Celebrating Rivalry Week On Wall Street

Celebrating Rivalry Week On Wall Street

Plus: BlackRock's west coast purchase, Bitcoin's blowout, and more

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

It’s Not Personal - It’s Just Business

(Source)

Red Sox - Yankees.

Ohio State - Michigan.

Barcelona - Real Madrid.

Sports fans love a good rivalry. Some feuds have been building for over a century. Others rise and fall with the growth of a team’s supporting fanbase & the success of their players.

Business rivalries are just as intense. Not only do employees treat a company like their team at times, but jobs and livelihoods can be at stake when firms face off. Exchanges are no different. Due to the deep histories of most exchanges & recent consolidation, old rivals are finding themselves pitted against each other in new ways.

This week I’m taking a look at the deepest, most intense rivalries in the exchange space, examining the stories that made the competition what it is today.

NYSE vs. Nasdaq - A Flashy New York Knife Fight

There isn’t an industry rivalry more well-known than that of the only two listings giants in the US - Nasdaq vs. the New York Stock Exchange. The two exchanges compete head-to-head in almost every way - cash equities & options trading, market data sales, and most notably, listings.

The NYSE consistently touts their IPO dominance when measured by money raised; Nasdaq is quick to point out their lead in number of IPOs given their less restrictive listing standards and a more tech-focused company base. When comparing their listings businesses by net revenue, the NYSE takes the lead with ~$450 million annually vs Nasdaq’s ~$300 million.

The Financial Times wrote a piece in late 2019 detailing the “knife fight” between the two exchanges to attract big-name IPOs to their podium. The firms compete fiercely over each new company thinking about going public, including big advertising budgets, access to exchange office space for board meetings, and “months, if not years” of negotiating. A recent win for Nasdaq? Airbnb:

Europe - M&A Musical Chairs

Europe’s exchanges share a long, interweaving history of consolidation & expansion as capital markets have evolved from the 1980s to today. A scattered field of ~30 independent exchanges in 2000 have morphed into a handful of exchange mega groups; those left have tried to merge even further. LSE has been involved in most of them, including three separate failed attempts to merge with Deutsche Börse, hostile takeover bids by Nasdaq & Hong Kong Exchange, and even a failed merger with TMX Group. Assets have been bought & sold to each other as strategies change and to satisfy regulators - the most recent example being LSE’s sale of Borsa Italiana to Euronext as it prepares to swallow Refinitiv.

One exchange serves as the epitome of Europe’s rivalries expressed through M&A - LIFFE, the London interest rate derivatives platform. Before LIFFE even began its journey under multiple exchange owners, they first found themselves on the losing side of a protracted market share battle with Deutsche Börse over their Euro-Bund contract. DB1 was able to wrestle away LIFFE’s top market by embracing electronic trading early, winning over German banks, and pushing for open access to let foreign investors trade with ease on their exchange. The public loss was a hard setback for LIFFE, but they were able to rebound by launching their own electronic platform, called LIFFE Connect, in 1998.

Nevertheless, the exchange’s leadership struggled with limited growth prospects, and in 2001 LIFFE put itself up for sale. Multiple bidders immediately emerged with strong interest in the platform, including LSE, Deutsche Börse and newly formed Euronext. Right away LSE was seen as the auction’s front-runner - besides having the high bid, LSE’s offices were a stone’s throw away from LIFFE’s and both exchanges shared the same clearinghouse, traded in the same currency and operated under the same regulator. The tie-up looked attractive and would have helped LSE diversify away from its core equities business & stave off even more potential takeover bids.

In the end, LIFFE shareholders chose to be bought by Euronext. Despite a lower offer, Euronext’s deal was all-cash, and LIFFE leadership thought their business would expand faster with pan-European ownership than with its London neighbor.

The news was a surprising blow not just to LSE but Great Britain as a whole. Exchanges serve as a symbol of national pride, and for a French company to own a prized British asset added insult to injury.

LIFFE’s story doesn’t end with Euronext. in 2006, the NYSE announced its purchase of Euronext, putting LIFFE under new American leadership. in 2013, ICE bought the NYSE, spun off Euronext, and kept LIFFE for itself. The irony of LIFFE’s saga comes when realizing that despite the jostling between firms to win the LIFFE auction in 2001, not one of the competing firms owns the asset today.

CME vs. CBOT - Chicago’s Oldest Rivalry That Ended With A Bang

Chicago has long been a city known for its exchange competition, with roots stretching back to the 1800s formation of the Board of Trade and the early 1900s birth of the Mercantile Exchange.

Despite being located less than a mile from each other, the two exchanges rarely competed directly. CBOT first made its name in the corn & wheat markets, and later with the wildly successful launch of US Treasury futures. CME grew from butter and eggs, to pork bellies, later to Eurodollars and S&P 500 futures.

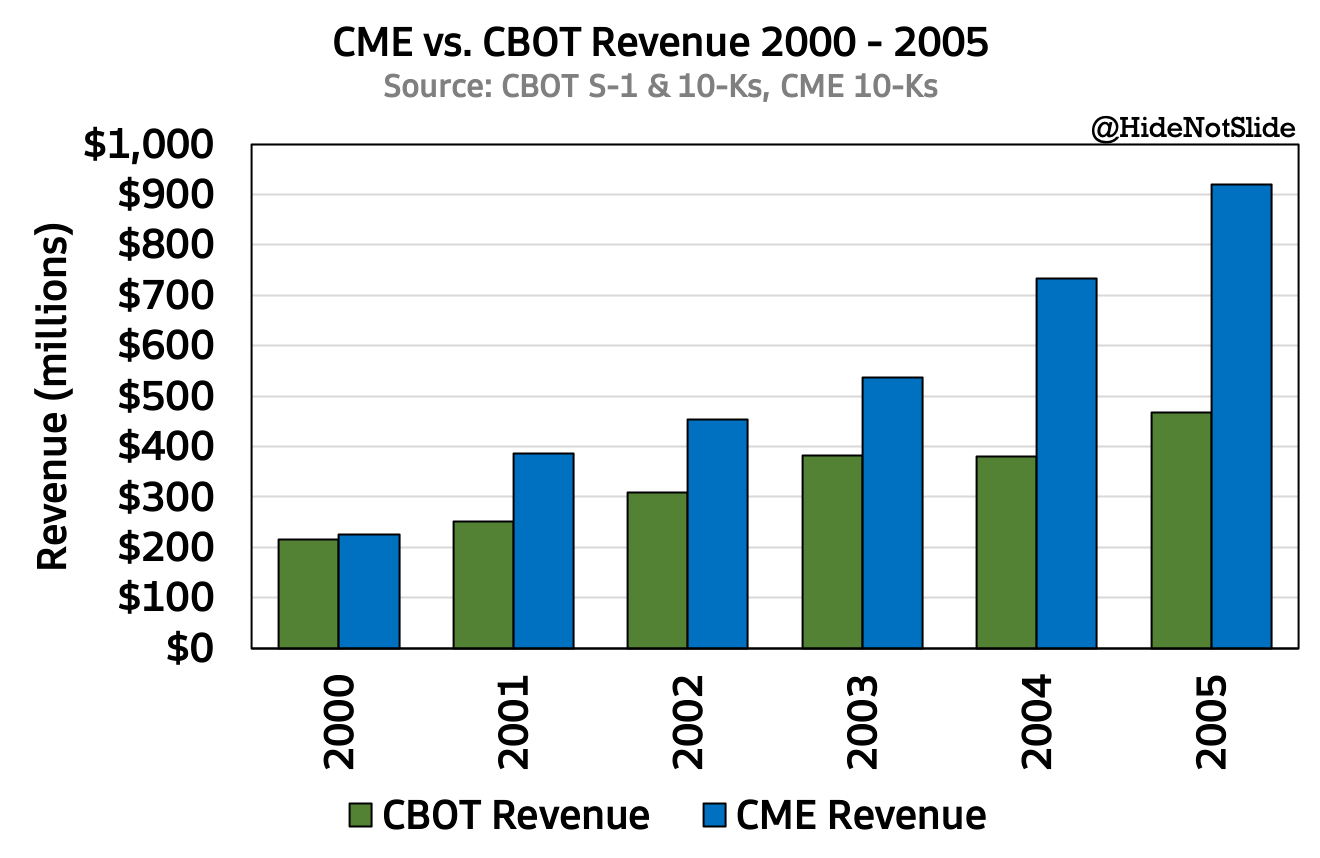

Instead, the city rivalry took the form of an arms race - which exchange could evolve faster, enter new markets, and overtake the other? Two important milestones gave CME the advantage. First, the exchange began to embrace electronic trading earlier, with the launch of Globex in the early 90s. Second, CME was the first exchange to demutualize & become a public company in late 2002. From 2000 to 2005, CME’s revenue grew from matching CBOT to almost doubling them in size:

By the mid-2000s, overseas challengers began to give Chicago a run for their money. Deutsche Börse’s Eurex had overtaken the CBOT in trading volumes, and was setting its sights on American expansion with the launch of Eurex US. Euronext & its newly purchased LIFFE had also begun to consider entering the US. If Chicago was to protect its lead, old rivals would need to band together to fend off European challengers. On October 17, 2006, CME announced its intention to merge with CBOT and create the largest derivatives exchange in the world, valuing CBOT at ~$7 billion.

Here’s where it gets interesting. An initially ho-hum approval process was turned upside down in March 2007 when ICE swooped in with a competing bid for CBOT at a ~$10 billion valuation. ICE CEO Jeff Sprecher reportedly slipped the offer under CBOT executives’ doors at an FIA conference, causing them to cancel planned presentations and consider their options.

As spring turned to summer 2007, ICE and CME traded ever higher bids for CBOT in an attempt to win shareholders over. CME was finally able to eke out a win for its cross-town competitor, but at a staggering $11.9 billion valuation - 60% higher than its initial offer. As an old rivalry within the city limits came to an end, a new one between Chicago and Atlanta was born. Although ICE didn’t end up winning CBOT, they were able to push the exchange’s final price high enough to make CME’s victory as expensive as possible.

If you’re interested in learning more on the wild fight for CBOT, I highly recommend reading Zero Sum Game by Erika Olson. Olson was working at the CBOT when CME’s initial merger announcement was released. She kept a detailed journal of the saga and interviews all the relevant players to capture the story in an accurate and entertaining way.

Honorable Mentions

According to the Financial Times, a think-tank advising incoming President Joe Biden put out a report calling for new restrictions on the big three asset managers and for BlackRock to spin off its Aladdin technology platform. The report invited response from BlackRock, State Street and Vanguard saying it contained “multiple factual inaccuracies” and that the proposal “would harm investors and companies”. Stories like this could be a signal of Biden’s stance towards not only big tech, but big asset management as a new cabinet takes over in 2021. BlackRock further grew its global reach on Monday with the $1 billion purchase of Aperio, a San Francisco based SMA manager with ~$36 billion in AUM.

Chart of the Week

As we’ve all most likely seen by now, Bitcoin prices are near all-time highs once again, and the cryptocurrency’s market cap has surpassed its 2017 bubble peak. CME launched their Bitcoin futures product in December of 2017, near the peak of the first crypto mania. Bitcoin options followed earlier this year. Many look to their suite of products as a signal of institutional adoption & interest in Bitcoin.

CME Bitcoin call buying has picked up substantially since early October, with calls outnumbering puts as much as 50-1 as of last week. The current opinion I’ve seen from knowledgable sources is that commercial adoption of crypto combined with a low relative float means Bitcoin could still have quite a bit of room to run:

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, CBOE, NDAQ and VIRT. I am also long Bitcoin.