A Full Exchange Earnings Preview

Welcome to another issue of Front Month, a newsletter covering the biggest stories in exchanges every Friday. If you have questions or feedback, please reach out via email or find me on Twitter. If you like this newsletter and want to follow the exchange industry with me, please hit the Subscribe button below:

Acquisition Spree in the US and Europe

(Image via Unsplash)

Three separate transactions were announced in the exchange space late last week, all with their own interesting narratives and impact on the industry.

First, the London Stock Exchange announced the sale of Borsa Italiana to Euronext for ~€4.3 billion. The deal looks to benefit both parties immediately following the transaction - for LSE, the divestment eases antitrust concerns and paves the way for the EU’s approval of its landmark Refinitiv deal announced in mid-2019. For Euronext, the acquisition diversifies its business both geographically & strategically, and the company says it can achieve €60 million in run-rate synergies 3 years post-closing.

Second, broker giant TP ICAP announced its acquisition of Liquidnet, an institutional block equities & fixed income platform, for up to $700M. The deal pushes ICAP further into both US equities, brushing up against Virtu’s POSIT dark pool & others, and fixed income, where they plan to invest £25 - £30M to grow the business to rival Bloomberg, Tradeweb and MarketAxess. It will be interesting to hear comments from TW & MKTX management on downstream impacts to their business during Q3 earnings season.

Lastly, Citadel announced it plans to buy IMC’s designated market making (DMM) business as it expands on the NYSE trading floor. As a quick refresher, the NYSE operates a hybrid machine/human model at its exchanges where the DMMs stand as the human element in both the IPO process and secondary trading of stocks. The DMM is responsible for running the initial auction to establish the first traded price of an IPO, as well as aid price discovery & ensure “fair and orderly markets” for their assigned securities. The NYSE has some helpful detail here if interested.

If the deal is approved, Citadel would become the lead DMM for more than half of all stocks traded on the NYSE, potentially raising concerns that the business is becoming too concentrated. News of the deal comes as Bloomberg reports Citadel’s profit doubled in the first half of 2020, and handled more than a quarter of all US equity volume.

CME Mulls Ether Futures

(Image via Unsplash)

Coindesk recently reported that CME has been gauging demand for Ether futures through discussions with clients and trading partners. Ether is the second largest cryptocurrency by market cap (~$43 billion vs Bitcoin’s ~$210 billion) and is the logical next step for new crypto products at the exchange. CME has already rolled out the Ether-Dollar Reference Rate as the index on which to launch a future, and some customers are saying an Ether product is “overdue”. As of October 9th, CME had close to $500 million in Bitcoin futures open interest with ADV of ~42,000 Bitcoin traded over the last 30 days.

Earnings Preview

A large majority of public exchange & data companies will report earnings towards the end of the month, giving investors a flood of new information to assess the current & future trajectory of the space as a whole.

Topics of note across all earnings reports will likely include:

Transaction tax comments - every exchange should get a question on the recent headlines around moving operations out of New Jersey if new taxes are passed. This will be their chance to get a good soundbite in supporting their views & fighting back against the recent scrutiny.

Debt issuance - 2020 has seen issuance figures crush records, with direct impacts to the ratings agencies (more issuance = more debt to rate, more revenue) and exchanges with interest rate exposure (more issuance = more outstanding debt to trade & hedge with futures). I’ll be looking for clues about the 2021 outlook for issuance with dovish monetary policy likely to stay around for the foreseeable future.

ESG - The new craze sweeping the investing world has become a sizable revenue stream for exchanges and data companies, who have built new products to meet the growing demand for socially responsible investing. Analysts have tried to assess the long term market opportunity for ESG in the past, and with each quarter showing more contribution from these segments, the analysis becomes all the more important.

I’ve laid out my top 3 earnings questions for each company below:

Exchanges head into earnings season having struggled through a quarter where low rates volatility and political uncertainty have weighed on performance. Not a single exchange stock beat the market in Q3:

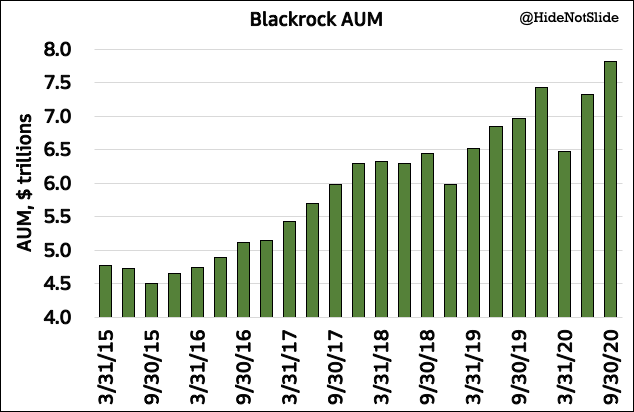

Chart of the Week

Blackrock reported earnings this week and blew away expectations. EPS beat estimates by 19% and assets under management beat by 18%. The company is now approaching the $8 trillion AUM mark as markets flirt with all time highs and the active-to-passive trend continues to build. In the short term, there looks to be nothing stopping Blackrock from extending its dominance in both the asset management space and on Wall Street more broadly:

Thank you for reading this issue of Front Month. If you liked this newsletter, please consider subscribing and sharing with friends & colleagues. Questions & feedback can be sent via email or Twitter.