CBOE & Euronext Report Earnings

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

CBOE Earnings

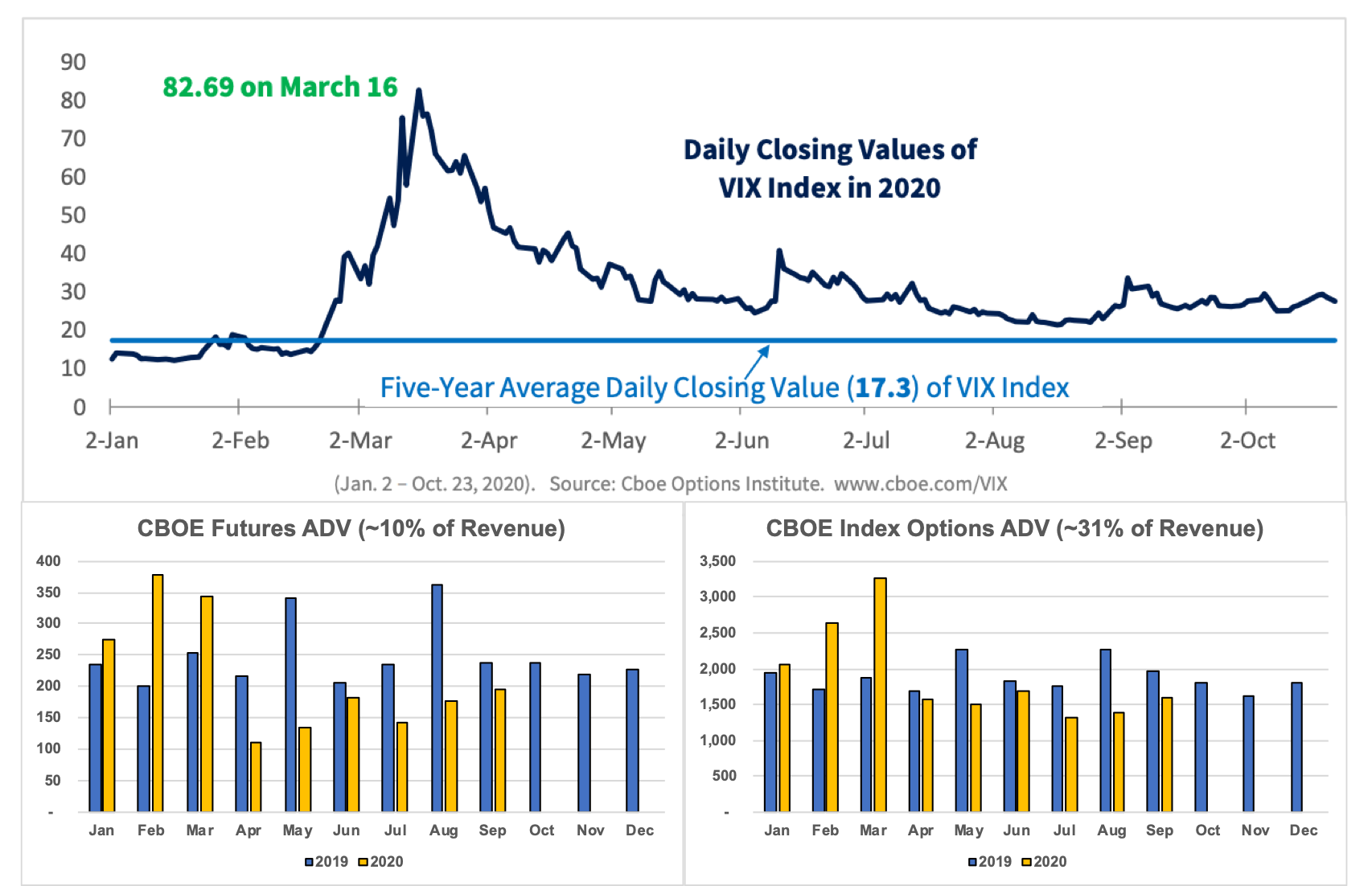

(Source)

CBOE reported earnings the morning of 10/30, publishing Q3 numbers that backed up the recent dismal showing for the stock. Revenue shrank -1% and EPS shrank -14% vs. Q3 2019 as futures & index options volumes suffered from a continuation of unhealthy volatility. The VIX has been above its long-term historical average since Q1, preventing both retail & institutional traders from piling back into CBOE’s volatility products:

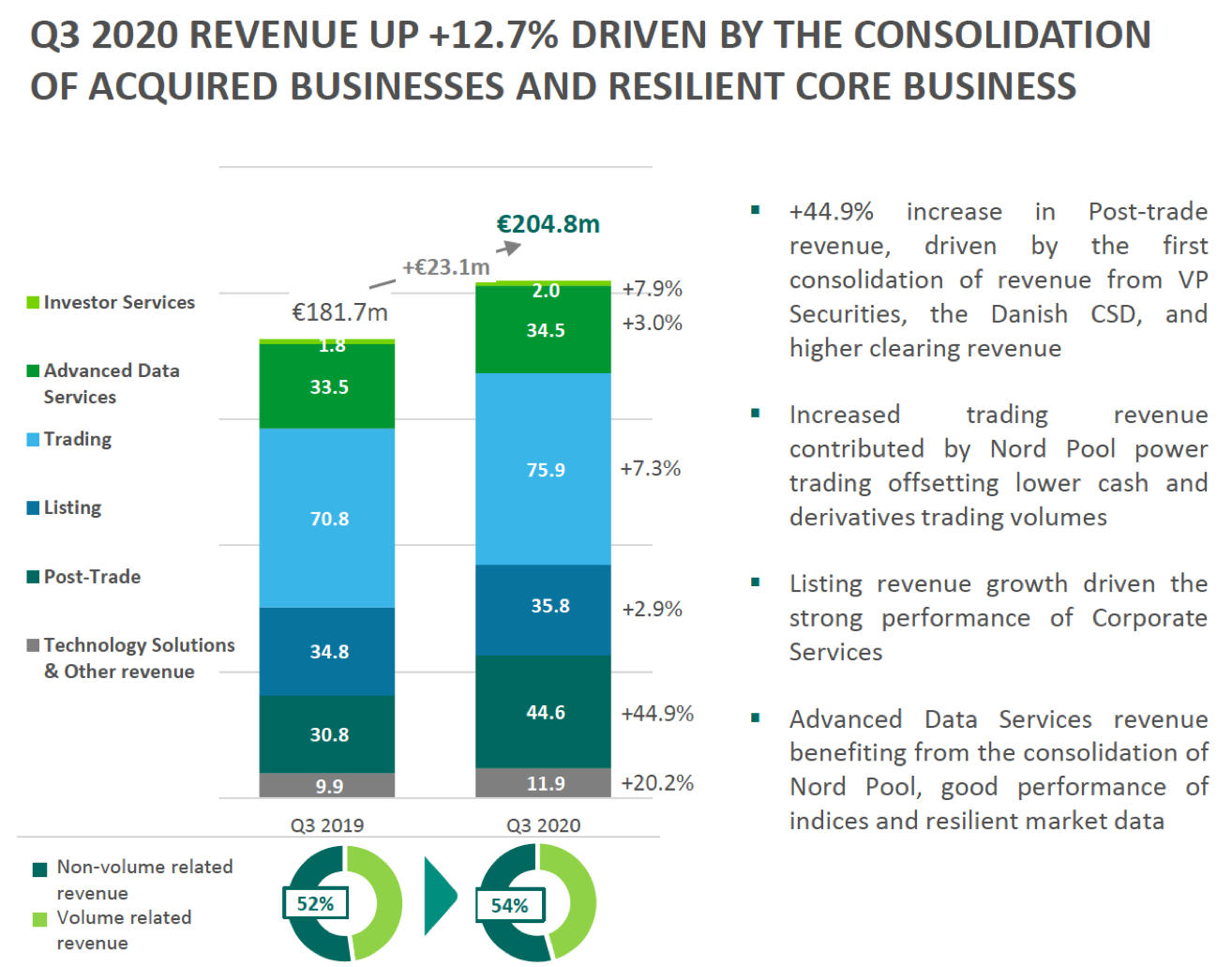

(Source)

Although the macro backdrop damaged CBOE’s results, there were some bright spots this quarter worth pointing out. Management highlighted upticks in retail demand for the company’s equity market offerings and associated proprietary market data. CBOE’s Retail Priority volumes - trades where retail designation outweighs speed in the order book - have grown to over 10% of their total cash equity volumes, and they raised expectations for market data growth from “mid single digits” to “mid-to-high single digits” organically. Management also lowered their FY 2020 expense guidance to reflect lower incentive compensation & T&E spend as the pandemic keeps employees working from home.

This was the first quarter since CBOE closed on its EuroCCP acquisition, and the company now expects its pan-European derivatives exchange to launch in 1H 2021 with six equity indices available to trade. Paired with their recent purchase of BIDS, the launch bolsters their presence in European cash equities & derivatives even more, with the goal of bringing more volume & liquidity onto lit exchanges.

As an owner of CBOE, I’m certainly disappointed with the macro story affecting their two largest products - VIX futures and SPX options. The company still seems to be reliant on the market & appetite for volatility to sustain growth, but I’m encouraged by what CBOE is doing to improve long-term performance. Management has made it clear they view strong and growing US equities market share as a high priority, and their recent acquisitions & pricing changes to rebuff competitors confirms this. They’ve also invested heavily in Europe with returns set to be seen in 2H 2021.

I think success in either US equities or Europe next year is crucial to reverse the struggling stock, with a resolution of election & COVID volatility as an added potential catalyst to boost their futures business.

Euronext Earnings

(Source)

Euronext released Q3 earnings on November 5th, reporting double-digit growth in revenue & EPS driven by M&A and listings. Low market volatility hurt Euronext’s cash equities & derivatives business, offset by moderate growth in recurring data & listings revenue:

(Source)

To diversify its business in a low vol environment, Euronext acquired physical power exchange Nord Pool in late 2019 and post-trade securities depository VP Securities in April 2020, contributing to the jump in Q3 revenue. The M&A game-changer, however, comes with the recently announced Borsa Italiana deal with LSE. Borsa Italiana will add more than €450M in annual revenue, make Italy Euronext’s largest market, and boost all parts of its business - from trading & clearing to listings, data & post trade products. As the deal gets expected regulatory approval, the stock will react to integration execution - synergy realization, maintaining market share in acquired products, and casting an aggressive vision for the combined group.

While I believe Euronext is still a macro-dependent exchange, its strategy of M&A - culminating with Borsa Italiana - gives investors reasons to be bullish over the next 2-4 years regardless of the macro environment.

October Volumes

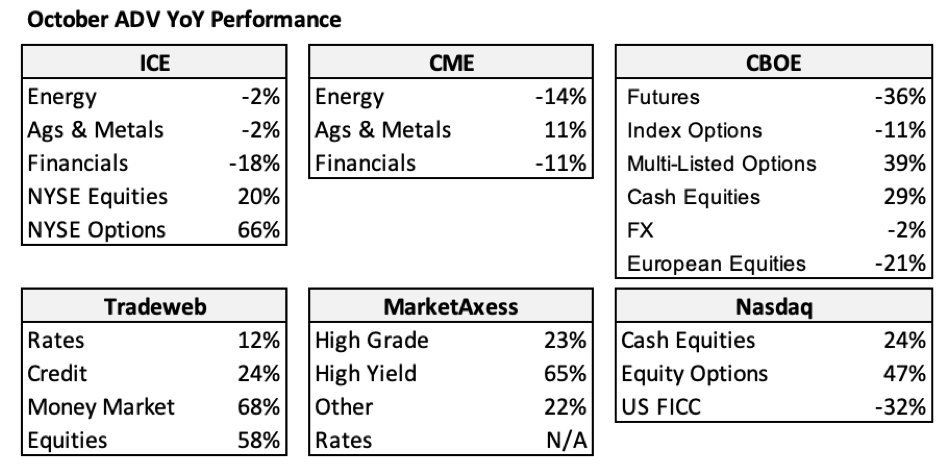

(Source: investor relations websites & press releases)

October volume reports were released across the exchange space this week, revealing the continuation of a “K-shaped recovery”. Markets that have struggled in 2020 kept struggling, and markets that have boomed this year kept booming.

Futures volumes were relatively weak across the board when compared to October 2019. ICE’s lead over CME in energy products has stayed firm, with CME showing better relative comps in Ags & Metals and Financials. CBOE’s VIX futures & SPX options products printed ghastly numbers for a 7th straight month after a tumultuous Q1.

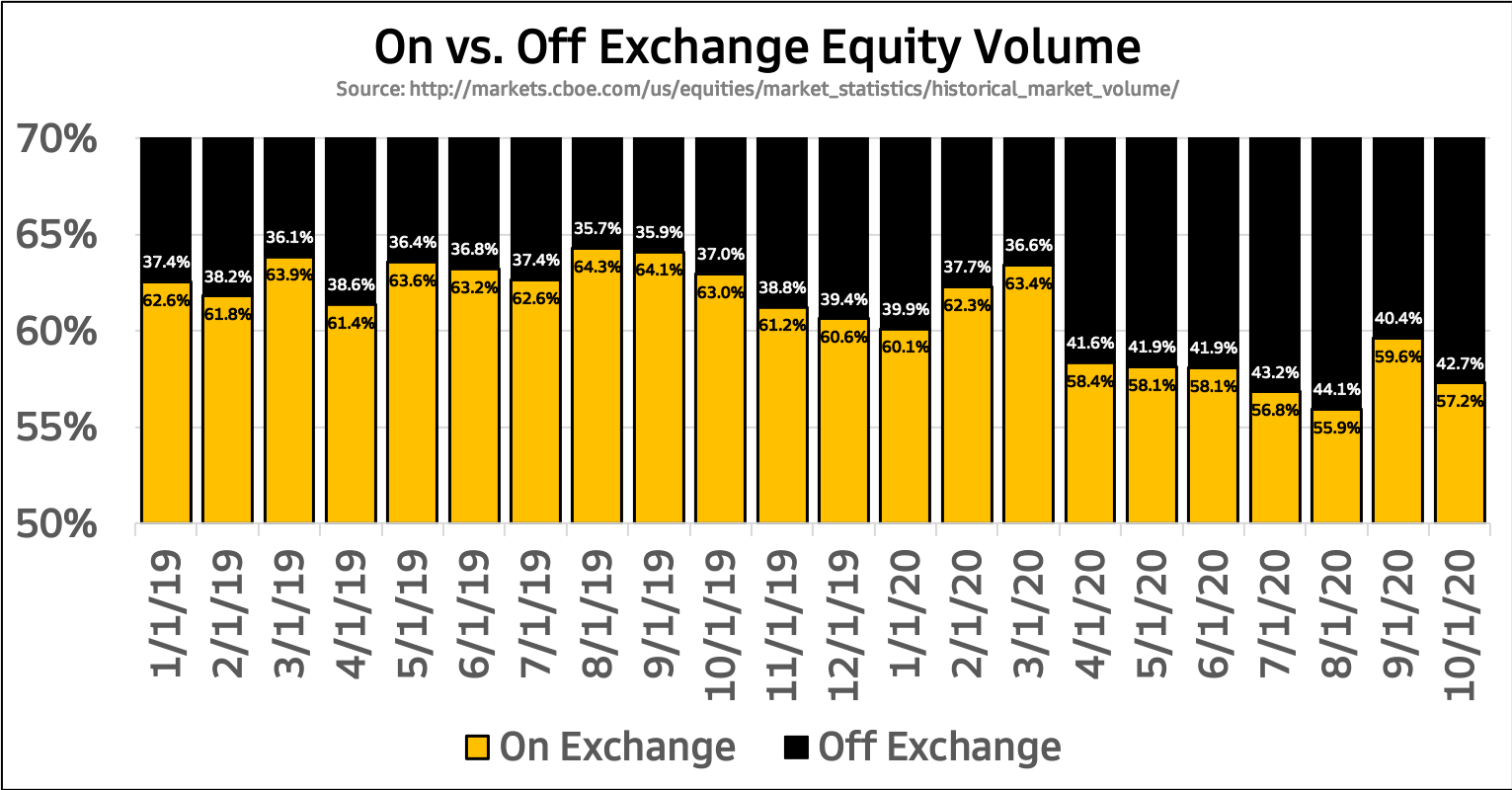

In the cash equities & options space the spotlight has been on not only strong industry volumes but high off-exchange market share. Since the March 2020 lows, over 40% of the US equity market has traded off a public exchange:

Among the public exchanges, the NYSE still controls the most equity market share at 21%, with Nasdaq & CBOE trailing in the mid-to-high teens. MEMX went live on all symbols towards the end of October, so expect their market share to trend upward throughout Q4. Nasdaq & CBOE stayed neck-and-neck in options with market share in the low 30%s, with the NYSE a distant third.

In the fixed income space, MarketAxess & Tradeweb posted strong volume growth once again. MarketAxess has grown corporate bond market share every month in 2020. Tradeweb saw surprising strength in repo & ETF trading as more users signed up to their markets. Tradeweb’s corporate bond market share kept rising as well, with over 19% of IG corporate bond trading taking place either fully or partially electronic through their platform.

Honorable Mentions

Two weeks ago I talked about Euronext’s recent technology glitch that caused multiple trading outages. This week saw reactions from participants & regulators - growing pressure to implement a consolidated tape in Europe. In the US, a consolidated tape already exists that provides one all-in feed of stock prices from all active trading venues. A similar feed in Europe would have allowed trading to continue on other venues despite Euronext’s outage, but could take trading & data revenue away from incumbent exchanges.

On November 1st, China further eased barriers for foreign money to enter their capital markets, including greater access to onshore futures markets and securities lending. The move should boost Asian demand for market data & infrastructure, a positive development for S&P Global, Moody’s, MSCI, and other exchanges with Chinese growth ambitions.

The Financial Times reported this week that the NYSE has reclaimed the listings crown from Nasdaq after losing it last year, driven by growth in SPAC listings. The NYSE and Nasdaq have attracted a similar number of SPACs, but the NYSE has secured larger deals after lowering fees & easing listing rules for the newly popular entity structure. While we may be in the midst of a “SPAC bubble”, the long term impacts of higher listing subscription revenue will help both exchanges for many years to come. Listings accounted for ~11% of Nasdaq’s revenue & ~8% of ICE’s revenue in Q3 2020.

Chart of the Week

An ongoing story in the futures world has been the globalization of energy infrastructure. As the global oil trade grew in the 1980s, exchanges were able to launch successful futures contracts and capitalize on the growing worldwide demand to hedge crude oil exposure - IPE with a Brent contract and NYMEX with WTI.

Today, a very similar story is unfolding in natural gas. As European & Asian demand for natural gas rises, energy companies & speculators need a deep, liquid market that serves as a global benchmark they can use to hedge. Recent data shows ICE’s Dutch TTF contract may soon be deserving of that label. the Netherlands-based gas contract saw open interest surpass that of the largest US market - Henry Hub - in 2020.

(Source)

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, CBOE, NDAQ and VIRT.