Coinbase Wants To Get Cloudy

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

News

Inside Coinbase’s Budding Plan To Become The AWS Of Crypto: A thought-provoking article came out of Forbes this week reviewing Coinbase’s cloud infrastructure business & their vision of “becoming the AWS of crypto”. The piece, and Coinbase by extension, argues that the company’s acquisition of Bison Trails combined with its unique crypto expertise & massive user base will help it beat competing providers, diversify revenue & achieve AWS-like status.

Does this argument have merit? Let’s orient ourselves around what Coinbase Cloud is today. Coinbase purchased Bison Trails in February 2021 for an estimated $80 million in stock and rebranded the business as Coinbase Cloud. You can find this segment’s revenue lumped into the “Other subscription and services revenue” line in their financials:

The unit is small relative to Coinbase’s retail transaction business, but it’s less tied to market volatility & more towards growing developer interest & adoption of crypto technology. If a customer wanted to spin up a new node for a certain blockchain, for example, they could pay Coinbase Cloud to launch & manage this node without having to master the complex tech themselves. Coinbase Cloud also offers advanced & easy to use blockchain data tools to help institutions & developers monitor transactions & build applications.

While I do think the future of this business is bright, I’m not betting on Coinbase Cloud becoming the next AWS. Regardless of the future market size of blockchain infrastructure tech, competition from both web3 and web2 companies in this arena is already quite intense. Companies like Bitfury, Consensys & Alchemy have already made significant inroads in the platform-as-a-service space for blockchain developers & are larger than Coinbase Cloud is today. Forbes highlighted Alchemy in particular as a formidable competitor with most major blockchain applications, like OpenSea & Axie Infinity, as customers. How will Coinbase Cloud differentiate & take market share from these more established players?

This doesn’t even consider the idea that AWS still has a chance to become the AWS of crypto. My guess is it will be a much smoother transition for Amazon to build blockchain expertise & take on web3 providers than the other way around. All it takes is a morning Amazon crypto press release for blockchain tech to shake in their boots the same way every other industry reacts when the Big Tech giant looks their way.

I still think Coinbase can slowly build a diversified crypto business to please shareholders, but I want to temper any “AWS of crypto” expectations this Forbes piece may create. I will keep watching Coinbase’s stock from the sidelines for now.

ICE Announces Senior Leadership Changes: An important but rather cryptic press release came out of ICE this week that merits a deeper dive. ICE made a number of executive shuffles across the company as it re-positions certain roles around ESG, evolving technology needs & a growing employee base in the wake of Ellie Mae integration. Here are the main highlights:

Lynn Martin, currently head of ICE’s Fixed Income & Data Services business, will take over as President of the NYSE, replacing Stacey Cunningham after three years in the role.

Former CFTC Commissioner Sharon Bowen is taking over as Chair of the NYSE as CEO Jeff Sprecher steps back from the role.

NYSE’s Head of Capital Markets Amanda Hindlian will replace Lynn Martin as head of ICE’s FIDS business.

COO Mark Wassersug will move to the CIO spot & ICE Futures Europe president Stuart Williams will take his place.

These moves have some intriguing implications. First, I don’t think it’s a coincidence that Cunningham’s stepping down from the NYSE comes on the heels of a WSJ article celebrating Nasdaq’s three year IPO win streak. Blame COVID’s trading floor shutdown, blame Nasdaq’s pivot to ESG, blame tech sector strength, but the truth remains that Nasdaq is enjoying its best IPO season since the Tech Bubble period of the late 1990s. Perhaps incoming President Lynn Martin can reverse the losing trend.

Second, CEO Jeff Sprecher is stepping back from more and more roles in what seems like a slow preparation for the founder’s retirement. However, Sprecher made it clear in his public note to employees that “he’s not going anywhere”:

“As organizations everywhere adjust to a world transformed by the pandemic, our management team is evolving along with the market environment. I’m not going anywhere, but for many years, we’ve been working to develop the next generation of ICE leaders who’ll bring energy and experience to drive our success in the future. Challenging this group of global leaders with new or expanded roles is fundamental to good governance and stewardship of our firm.”

(Source)

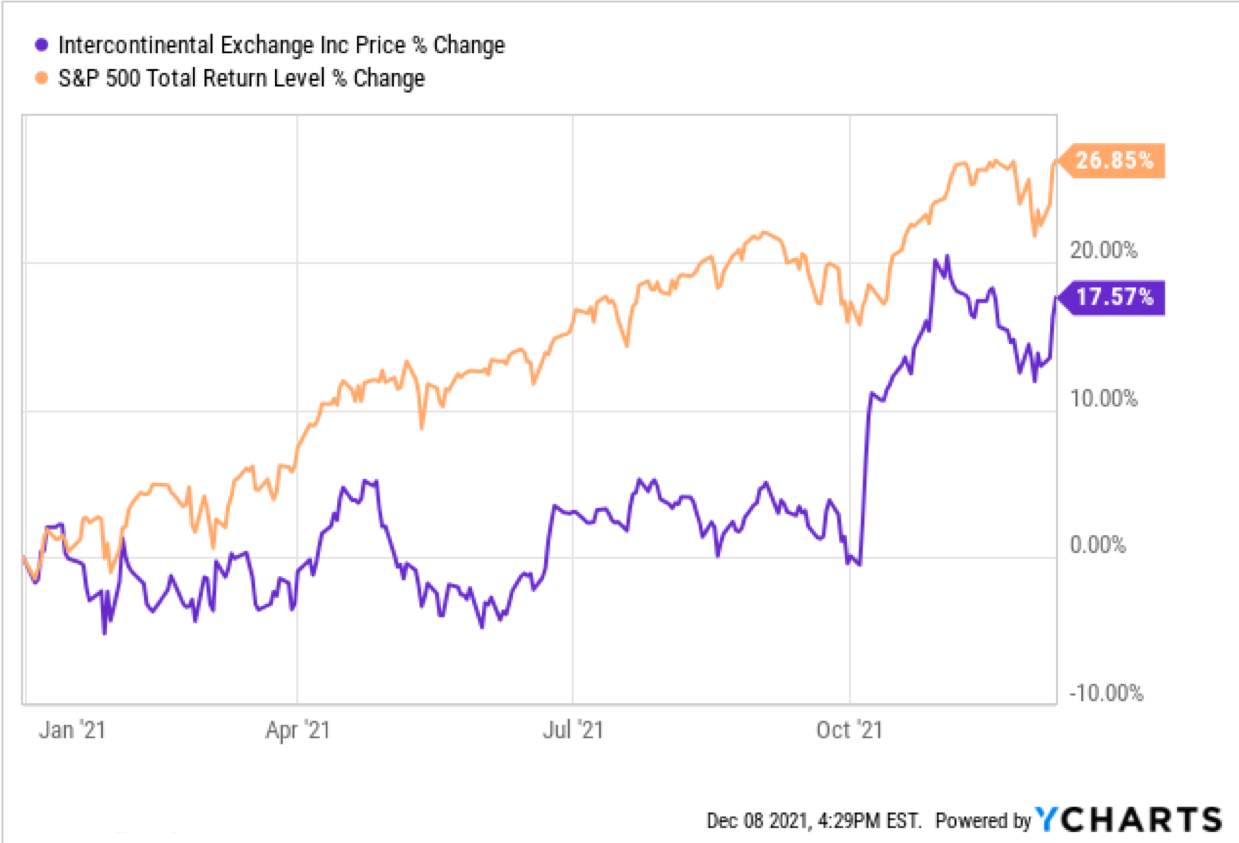

Has ICE evolved to the point where its stock will be unfazed by Sprecher’s eventual departure? Shares are near an all-time high but have still lagged the broader averages YTD:

My latest paid post is live - The Death Of Citadel is the first of a two-part series that explores the birth, near-death experience and ultimate dominance of Ken Griffin’s hedge fund/market maker conglomerate. Subscribers get immediate access to this post & a deep archive of past market structure research.

Thank you for your support!

Other Stories I’m Reading

Investors Are Using Robinhood, Other Platforms to Jump Into Options Trades, Worrying U.S. Regulators

CME Group Announces Launch of Micro Ether Futures

Flow Traders Takes a New Market Position As An Active Liquidity Provider on MarketAxess

The next quant revolution: shaking up the corporate bond market

Six cryptocurrency CEOs testify before Congress

Enabling Algo Research on Blockchain Data

Chart of the Week

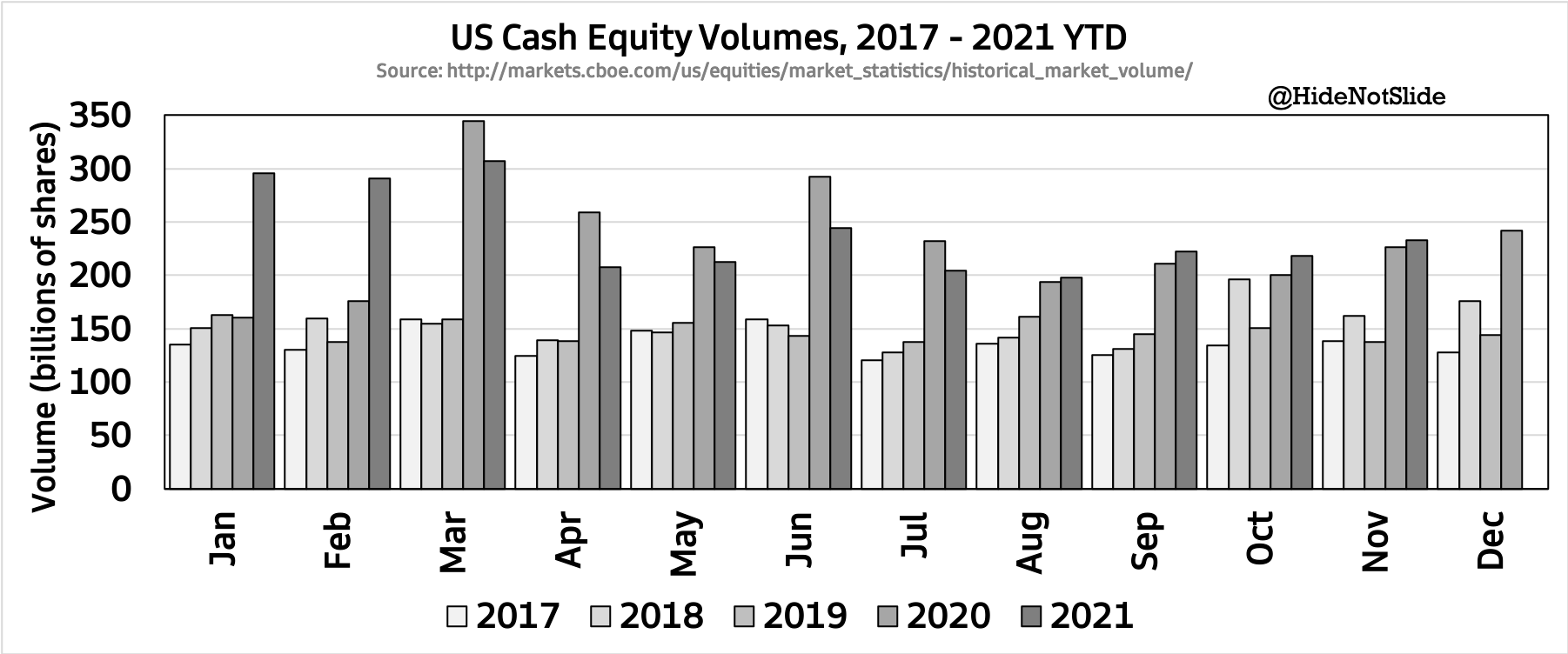

The US equity market finds itself in a narrative tongue-twister as it rapidly closes out 2021. Comparisons against the craziest year in the history of markets, changing on/off-exchange dynamics & new entrants make it hard to keep the landscape straight. Let’s look at a couple charts that should help paint a clean picture.

First, 2021 US equity industry volumes have remained extremely elevated relative to pre-COVID levels. Q3 and Q4 2021 have even seen growth vs. 2020 and have come nowhere close to “normalizing” like some predicted would occur. Exchanges may report “declining” FY equity volumes vs. 2020, but this is a technicality & takes focus away from the good times they’ve enjoyed longer than anyone has expected.

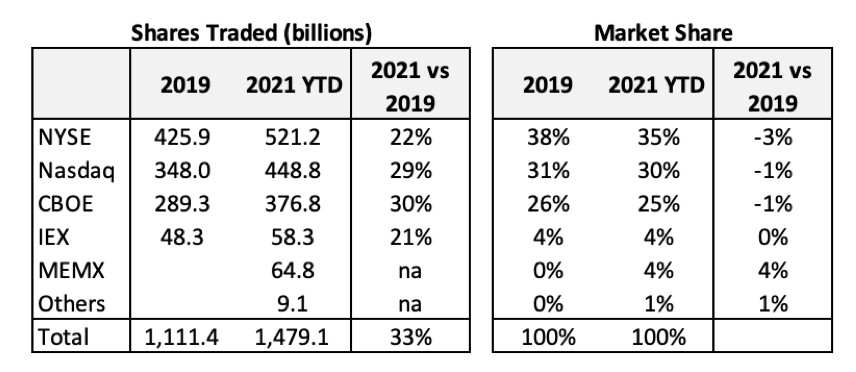

That clears up the volume story a bit - what about the market share story? The below table tracks on-exchange volumes only and excludes the off-exchange world for simplicity. On-exchange volumes have grown a whopping +33% vs. 2019 levels with broad-based growth across competing venues. On-exchange market share gives us an interesting bit of info - new exchange entrants like MEMX & MIAX have gained ~5 percentage points of market share at the expense of predominantly the NYSE. IEX has weathered the threat from new challengers well despite the lowest amount of volume growth vs. 2019:

Despite what management teams or critics may tell you during upcoming earnings season, the data is clear - it’s a great time to be a US equity exchange in the post-COVID era!

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Solana.