A Post-Investor Day Cboe Review

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges & market structure every Friday. If you have questions or feedback, please reply to this email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below & be sure to share with friends & colleagues:

News

Cboe Investor Day: Readers who’ve followed my writing for very long know my lack of love for Cboe. I’ve avoided the stock for some time now despite its market-beating performance this year amid strong options volumes & takeover speculation. Cboe had its first ever Investor Day this week where it updated the public on its strategy & medium term outlook, giving us a chance to revisit the stock & a possible investment thesis.

I like to think about Cboe’s strategy & trajectory in comparison to its closest rival - Nasdaq. Cboe and Nasdaq found themselves in similar positions in early 2016 - both held top market share in US options and were mostly exposed to unpredictable but high-margin, cash flow heavy transaction businesses. After Adena Friedman became Nasdaq’s CEO in early 2017, the company chose to invest in non-transaction products like exclusive index licenses, market technology contracts and analytics & surveillance platforms. These investments gave Nasdaq valuable IP, recurring subscription revenue & exposure to popular medium-term market structure trends (automation, ESG demand, passive investing, etc…). These investments have since paid off in spades - Nasdaq is currently the best performing exchange since 2016 by a wide margin.

Compare this with Cboe. Faced with a similar position in 2016, Cboe invested in a completely different set of businesses, starting with its acquisition of BATS to enter the US equities market. It then bought a slew of data businesses not to access exclusive IP or exposure to popular market structure trends, but to beef up its existing trading businesses. It bought lit & dark equity trading venues around the world, including BIDS, Chi-X Asia & MATCHNow. It expanded its derivatives presence in Europe with its EuroCCP buy, and just this week announced a deal to buy NEO Exchange, a Canadian equities trading & listing venue. These deals send a strategic signal that Cboe values global equities expansion as much as it values its core options & VIX futures franchises.

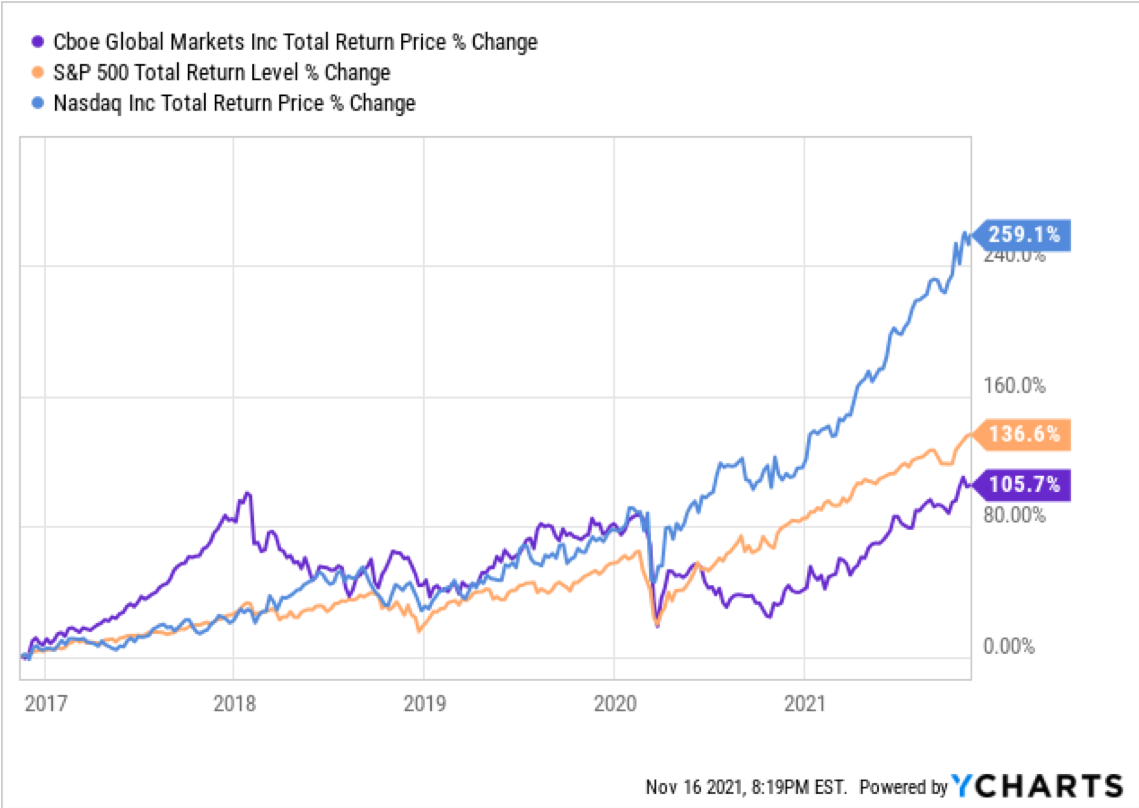

How have these deals been received by the market? To date Cboe is one of the worst performing exchanges over the past five years:

In my opinion the reason for this is the nature of the asset class Cboe is eyeing - equities are considered a mature, efficient & highly regulated part of market structure. Global equity volumes aren’t expected to rapidly grow from today’s levels, and competition for equities market share is fierce. I don’t see a ton of upside in revenue from the companies Cboe has been purchasing, and right now the market seems to agree.

Which brings us to this week’s Investor Day - Cboe walked through a 71 page slide deck largely doubling down on this equities + connected market data strategy. It raised its organic data revenue guidance up to 7-10% annually & pushed the value of a global equities network run on a single platform. It also highlighted its recent pushes into crypto & fixed income as worthwhile investments that will expand Cboe’s addressable customer base. This slide sums it up pretty well:

After digesting Cboe’s investor day materials, my non-bullish thesis on the stock remains intact. I believe Cboe’s investments put them in head-to-head competitive situations against entrenched incumbents that make them difficult to succeed.

European derivatives - entering a stagnant, grid-locked market structure against larger incumbents like Euronext, Deutsche Boerse & LSE.

Crypto - re-entering space ripe with competition from CME, Coinbase, Binance & FTX who’ve all had multi-year head starts on attracting institutional & retail order flow.

US Treasuries - entering an unfamiliar asset class where Tradeweb, Bloomberg & CME control most of the electronic market share with deep network effects & decades of experience.

Could any or all of these initiatives end up working out? Absolutely. Am I willing to tolerate a growing expense base to wait around & find out? Count me out of the Cboe experiment for the time being.

Coinbase Reports Q3 Earnings Results: Crypto’s public bellwether pulled back the curtain on its quarterly performance last week, giving me a chance to re-think my position in the stock. To quickly recap, Coinbase went public earlier this year at a valuation rivaling traditional exchange powerhouses. The stock dipped -30% from IPO highs & I opened a long position at ~$240 per share. My thesis, laid out here, hinged on Coinbase beating volume & revenue expectations as crypto volatility continued into the summer & early fall. Coinbase’s retail revenue capture was astoundingly high & the odds of a spike in trading volume seemed likely. As Q3 came to an end volatility did indeed return to the crypto market, pushing Coinbase revenue expectations above $6 billion & prices back near post-IPO highs:

Q3 earnings caused me to take profits & completely exit my Coinbase position. My change in sentiment came when digesting Coinbase’s alarmingly fast retail & institutional fee compression. At the end of 2020 Coinbase generated ~1.40% in fees from every retail trade. As of Q3 2021 that figure is down to 1.10%. Institutional fee capture has also dropped from .05% in 2020 to .03% this year. These may seem like small changes but they have a significant impact on revenue given Coinbase’s heavy reliance on transaction fees.

Whether it be from competition, a more aware/cost-conscious user base, or both, Coinbase seems to be losing the pricing power that garnered is original high valuation. The exchange would need to see extreme volume growth to offset lower fees or face a steep drop in revenue & earnings in 2022 and ‘23. At a ~$85 billion market cap Coinbase is trading at ~30x next year’s earnings IF volume doesn’t contract. I don’t think the stock presents a good risk/reward above $300 and will be sitting the rest of the year out on this name despite upcoming NFT marketplace launches & non-trading revenue growth.

My latest paid post is live - Options Market Structure 101 gives a clear, detailed picture of the plumbing, incentives & major players in the US options market. Subscribers get immediate access to this post and a deep archive of past exchange & market structure research.

Thank you for your support!

Other Stories I’m Reading

Robinhood Announces Data Security Incident

Micro E-mini Equity Index Futures and Options Surpass 1 Billion Contracts Traded

Coinbase co-founder launches biggest VC fund in crypto

The SEC Crackdown on DeFi is Imminent

Chart of the Week

The chart that never disappoints has again piqued my interest - US options industry volumes are on track to reach a new all-time record in November. More options have traded hands per day this month than in January 2021, when GameStop was squeezing, brokers were sweating & the r/wallstreetbets inmates ruled the asylum.

How is this month different? The retail options frenzy has shifted from a sharp spike to a slow, dull rise nearly every month in 2021. My guess is this month’s sudden jump in activity has been driven by retail favorite Tesla - shares have traded wildly amidst Elon Musk’s weekend Twitter poll & associated stock sale. How Tesla goes, so goes a surprisingly large chunk of the options market.

Keep an eye on the major options exchanges (Nasdaq, CBOE & ICE) this quarter for changes in sentiment around the below chart, and be prepared for even the slightest uptick in volatility to send options volumes surging further.

Thank you for reading this issue of Front Month. Word of mouth is the #1 way others find this newsletter - If you liked this week’s content, please consider sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.

Disclaimer: I am not a financial advisor. Nothing on this site or in the Front Month newsletter should be considered investment advice. Any discussion about future results or projections may not pan out as expected. Do your own research & speak to a licensed professional before making any investment decisions. As of the publishing of this newsletter, I am long ICE, CME, TW, NDAQ and VIRT. I am also long Solana.