CBOE Q4 2020 Earnings Review

CBOE Q4 2020 Earnings Review

This piece is part of a series on exchange & market data industry earnings - please SUBSCRIBE below for more earnings reviews & weekly writeups on the top stories in exchanges:

Links

Results

(Source: CBOE Investor Relations)

My love/hate relationship with CBOE got complicated in Q4.

On one hand, CBOE owns multiple high quality asset classes that are either enjoying record volumes or are in positions to recover meaningfully in 2021. Multi-listed options revenue grew an eye-popping +94% YoY in Q4. Index options, while struggling in 2020, have seen volumes trough & are on their way toward better comps in 2021. The same can be said for the VIX futures business - the past few quarters have been ugly, but traders are slowly coming back to the market & further recovery looks likely as markets stabilize. A secularly more active options market plus a healthy VIX & growing mix towards stable market data revenue should mean better results & an improving stock price. This loose thesis is why I initiated a position in CBOE in the low $80s towards the end of Q3 2020.

That’s about where good things end when digesting this earnings report. CBOE management spent 2020 embarking on a spending spree to bolster its market data business & expand geographically - 2020 acquisitions included Hanweck, FT Options, Trade Alert, MATCHNow, BIDS Trading, and EuroCCP. EuroCCP in particular underpinned a new series of investments in launching a European derivatives exchange sometime in 2021. On first glance, these deals seem in line with the normal strategy of an exchange - build a core technology platform and absorb adjacent businesses onto this platform, cutting expenses but keeping the associated revenues to capture economies of scale.

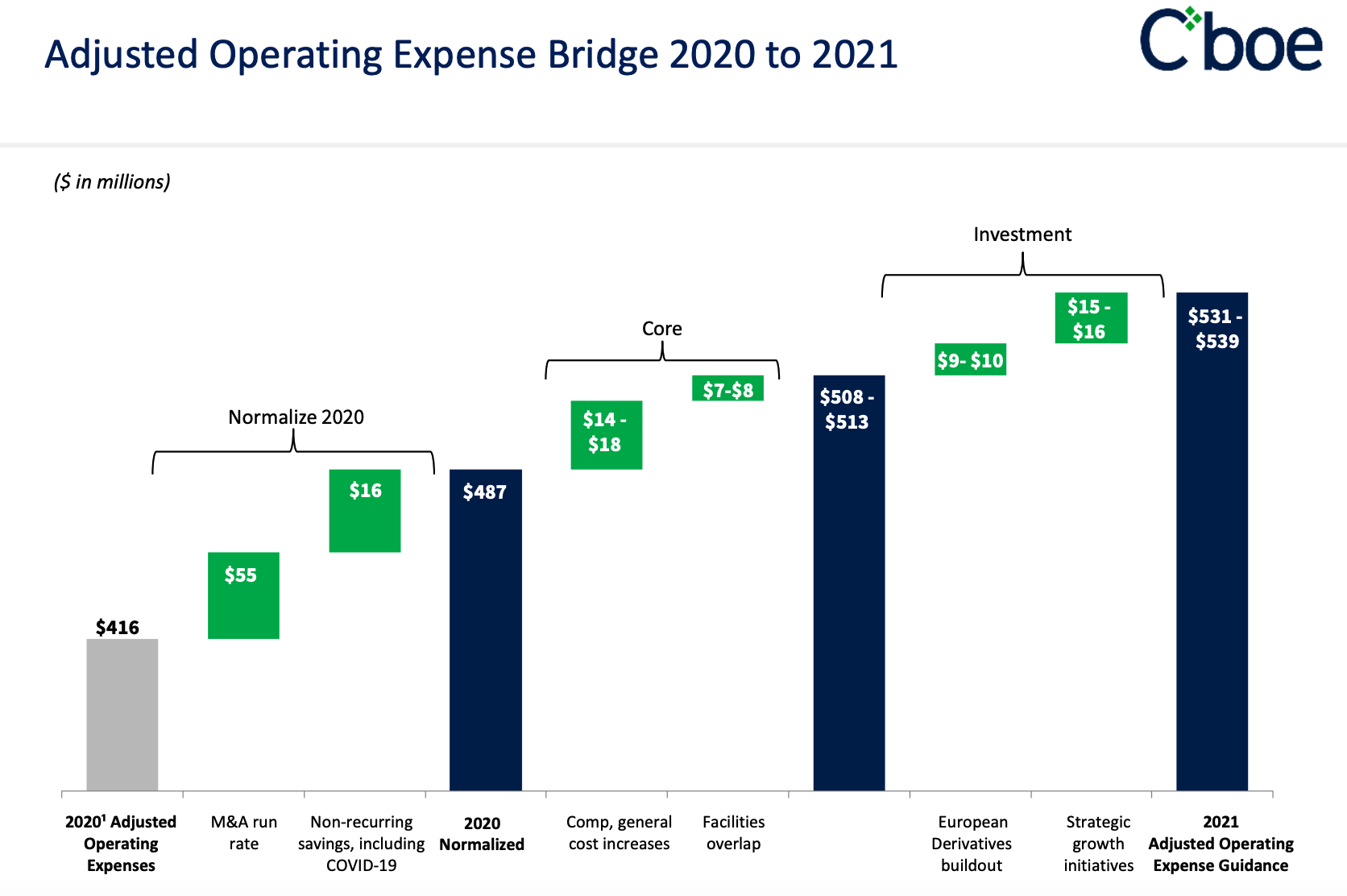

CBOE quashed this narrative when it released 2021 expense guidance calling for expenses to jump nearly +30% at their midpoint:

(Source: CBOE Earnings Presentation)

With the above slide, CBOE broadcasted that:

Their 2020 acquisitions come with no associated expense synergies - management clearly stated that “those transactions were not a cost play”.

Core expenses, including compensation & facilities costs, are expected to grow +5% before any additional investments are made.

On top of this, another $25 million of expenses are expected for more investment in Europe & other initiatives in 2021. Management highlighted that ~$20 million of this is recurring in nature.

While there is potential for expenses to underperform this range - if COVID keeps people at home some non-recurring savings could drag into 2021, and total expenses came in under guidance in 2019 and 2020 - a big increase in costs is coming in 2021. Core expenses plus investments account for a +10% increase in costs alone.

I can stomach growing costs if I can see a clear path to healthy returns on investment. That path so far is not perfectly clear with CBOE - along with a +30% expense guide, the company put out revenue guidance of +6-7% growth for its data businesses and +4-6% growth in total over the medium term. The data business grew +9% in 2020, so a +6-7% guide implies decelerating growth:

(Source: CBOE Earnings Presentation)

In summary, 2020 was not a great year for CBOE. Revenue grew through M&A, and its Index Options & Futures businesses suffered amid extreme volatility. This earnings call sent the message that 2021 may not be a great year either. CBOE’s European strategy requires a lot of investment, and their recent string of deals form many disparate parts rather than one comprehensive platform that would create synergies. Management’s concluding selling point? Trust us. Europe investments will pay off. Our strategy will show returns, just not in 2021. Hold on a little longer.

As a holder of CBOE, I need to ask the question - am I willing to trust that Europe will pay off? Is hope that Index Options & Futures will come back enough to hold the stock? Right now, I’m unsure. My confidence in the bull-case is beginning to fade.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this post, I am long ICE, CME, CBOE, NDAQ and VIRT. I am also long Bitcoin.