Brasil, Bolsa, Balcão

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

There’s no arguing that financial markets have now become deeply interconnected on a global scale. Retail & institutional customers can now cheaply trade financial instruments of almost every country in the world at the push of a button. When it comes to the exchanges underpinning these global markets, however, the story gets quite messy. Global exchange competition has long been an interesting & important story to watch as markets mature, and no market showcases this better than Latin America.

This week I want to chronicle the fascinating rise of Latin America’s top exchange, the Brazilian market operator now called B3, and its intense battle with US exchange heavyweights that made B3 what it is today.

Bolsa’s Beginnings

The roots of Brazil’s largest exchange stretch back to 1890 with the formation of “Bolsa Livre” by Emílio Rangel Pestana, then a wealthy & well-connected stockbroker. Similar to the NYSE, Bolsa Livre was born when many of the largest Brazilian brokers decided to work with each other to lower costs & improve trade. Bolsa Livre’s birth, however, was ill-timed - a speculative bubble caused by aggressive inflation & government stimulus popped in 1891, and the resulting crash drove Bolsa Livre to bankruptcy. It took four years for the economy to recover enough to attract a new exchange, when the Sao Paulo Exchange was born from Bolsa Livre’s ashes. Brazil’s economic position was sturdy enough this time to support a new exchange’s formation.

During the early to mid-1900s, Brazil’s capital markets consisted of various regional, state owned exchanges operating under government control, of which Sao Paulo was one. As Brazil’s economy grew, market reforms became necessary to keep the country competitive with other developing nations. In 1965 exchanges were privatized, and the Sao Paulo Exchange began growing independent of its former government handlers. Intense competition between the regional exchanges ensued, and Sao Paulo was able to weather a series of market crashes in the early 1970s to grow market share. Sao Paulo’s key advantage this time was an early embrace of automation - in 1972, they were the first Brazilian exchange to begin disseminating stock quotes electronically in real time.

A second market crash in 1989 again favored Sao Paulo, sealing its dominant status among Brazil’s exchanges for good. Naji Nahas, an omnipresent & corrupt billionaire among Brazil’s financial community, had built massive positions in equities during the first half of 1989. Nahas was able to use his extensive relationships with banks & brokers to access extreme leverage for his account - he effectively only used his broker’s money to bet on stocks.

As Nahas’s leverage grew ever more extreme, the Sao Paulo exchange took the conservative route and raised Nahas’s margin trading rates. In response, Nahas simply took his business cross-country to the Rio de Janeiro stock exchange, then the biggest venue in Brazil. The Rio stock exchange enticed Nahas with low fees & huge trading leeway, similar to other firms looking for the billionaire’s book of business. At one point, Nahas’s account alone made up 50% of all equity trades on Rio’s exchange - a truly mind-blowing amount of activity for one account. However, all was not as it seemed, and Rio’s sunny days were about to come to a swift end.

On June 12, 1989, Nahas’s overleverage had finally caught up with him. A $30M check to his brokers bounced, causing a rapid insolvency crisis among institutions with too much exposure to his portfolio. As brokers & banks liquidated & scrambled to cover their losses, markets dropped -15% in one day, the worst crash in Brazil’s history. After the dust had settled, six brokerages had failed, Brazil’s head central banker had resigned, and the Rio Stock Exchange was forced to suspend operations. Rio’s exchange president resigned shortly thereafter. As Nahas’s associates took the brunt of the market fallout, traders quickly flocked to the next biggest national exchange - Sao Paulo - and never looked back.

With its largest competitors decimated by a trading scandal and market crash, the Sao Paulo Exchange was free to expand as Brazil’s new largest market center. Brazil’s economy continued to grow in the late 1990s and early 2000s as market reforms brought new inflows of foreign capital to the country. The Sao Paulo Exchange rode this wave of economic growth & invested further in electronic trading to bring its technology in line with other global exchanges. In 1997 the exchange launched the “Mega Bolsa”, a new electronic equities trading platform, and by 2005 trading on its exchange had become fully electronic. The Sao Paulo Exchange had survived competition, scandal & a wholesale tech transformation to become Brazil’s dominant equities platform. In 2007 the exchange completed its IPO and became a public company, and with a new base of shareholders to satisfy, the exchange looked for ways to expand outside of its core equities business. M&A became the avenue of choice for Sao Paulo to unlock the next era of Brazil’s exchange evolution.

On March 26, 2008, the Sao Paulo Exchange announced it was merging with the Brazilian Mercantile & Futures Exchange (BM&F) in a blockbuster $10 billion deal. While Sao Paulo had grown to dominate Brazilian equities, BM&F followed a similar path to dominate Brazilian futures. Expanding through acquisition & with help from Brazil’s strong economy, BM&F had grown to become the country’s top exchange for interest rates & equity index products, and had IPOd around the same time as Sao Paulo. A merger of equals would solidify the two exchanges as an attractive hub for institutional capital flowing into Latin America, and provide meaningful synergies from overlapping labor & sharing of technology. The combined entity was renamed BM&FBOVESPA, symbolic of the two exchange’s shared identity & equal company ownership. Brazil was now without a doubt a forced to be reckoned with in the global exchange landscape.

Here Come the Americans

The $10 billion deal between Sao Paulo & BM&F was large enough to attract US exchange attention, and headlines soon surfaced from ICE, CME and BATS (now CBOE) that they were considering expansion into Brazil & Latin America.

The first big move by a US exchange came from CME, choosing to join BM&FBOVESPA rather than enter their market & compete head-to-head. In October 2007, before news of the Brazilian merger had even been released, CME announced a unique partnership with BM&F - the two exchanges would swap equity stakes in their respective companies. After the swap, CME would own 10% of BM&F and BM&F would own 2% of CME. The two companies also committed to link together their futures markets & collaborate on new products. CME’s commitment to expanding their influence in Brazil was backed up with serious ongoing investment - the exchange would later go on to completely redesign BM&FBOVESPA’s technology platform, rolling out a new integrated PUMA electronic trading system in the early 2010s.

The next exchange to give Brazil a try was BATS, deciding to fight BM&FBOVESPA head on in Brazilian equities. In early 2011, BATS announced they had signed a memorandum of understanding with Claritas, a Brazilian asset management firm, to begin scoping the buildout of a Latin American stock exchange. This foray ran into serious problems when BM&FBOVESPA mentioned later that year that it wouldn’t share its vital equity clearing services with newcomers, effectively stopping BATS’s plans in their tracks.

Finally, ICE took a crack at Brazilian expansion, also in 2011, with the purchase of a 12% stake in CETIP, Brazil’s largest fixed income clearinghouse. Just like CME, ICE’s investment came with an ongoing agreement to share technology & work on new products. ICE & CETIP chose to go after the Latin American corporate bond market with the launch of CETIP Trader, an electronic bond platform to pair with CETIP’s clearing function.

For a few years after these respective deals were made, it looked like Latin America was set to become the next financial frontier for US exchange dominance. With ownership stakes & multi-year tech partnerships with the top Brazilian market operators, it seemed as if the US had entered a back door into a region once thought to be BM&FBOVESPA’s for the taking.

The story, however, doesn’t end there.

Tchau USA, Hola B3

In 2016, BM&FBOVESPA made a series of moves that turned its position from a potential pawn in the US-Latin American expansion story into the dominant market leader it is today. The week of April 8, the company made several explosive announcements:

It was planning to buy CETIP for $4 billion, including ICE’s stake.

It was selling its stake in CME to pay for the acquisition.

It was ending its trading partnership with CME in the process.

Wow. In one fell swoop, via M&A, BM&FBOVESPA had cut off the top two US exchanges from their future Brazilian plans, using their own money to do so. I at least find it ironic that the proceeds from CME’s equity sale made its way into ICE’s coffers via CETIP, all while effectively kicking both exchanges out of the country.

How did ICE and CME let this happen? For one, both exchanges were dealing with transformations of their own, including massive acquisitions of the NYSE and NEX Group that presumably took their focus away from Latin America. I suspect another contributing factor was national politics - BM&FBOVESPA was originally a Brazilian quasi-government entity. Most nations generally want their markets to trade on their own national exchange, rather than an exchange owned by a foreign conglomerate. I suspect that ICE and CME saw they weren’t going to make much headway in Latin America without Brazilian regulatory support, and that didn’t seem very likely given what happened to BATS. Better to take a small gain on investment and move on to bigger and better things in the US.

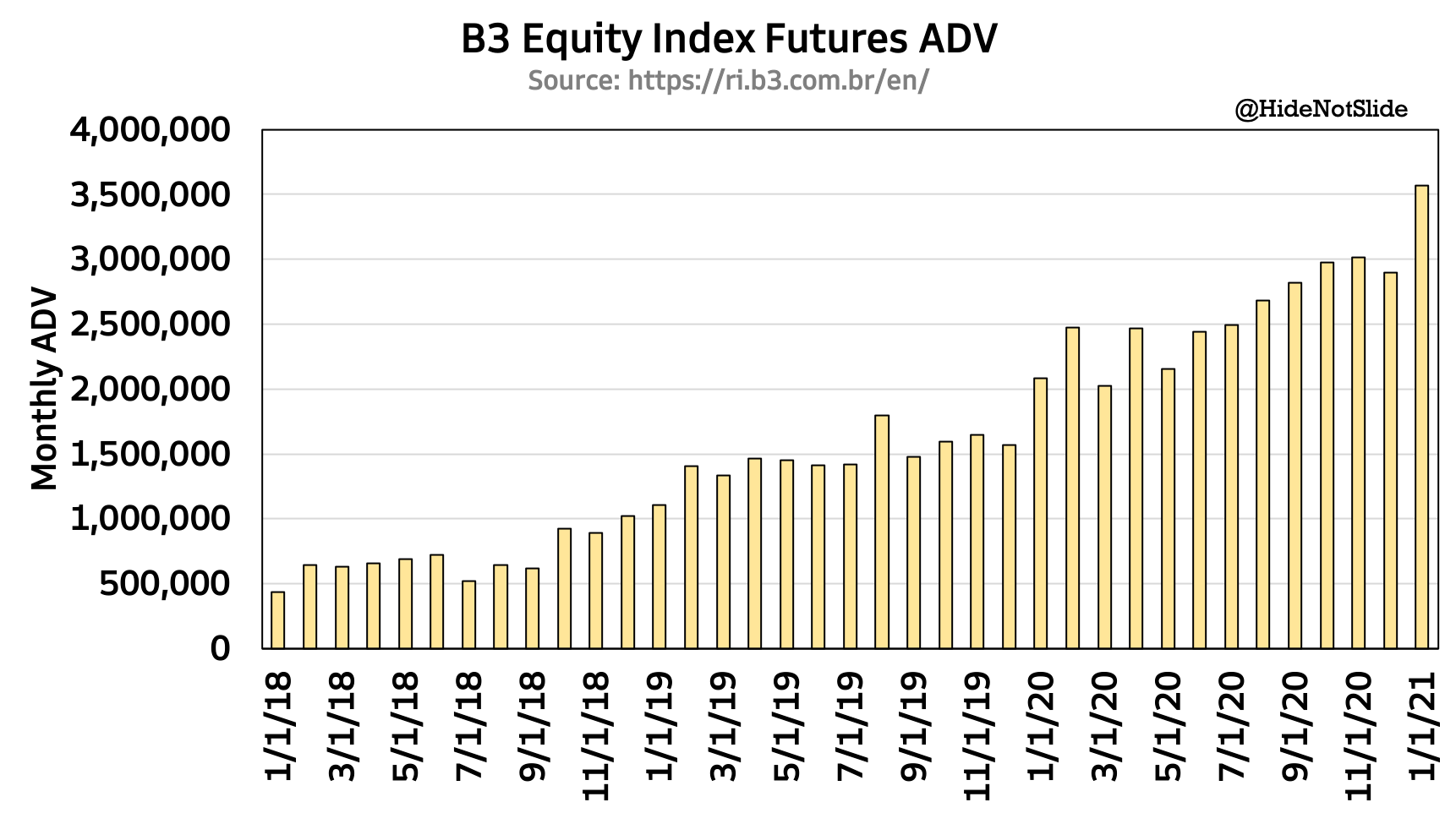

After the CETIP deal, BM&FBOVESPA decided to change its name once again, this time to B3 - Brasil, Bolsa, Balcão. B3 is now by far the largest exchange in Latin America, with interests stretching across equities, futures trading & clearing, and fixed income. The company has since purchased minority stakes in the Mexican, Colombian and Chilean exchanges with the long-term goal of integrating Latin American financial markets. B3 brought in ~$1.5 billion in 2020 revenue, putting it ahead of other well-known exchanges like CBOE & Euronext. Its flagship iBovespa index is considered the benchmark for Latin American business performance, and its equity index trading volume has grown 7-fold since early 2018:

Just because US exchanges aren’t expanding into Latin America doesn’t mean the region isn’t worth pursuing. In fact, the top exchanges tried mightily to break into the southern hemisphere with acquisitions & significant investment, but were shut out by Brazil’s dominant exchange that’s weathered more than its fair share of competition.

Wether it be market crashes, corrupt billionaires, or competitors both foreign & domestic, B3 has navigated through a wide range of challenges to become the market leader it is today. As Latin America keeps its streak of strong economic & technological growth alive, don’t overlook B3 as a global exchange contender in the years to come.

Honorable Mentions

On March 8 CME announced fresh all-time record volumes for its micro e-mini equity index futures, beating the previous record by an eye-popping 700K lots. Micro e-mini futures are seen as more accessible for retail traders given their small relative contract size; volumes have performed particularly well in 2021 driven by the Nasdaq-100 index.

Platts, a subsidiary of S&P Global gave oil traders quite a surprise last week when it announced it was making emergency changes to its Brent benchmark, used to price more than two-thirds of the world’s crude oil. The development particularly matters for ICE and CME, the top two oil exchanges in the world with futures contracts tied to Platts benchmarks. Platts is concerned that the North Sea is running out of crude oil, and is considering adding American WTI oil to its flagship index. This would be a boon for CME, the dominant WTI futures market, while a setback for ICE, the owner of Brent futures & a struggling competitor in WTI.

The SEC announced on March 10 that it was delaying approval of Nasdaq’s board diversity rule, requiring companies to have at least one woman & one minority or LGBT member on its board.

Charts of the Week

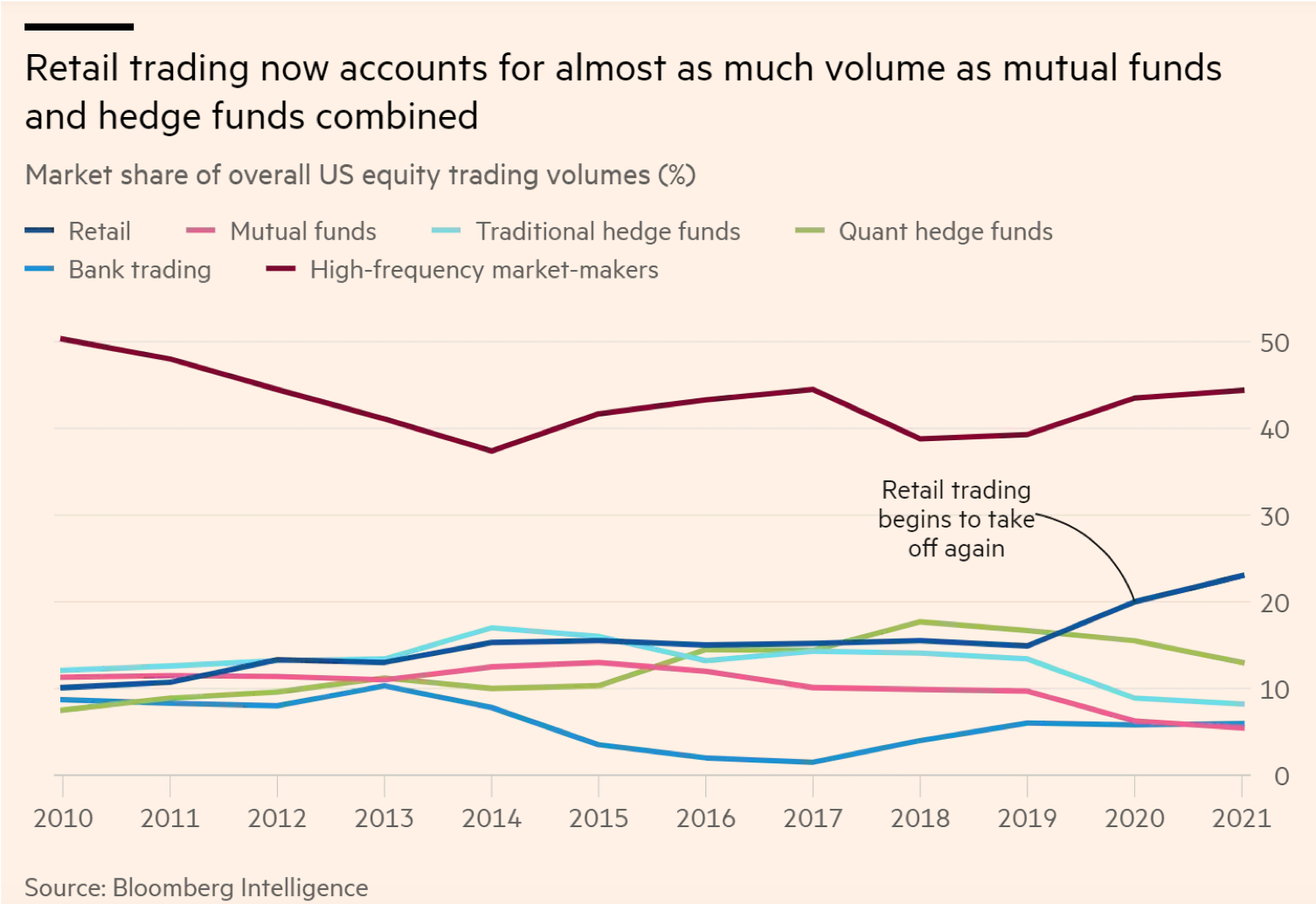

The Financial Times put out a set of interesting charts this week detailing the rise of retail trading in the US equity market. The first chart below shows how retail share of the equity market has surpassed 20% for the first time since the GFC, accounting for the same amount of volume as mutual funds & hedge funds combined.

The second chart looks at the 10-day rolling purchases of US stocks by retail investors, giving a sense for what stocks & sectors are benefitting from retail’s focus. I find it interesting that ETFs are now the top area of interest for retail after a rotation through Reddit names, ESG, growth, and travel/re-opening plays throughout 2020.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Bitcoin.