Asia - The New Exchange Frontier

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

Crazy Rich Asian Growth Prospects

(Source)

{kind=link}

4.7 billion people.

$65 trillion of GDP - larger than the rest of the world combined.

Growing access to the Internet, middle class incomes, and financial freedom.

Asia has quickly become the epicenter of global economic growth, and as Asian financial markets slowly reduce barriers to foreign entry, exchanges are scrambling to establish a foothold.

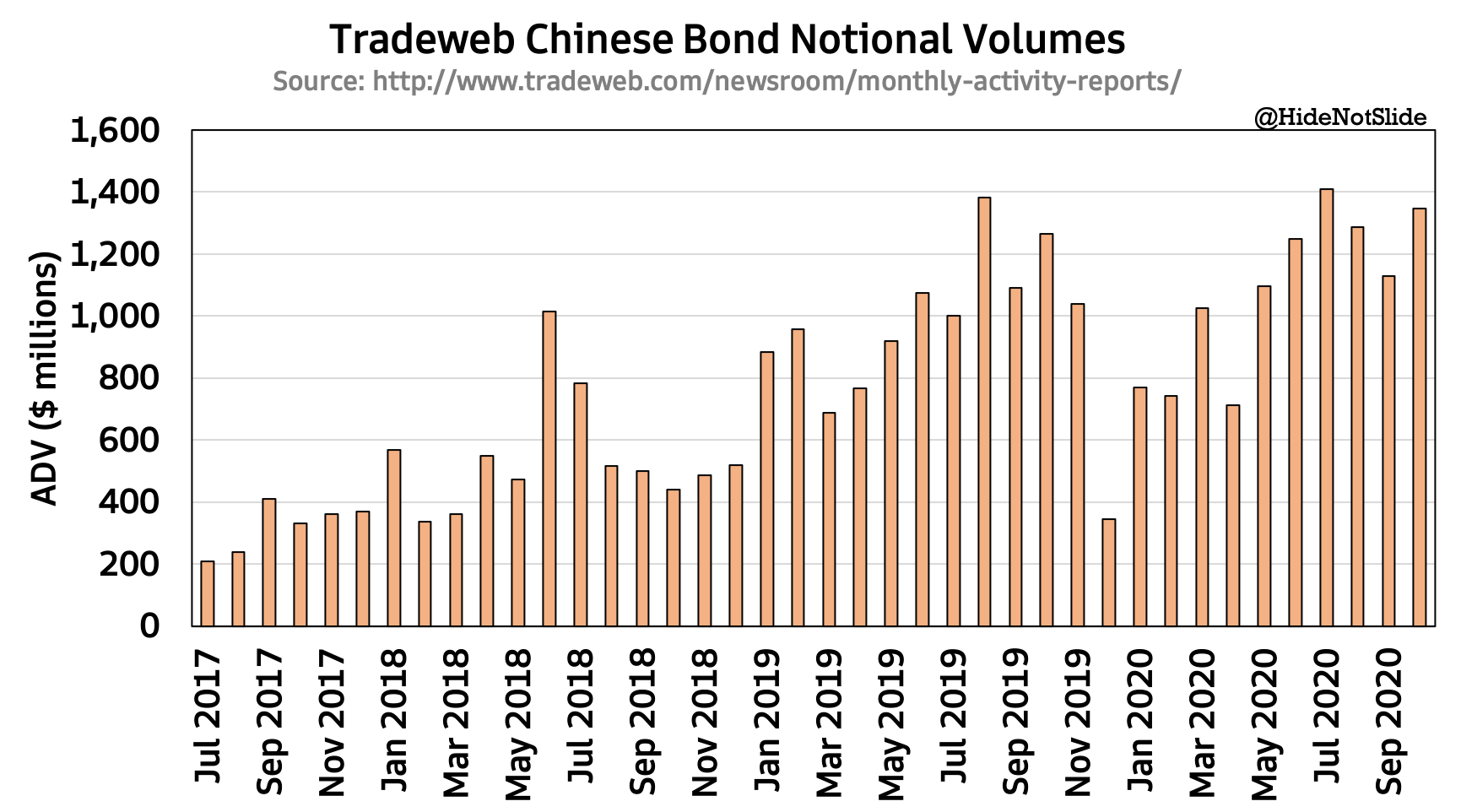

Some exchanges are taking a transaction-focused approach to Asian expansion, in line with their core strategy & company profile. Take Tradeweb - they entered China in 2017 through a partnership with BondConnect, a joint venture sponsored by the People’s Bank of China and Hong Kong Exchange. Since launch, over $620 billion of Chinese bonds have changed hands on Tradeweb’s platform:

Or take the futures exchanges - ICE & CME both tout recent energy market success due in part to rising demand in Asia. Because the region’s gas pipeline network is still relatively nascent, energy companies doing business in Asia need a liquid seaborne market to hedge their price risk. ICE’s Japan/Korea Marker liquified natural gas contract is quickly becoming that market - trading volumes tripled from 2018 to 2019 and grew more than +30% year-over-year in October 2020 alone. CME’s Henry Hub gas & WTI oil contracts are benefitting in a similar way; trading volumes from Asia grew +18% YoY in 2020, far outpacing US growth and now making up ~6% of CME’s total volume.

Some exchanges are using M&A to up their exposure to Asia’s future. The London Stock Exchange’s Asian presence will grow substantially with their pending acquisition of Refinitiv, where annual revenues from the region already top $1 billion per year. Asia is estimated to make up ~12% of LSE & Refinitiv’s combined business post-merger, with a large share of that recurring in nature.

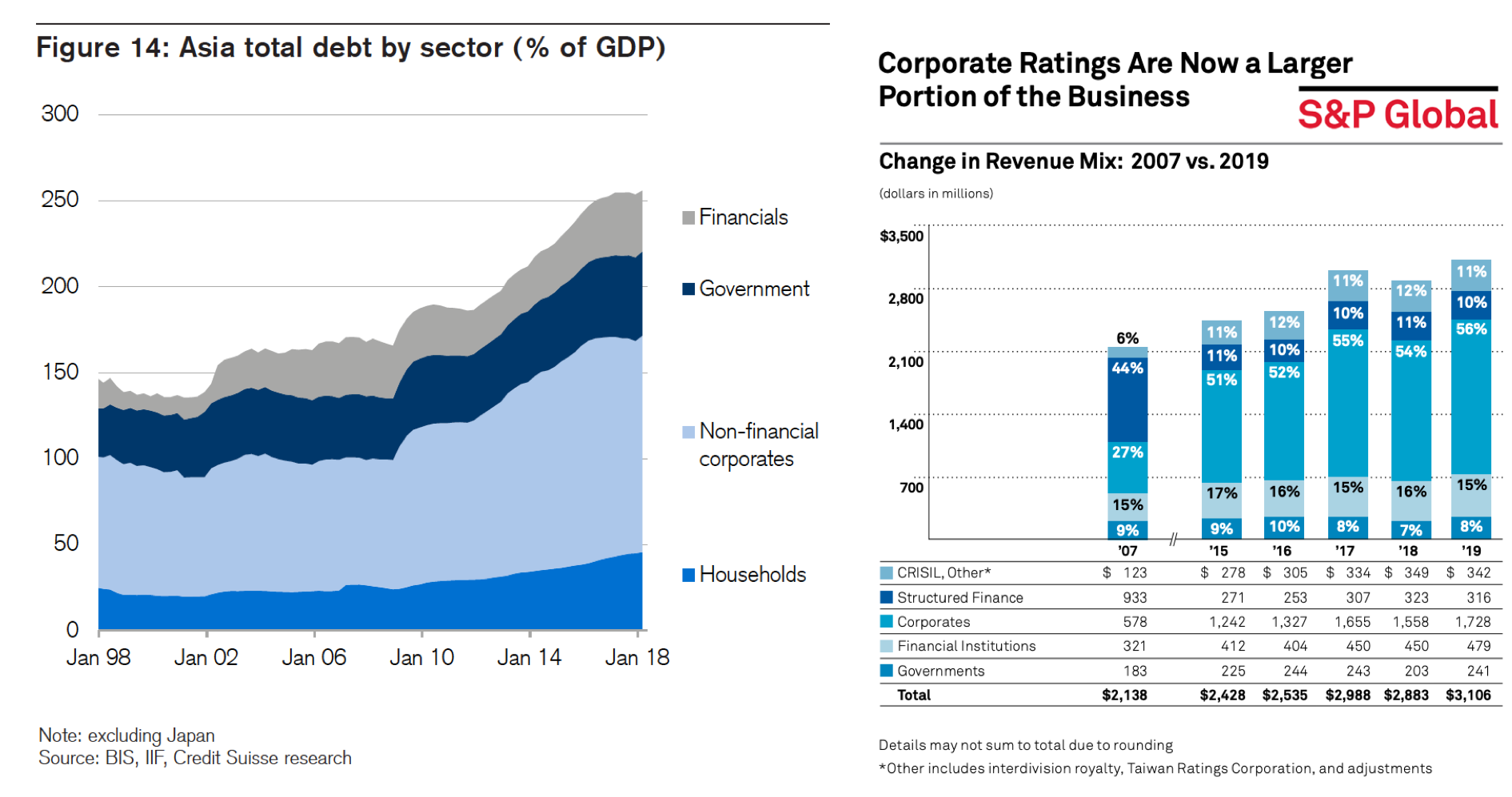

On the ratings front, S&P Global looks to have a sizable lead over Moody’s in Asia. in 2019 S&P rated over 50% of the $826 billion addressable APAC debt market, where corporate debt is making up a greater slice of the overall market - right in S&P’s wheelhouse:

(Corporate debt is the largest share of both Asia’s debt and S&P Global’s ratings business. Source)

A large share of the debt that S&P Global doesn’t rate is taken by China Cheng Xin International Credit Rating Co., Ltd. (CCXI), the first nationwide Chinese ratings agency. In the mid-2000s Moody’s acquired a 30% stake in CCXI, giving them an indirect link to China’s growing domestic debt market in addition to cross-border business. Today Asia makes up ~11% of S&P Global’s annual revenue compared to ~4% for Moody’s.

Asian market development has perhaps supported global data providers the most so far. For Nasdaq, FactSet and MSCI, Asia ranks as one of the fastest growing parts of their business. Nasdaq’s Asian business has grown at a +13% CAGR between 2016 and YTD 2020, driven by indexation and demand for regional exchange-traded products. When Nasdaq laid out their 3-5 year strategy during a recent Investor Day, Asia was a key pillar of future growth:

(Nasdaq’s Investor Day Index segment outlook - Source)

After assessing the competition, I’m convinced MSCI is today’s winner in Asia. First, they have the most exposure to Asia of the field. APAC makes up 17% of their total subscription revenue and over a fifth of their core index business.

Second, they have partnerships in place that allow them to capitalize on future growth. In May 2020 they signed a license agreement with Hong Kong Exchange to launch 37 futures & options contracts on their Asian & emerging market indices.

Third, MSCI has positioned their index product suite to give the Asian market access to passive investing. In late 2019 MSCI completed its inclusion of China A shares in a number of its indices, including the Emerging Markets Index with linked assets numbering in the trillions. The more behind-the-scenes index tweaks MSCI makes now to prepare for growth in Asia, the easier it will be for billions more in AUM to flow their way in the years ahead.

In closing, to say Asia is a huge opportunity for market infrastructure operators would be an understatement. Whether it be through state partnership, M&A, or leveraging secular trends like energy liberalization or passive investing, exchanges are doing whatever they can to get a piece of the Asian growth trend. I believe MSCI is leading the field in Asian expansion, but am impressed with ICE & Tradeweb’s transaction success and S&P Global’s ratings progress as well.

2020 - The Year Of Exchange M&A

Multiple large exchange M&A deals were signed this week, adding to the already lengthly list of tie-ups that have either been announced or are ongoing in the industry this year.

First, the Financial Times reported on November 17 that Deutsche Börse has purchased 80% of proxy advisory firm ISS at a $2.3 billion valuation.

Institutional Shareholder Services (ISS) makes ~$280 million per year advising & servicing thousands of asset managers on shareholder votes. ISS went from a subsidiary of MSCI in 2014 to a portfolio company of multiple PE firms until DB1’s buy this year.

For Deutsche Börse, the deal looks to be built on ESG data & analytics - below comments from management seem to confirm this:

“This partnership of a global market infrastructure provider with a leading corporate governance, ESG, data and analytics provider forms an excellent foundation to fully realise opportunities for future growth in ESG-based investing globally. With this transaction, Deutsche Börse strongly commits to one of the key megatrends in the industry that will fundamentally change the investment space over the coming years. ISS’ unique ESG and data expertise will allow Deutsche Börse to emerge as a leading global ESG data player.”

-DB1 press release

While gaining exposure to ESG is a positive, there are those who argue the marriage of an exchange & a proxy advisor poses potential conflicts of interest. If an exchange benefits when more customers need their premier ESG data, wouldn’t there be an incentive to advise shareholders & boards towards ESG-focused corporate governance? The downstream impacts of such a deal remain to be seen. DB1 says they expect to close on the ISS purchase in 1H 2021.

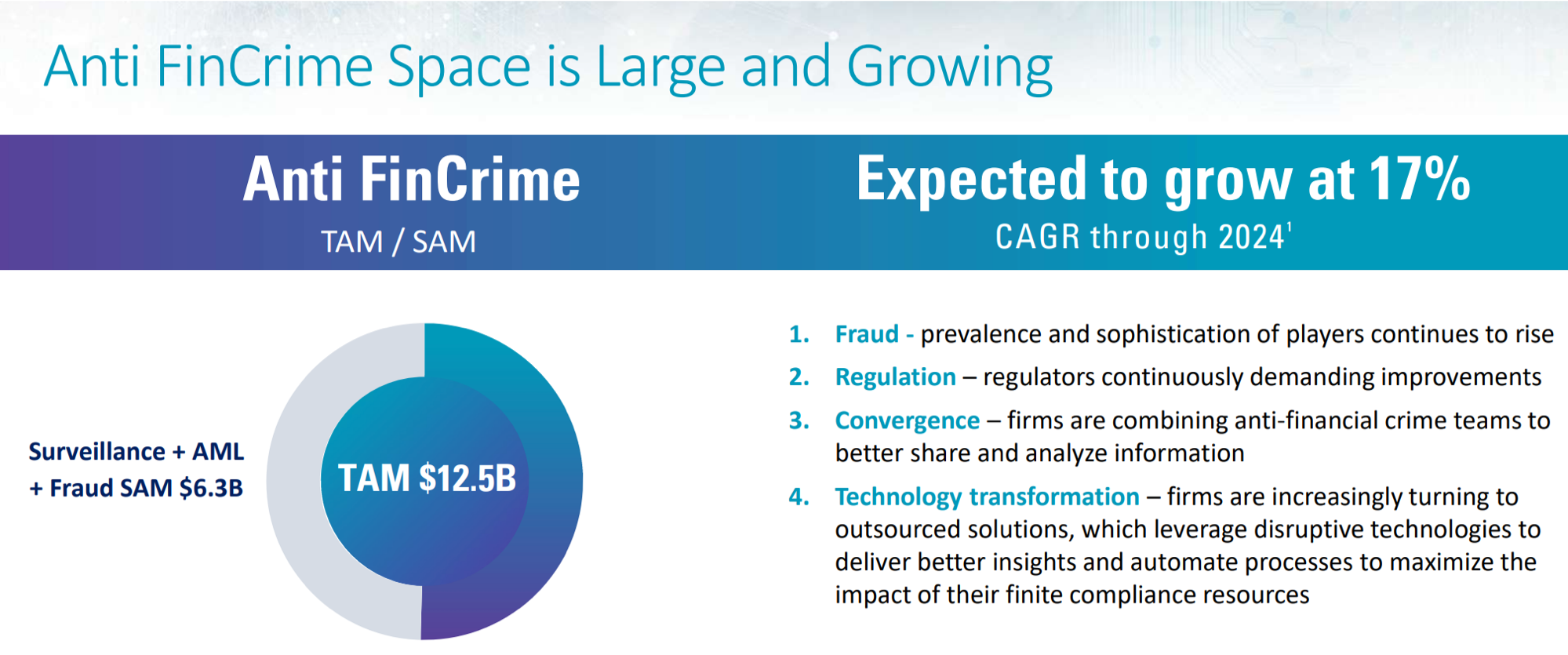

Second, on November 19 Nasdaq announced its $2.8 billion purchase of Verafin, a financial crime management platform. The deal pushes Nasdaq further into the anti-fin crime space where management argues the addressable market is large and untapped:

(Source)

To me the deal makes sense given their updated strategy discussed during Investor Day on November 10. Nasdaq is putting money where their mouth is - managing expenses in their transaction segments & focusing resources on a SaaS transformation, where growth prospects are higher and less volatile in nature.

In conjunction with the Verafin announcement, Nasdaq raised their outlook for Market Technology and Information Solutions growth as their SaaS revenue mix improves:

(Source)

Nasdaq expects the deal to close in Q1 2021.

Honorable Mentions

On November 16 the Australian Stock Exchange suffered its largest outage in a decade after a trading system update produced errors causing “inaccurate market data”. Nasdaq was the primary technology provider and who’s software glitch was behind the outage. Australian securities regulators put a release out saying they’re “concerned” and are assessing whether any licenses have been breached. The outage comes on the heels of Nasdaq’s Investor Day where they gave 3-5 year growth targets with Market Technology as a key driver of that growth.

On November 17 CME launched a suite of new volatility indices tracking 10-Year Treasury & FX futures, with more to come in 1H 2021. The move solidifies the exchange’s push into volatility - as more indices are published & traders begin to view CME’s products as the benchmark, the next logical step is to launch futures based on those indices. Treasury volatility futures pique my interest the most, as a liquid futures market for fixed income volatility doesn’t exist today, and CME seems like the right home for the product given their dominant interest rate complex in the US.

The Block crunched the numbers and found that Robinhood has so far received $453 million this year in payments for order flow, up sharply from prior years driven by the rise in retail engagement in the equity markets. Bloomberg also reported this week that Robinhood has engaged banks to begin the IPO process with a debut as early as Q1 2021.

In an interesting development, ICE Benchmark Administration said this week that they plan to cease *most* LIBOR calculations late next year, but may continue to publish the US Dollar version of LIBOR past the deadline as discussions with regulators remain ongoing. The decision could introduce confusion or doubt towards the true ending of LIBOR next year, if at all. SOFR futures volumes have begun to pick up on CME, but the Eurodollar market (based on LIBOR) still dwarfs SOFR in size.

Chart of the Week

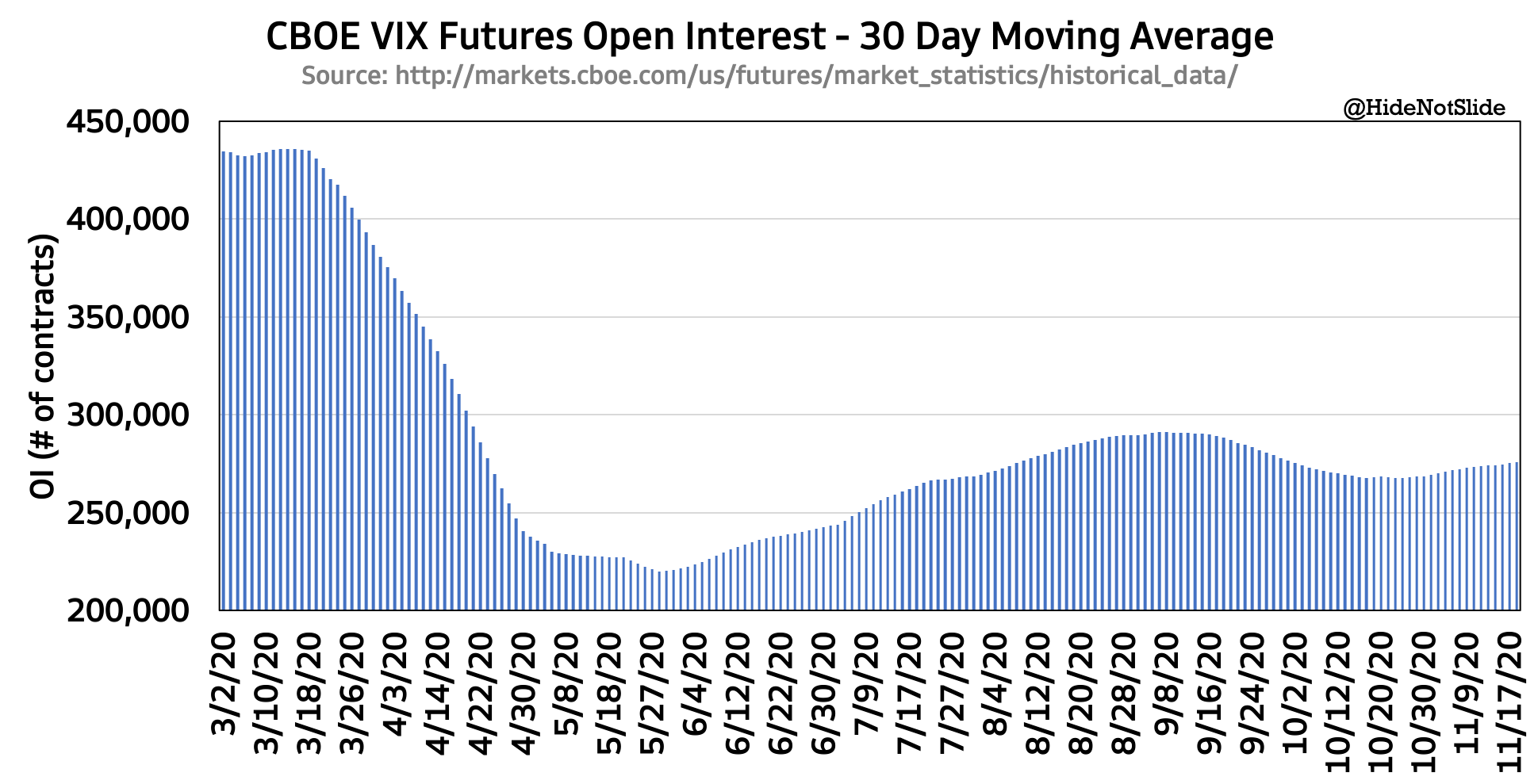

In early April 2020 I wrote a Seeking Alpha article where I talked about the March volatility & its impact on CBOE’s VIX futures complex. The VIX reached an all time high of 82.69 on March 16, 2020 - higher than the depths of the ‘08 - ‘09 financial crisis. The historic volatility caused open interest to crater in VIX futures as traders were blown out of their positions.

Open interest bottomed on May 22 and has been slowly clawing its way back since. With the index now bouncing around in the low 20s, I think OI can recover further as we get more political clarity, AUM starts to flow back into volatility funds, and VIX traders put their hedges back on at lower levels. If we do see OI return to pre-COVID levels, I think CBOE’s stock can start to build a meaningful uptrend going into 2021.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, CBOE, NDAQ and VIRT.