserve’s agenda. Interest rate products make up close to a third of total revenue & have historically seen higher demand when interest rates are moving up & the yield curve is steepening. If the US economy can’t stomach higher rates the way they used to, core demand for hedging rate exposure may be irreversibly impaired. CME will have a tough time growing earnings if interest rate products don’t contribute to at least some future growth.

Which brings me to point #2 - how can CME grow if rates volatility remains low for the foreseeable future? One way is new products - crypto futures, micro e-mini products & SOFR futures come to mind as examples. In each case, new product launches come with the challenge of tailoring the product to the correct audience from day one, beating out competition, and convincing customers to build liquidity over time. New futures products are hard to get right - most launches fail to attract enough volume to impact profitability. If new products don’t fuel most of CME’s growth in the medium to long term, it's likely the company won’t outperform its peers or the broader market.

Finally, competition in CME’s markets is heating up & there is a serious chance that the exchange loses market share in key asset classes. CME’s energy business faces direct pressure from ICE in both oil & natural gas, and ICE has found itself better positioned for a globalized energy market as LNG demand rises. Even in interest rates, recently integrated BrokerTec faces renewed threat from Tradeweb, who just purchased rival platform eSpeed with plans to challenge CME in dealer-to-dealer US Treasuries. Even if CME fends off competition on multiple fronts, a bearish outcome of such a battle would be lower prices & squeezed margins.

ICE - The bear case for ICE is a story not of implosion but of stagnation. The exchange went on a transformational shopping spree in the 2010s, as it swallowed the NYSE in 2013, Interactive Data in 2015, and Ellie Mae in 2020. In each case ICE stressed these assets would grow faster under its leadership than they would as a standalone company, justifying a premium purchase price.

ICE would enter a bearish scenario if this assertion ceases to show up in reality - a competitive equity market erodes NYSE’s market share, IDC’s fixed income data business reaches maturity, and a sustained housing downturn slows adoption of Ellie Mae’s automation tools. If core acquisitions aren’t the growth engine of the company, how can spending a combined ~$25 billion of investor cash be justified?

There’s also the executive bench to consider. ICE founder & CEO Jeff Sprecher has led the company for over 20 years & turned a small power trading program into a global exchange powerhouse, making investors rich along the way. Sprecher is reaching retirement age, and long-time colleagues like former COO Chuck Vice & general counsel Jonathan Short are beginning to step away from the company. When the time comes, will Sprecher’s successor be able to pick up where he left off? Sprecher has been referred to as the Steve Jobs of the exchange industry - does ICE have a Tim Cook waiting in the wings to organize & optimize the vision Sprecher has built?

MarketAxess - A clear story underpins MarketAxess’s premium valuation - legacy banks & broker dealers used to own all trading in the corporate bond market. Market share is rapidly moving away from the dealers to MarketAxess’s electronic platform as trading costs come down. The stock trades under the assumption that 1) corporate bond trading will become 100% electronic at some point in the future and 2) MarketAxess will own a large percentage of this electronic market.

What if those assumptions don’t come true?

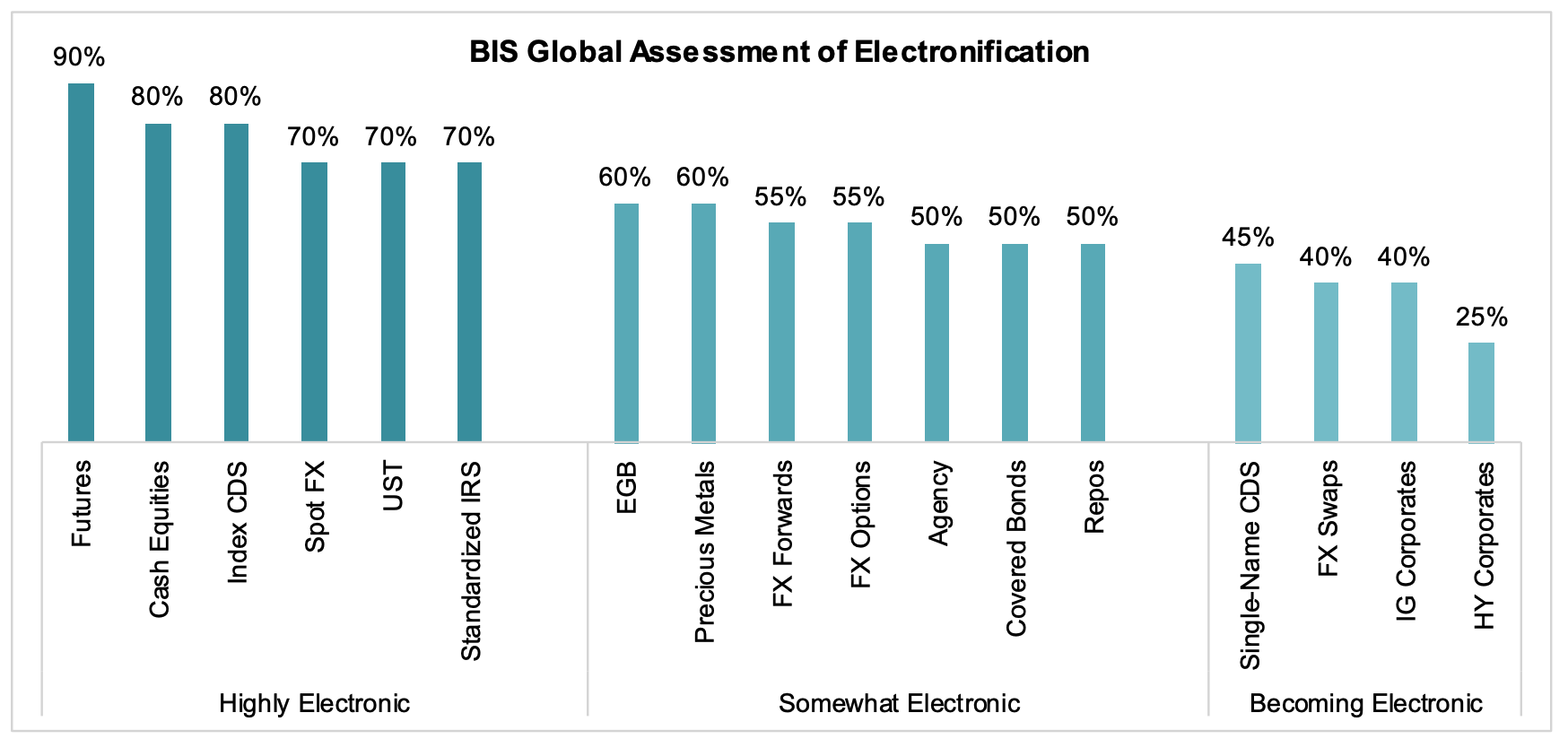

Sure, most of the corporate bond market will likely move away from the legacy dealers & go electronic, in line with other markets. But even the most mature asset classes (like futures & cash equities) aren’t completely electronic, leaving some space for dealers to keep permanent market share:

(Source)

What will the natural, steady-state electronic share of corporate bonds be? 90%? 80%? Something less than that? The MarketAxess TAM is highly dependent on this percentage.

If dealers are able to keep a larger share of the corporate bond market for longer than investors may be expecting, MarketAxess’s growth trajectory won’t be what its valuation implies. This threat isn’t entirely out of the question - because fixed income trading is less liquid & more complex than equities trading, a relatively large human component may always be needed.

Tradeweb - There are two primary bear cases for Tradeweb, and they both have to do with competition. In most of Tradeweb’s primary markets they face stiff competition from another high-profile financial behemoth - Bloomberg. Tradeweb President Billy Hult described their relationship with Bloomberg well during Q4 earnings:

“We grew up essentially from day 1 competing with Bloomberg, whether or not that was U.S. government bonds, European government bonds, global swaps. It's been kind of us and Bloomberg kind of shoulder to shoulder together for a long time. So we know the company well, healthy, obviously, healthy respect.”

(Source)

The market where competition between Tradeweb & Bloomberg is most intense is dealer-to-client (D2C) US Treasuries, where each company has an equal share of electronic trading in a part of the market where electronification still has room to grow:

(Source)

Tradeweb has been able to defend and grow market share up to this point, but future success is by no means a certainty. Bloomberg is much larger than Tradeweb & can leverage its dominant Terminal client network to facilitate trades & attract clients.

Another piece of the bear case has to do with Tradeweb’s stakeholders. Multiple banks including Citigroup, Barclays, Credit Suisse, Goldman Sachs & JP Morgan own a large percentage of Tradeweb stock, and also account for a significant part of the company’s revenue. If these primary dealers were to sell down their equity stakes materially, they may no longer have an incentive to trade with Tradeweb over competitors like Bloomberg. Tradeweb itself highlights this risk in its annual filings:

In addition, it is possible that the pre-IPO Bank Stockholders and their affiliates may reduce their use of our trading platforms or their engagement with us in the future due to reductions in the level of their equity ownership following any completed or future offering.

(Source)

Virtu - Of all the companies on this list, equity market volatility is the most intertwined with Virtu’s performance & corresponding bear case. When bouts of chaos in stocks are intense & frequent, Virtu enjoys other-worldly success like we saw throughout 2020. The flip side is also true - a prolonged drought of volatility would leave little opportunity for Virtu to impress investors. Sure, spreads are wide enough today for the market-maker to fund operations & pay a modest dividend, but that’s not enough to beat the market consistently. No one can predict if or when volatility will occur, and that lack of visibility contributes to a bearish or at least non-bullish view of the stock.

Unfortunately, investors & governments are beginning to view the stock market less as a free-floating venue for raising capital & more as a defined retirement benefit tool.

Stocks are going up in a slow, consistent fashion with little chaos? Good.

Stocks are whipsawing around & depriving retirees of the returns they need? Unacceptable.

To the extent monetary & fiscal policy forces markets perform one way or another, Virtu’s ability to profit off future volatility may become muzzled.

Honorable Mentions

CME launched Ethereum futures on February 8th amid new record highs for Bitcoin & Ethereum. Tim McCourt, Global Head of Equity Products at CME, did a worthwhile interview with The Block on CME’s journey to launch an ETH futures product - you can find that interview here.

NYSE President Stacey Cunningham warned the exchange may exit New York if a transaction tax is imposed, and Virtu CEO Doug Cifu echoed this sentiment during Q4 earnings:

“I will tell you that the notion of a transaction tax in New York is, I'll use the word foolish because I know what we would do. I would shut this office and we have an office now in Short Hills, New Jersey, and we have an office in Florida, and we would just leave the state of New York. We would never pay a penny of the New York State transaction tax. And Stacey Cunningham, God bless her, said the same thing. She may just move the New York Stock Exchange.”

Chart Of The Week

Exchange earnings season is coming to a close as quickly as it began, leaving plenty for investors to process. With two companies left to report, the exchange & market data industry looks to have thrived in Q4. Consolidated revenue & EPS grew double digits led by companies more exposed to market volatility - MarketAxess, Tradeweb & Virtu as examples. Multiple companies also announced dividend increases & new buyback programs on the back of good results.

CME is notably the only exchange so far with shrinking EPS YoY - they haven’t done significant M&A recently and their top interest rates products struggled in Q4. CBOE barely escapes the shrinking EPS club with flat growth YoY helped by M&A.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Bitcoin.